- Summary

- Table Of Content

- Methodology

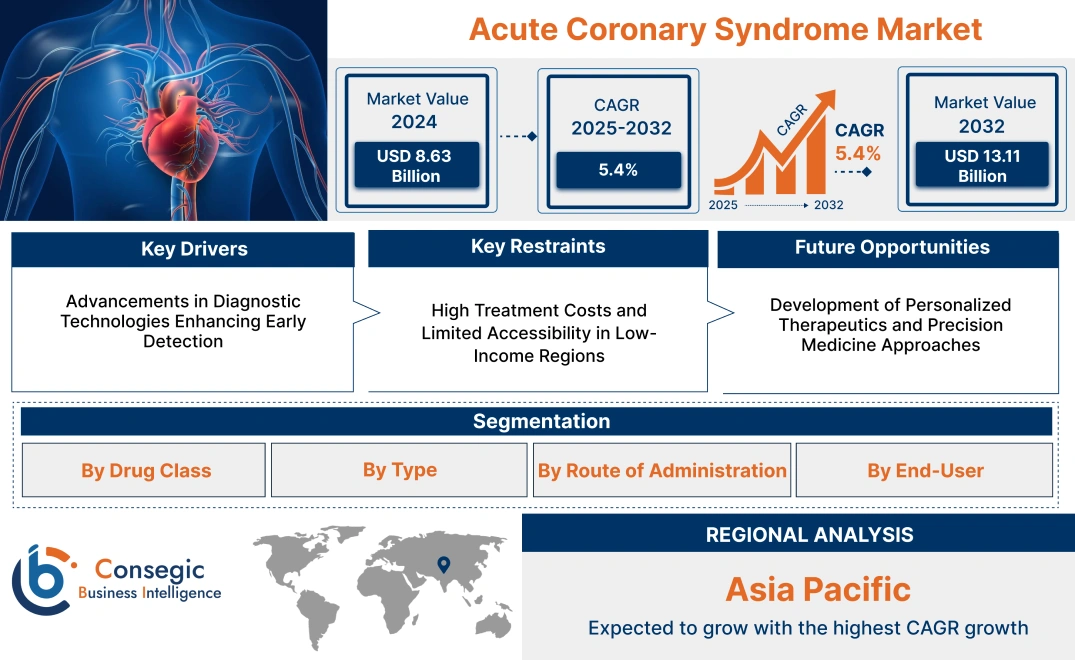

Acute Coronary Syndrome Market Size:

Acute Coronary Syndrome Market Size is estimated to reach over USD 13.11 Billion by 2032 from a value of USD 8.63 Billion in 2024 and is projected to grow by USD 8.94 Billion in 2025, growing at a CAGR of 5.4% from 2025 to 2032.

Acute Coronary Syndrome Market Scope & Overview:

Acute coronary syndrome (ACS) encompasses a range of conditions associated with sudden, reduced blood flow to the heart, including heart attacks and unstable angina. This condition results from the buildup of plaque in coronary arteries, leading to chest pain, shortness of breath, and, in severe cases, life-threatening complications. Timely diagnosis and treatment are essential for managing ACS, which includes therapies such as antiplatelet medications, thrombolytics, and surgical interventions like angioplasty. Key end-users include hospitals, specialized cardiac centers, and clinics, which provide critical care and management for ACS.

Acute Coronary Syndrome Market Dynamics - (DRO) :

Key Drivers:

Advancements in Diagnostic Technologies Enhancing Early Detection

The evolution of diagnostic technologies has markedly improved the early detection and management of ACS. High-sensitivity cardiac troponin assays, for instance, have enhanced the accuracy of myocardial infarction diagnosis, enabling prompt and appropriate therapeutic interventions. Additionally, advancements in imaging modalities, such as coronary computed tomography angiography (CCTA) and cardiac magnetic resonance imaging (MRI), provide detailed visualization of coronary anatomy and myocardial tissue characterization, facilitating precise risk stratification and personalized treatment plans. The integration of artificial intelligence (AI) and machine learning algorithms into these diagnostic tools further augments their predictive capabilities, leading to improved patient outcomes and driving the acute coronary syndrome market demand.

Key Restraints :

High Treatment Costs and Limited Accessibility in Low-Income Regions

Despite therapeutic advancements, the high cost of ACS treatments poses a significant barrier to acute coronary syndrome market growth, particularly in low- and middle-income countries. Interventions such as percutaneous coronary intervention (PCI) and coronary artery bypass grafting (CABG), along with long-term pharmacotherapy involving antiplatelet agents, statins, and beta-blockers, incur substantial expenses. Limited healthcare infrastructure and inadequate insurance coverage in these regions further exacerbate the issue, restricting patient access to essential treatments. This disparity underscores the need for cost-effective therapeutic strategies and equitable healthcare policies to enhance the accessibility and affordability of ACS management globally.

Future Opportunities :

Development of Personalized Therapeutics and Precision Medicine Approaches

The shift towards personalized medicine presents a significant opportunity in the ACS market. Understanding the genetic and molecular underpinnings of ACS has led to the identification of novel therapeutic targets and the development of tailored treatment regimens. For example, pharmacogenomic testing can guide the selection of antiplatelet therapy, optimizing efficacy and minimizing adverse effects. Additionally, the exploration of biomarkers for risk stratification enables clinicians to identify high-risk patients who may benefit from more aggressive interventions. The integration of precision medicine into ACS management not only enhances patient outcomes but also fosters innovation in drug development, offering substantial acute coronary syndrome market opportunities.

Acute Coronary Syndrome Market Segmental Analysis :

By Drug Class:

Based on drug class, the market is segmented into antiplatelet drugs, beta-blockers, statins, ACE inhibitors, angiotensin II receptor blockers (ARBs), antithrombotic agents, and others.

The antiplatelet drugs segment accounted for the largest revenue share of the total acute coronary syndrome market share in 2024.

- Antiplatelet drugs are critical in ACS management due to their role in preventing blood clots and reducing the risk of recurrent cardiac events.

- Commonly prescribed antiplatelets like aspirin and clopidogrel are mainstays in ACS treatment protocols, especially for high-risk patients.

- The widespread use of dual antiplatelet therapy (DAPT) after myocardial infarction (MI) and angioplasty procedures supports the dominant position of this segment.

- The availability of new antiplatelet agents with enhanced efficacy and safety profiles is also contributing to this segment's growth.

- Thus, as per the segmental trends analysis, antiplatelet drugs lead the market due to their essential role in clot prevention and their critical use in dual therapy for reducing recurrent cardiac risks in ACS patients, driving the acute coronary syndrome market growth.

The statins segment is anticipated to register the fastest CAGR during the forecast period.

- Statins are increasingly prescribed to ACS patients as they lower cholesterol levels, reducing the risk of atherosclerotic plaque formation.

- Their use is associated with improved long-term outcomes, particularly in reducing secondary events following ACS.

- Statins are an integral part of the preventive strategy in ACS management, and the development of advanced formulations with enhanced efficacy and fewer side effects is driving their growth.

- The rising focus on preventive cardiology and improved patient compliance with newer, long-acting formulations are expected to propel the statins segment's rapid growth.

- Statins are expected to grow rapidly due to their preventive role in reducing recurrent cardiac events, supported by advancements in drug formulations that improve efficacy and patient compliance, boosting the acute coronary syndrome market trends.

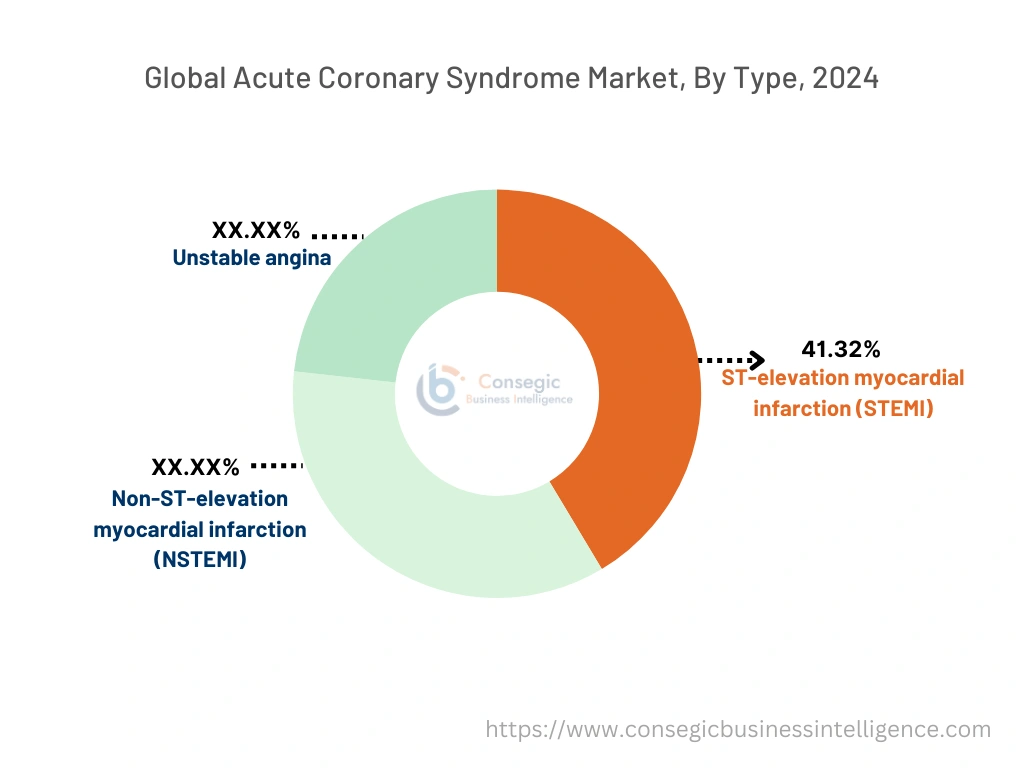

By Type:

Based on type, the market is segmented into unstable angina, non-ST-elevation myocardial infarction (NSTEMI), and ST-elevation myocardial infarction (STEMI).

The ST-elevation myocardial infarction (STEMI) segment accounted for the largest revenue share of 41.32% in 2024.

- STEMI is the most severe type of ACS, requiring immediate intervention to restore blood flow and minimize heart muscle damage.

- Due to its critical nature, STEMI cases often involve intensive therapies, such as primary percutaneous coronary intervention (PCI) and thrombolytic therapy, contributing to higher treatment costs and demand.

- With the rising incidence of STEMI and the emphasis on rapid treatment protocols to improve patient outcomes, this segment leads the market.

- Therefore, the analysis of segments shows that STEMI dominates the market, driven by the critical need for immediate and intensive treatment interventions, boosting the acute coronary syndrome market demand.

The unstable angina segment is anticipated to register the fastest CAGR during the forecast period.

- Unstable angina, while less severe than STEMI, requires urgent medical attention and is often a precursor to more serious events like myocardial infarction.

- The management of unstable angina involves comprehensive pharmacological intervention, including the use of antiplatelet drugs, statins, and beta-blockers, to stabilize the patient and prevent progression.

- As healthcare systems place greater emphasis on early detection and management of unstable angina to prevent escalation, the demand for targeted therapies in this segment is expected to grow.

- Unstable angina is expected to grow rapidly due to the increasing focus on early detection and intervention to prevent progression to more severe ACS events, creating lucrative acute coronary syndrome market opportunities.

By Route of Administration:

Based on the route of administration, the market is segmented into oral and injectable.

The oral segment accounted for the largest revenue share of the global acute coronary syndrome market in 2024.

- Oral medications, including antiplatelet agents, statins, and ACE inhibitors, form the backbone of ACS management, particularly for long-term maintenance therapy.

- These medications are integral to secondary prevention strategies, reducing the risk of recurrent ACS events.

- Patient preference for oral formulations, which are easier to administer and adhere to, has solidified this segment's leading position in the market.

- Additionally, advancements in oral drug formulations, including extended-release tablets, have enhanced patient compliance and efficacy.

- The segmental trends analysis portrays that oral medications lead the market due to their essential role in long-term ACS management, boosting the acute coronary syndrome market expansion.

The injectable segment is anticipated to register the fastest CAGR during the forecast period.

- Injectable treatments, such as thrombolytic agents and certain antithrombotic therapies are crucial in the acute management of ACS, particularly in emergency settings for rapid intervention.

- The use of injectable agents is common in hospital settings, where the immediate effect is necessary to stabilize patients and prevent further cardiac damage.

- The growing demand for rapid and Effective treatment options in high-risk ACS patients, combined with advancements in injectable drug formulations, is driving growth in this segment.

- Hence, the analysis of segmental trends depicts that injectables are expected to grow rapidly as they are vital in acute ACS management, especially in emergency settings where fast-acting interventions are critical.

By End-User:

Based on end-users, the market is segmented into hospitals, ambulatory surgical centers (ASCs), specialty clinics, and others.

The hospitals segment accounted for the largest revenue share of the overall acute coronary syndrome market share in 2024.

- Hospitals are the primary setting for ACS treatment, particularly for severe cases requiring intensive care and surgical intervention.

- Advanced diagnostic and treatment facilities, such as cardiac catheterization labs and specialized cardiac care units, make hospitals the main choice for ACS management.

- Hospitals are also equipped to handle complex cases of STEMI and unstable angina, providing comprehensive care through multidisciplinary teams.

- The high volume of ACS cases handled in hospitals, along with their role in administering critical treatments, supports their dominant market position.

- As per the acute coronary syndrome market analysis, hospitals lead the ACS market due to their capacity to manage high-risk cases and provide comprehensive treatment options, including intensive and surgical interventions.

The ambulatory surgical centers (ASCs) segment is anticipated to register the fastest CAGR during the forecast period.

- ASCs are becoming an increasingly preferred setting for certain ACS-related procedures, such as follow-up angioplasty and low-risk interventions, due to their cost-effectiveness and shorter patient stays.

- These centers provide an alternative to hospitals for patients requiring specific procedures with minimal recovery time.

- The increasing focus on outpatient cardiac procedures, particularly in developed markets, is driving the adoption of ASCs for ACS management.

- Additionally, the expansion of ASC services to include advanced cardiac care is supporting their rapid growth.

- ASCs are expected to grow rapidly as they offer cost-effective solutions for certain ACS procedures, aligning with the trend toward outpatient cardiac care and shorter recovery times, proliferating the acute coronary syndrome market trends.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

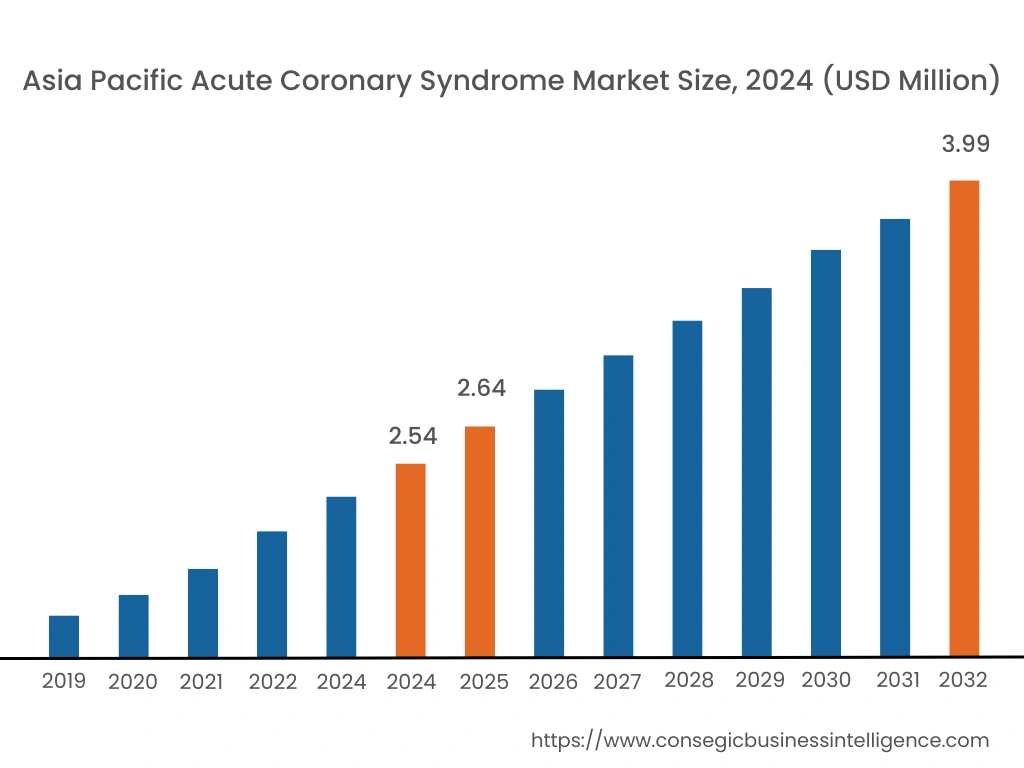

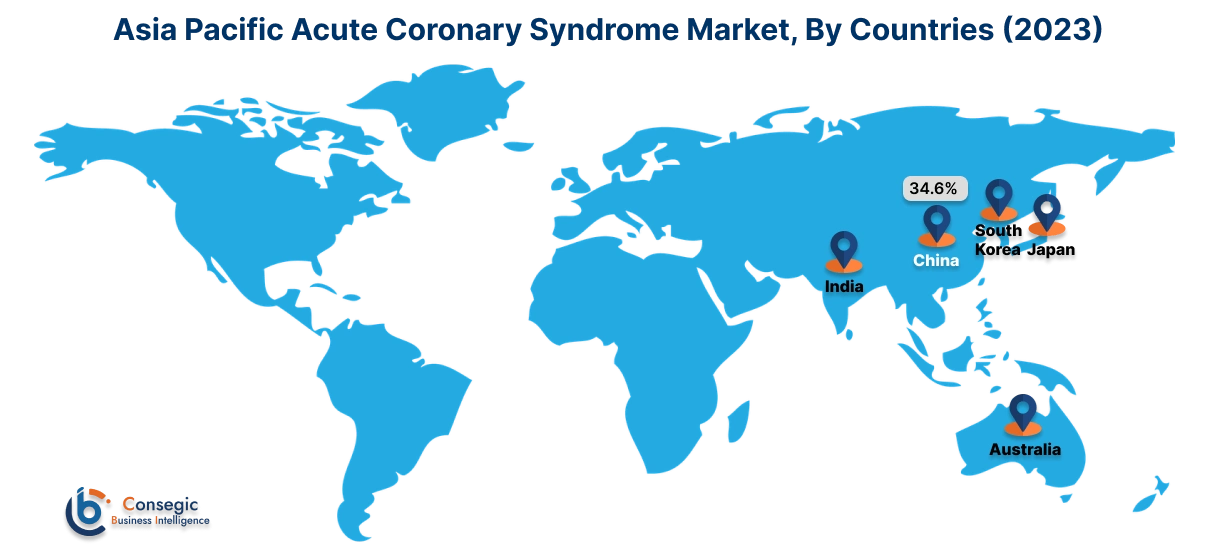

Asia Pacific region was valued at USD 2.54 Billion in 2024. Moreover, it is projected to grow by USD 2.64 Billion in 2025 and reach over USD 3.99 Billion by 2032. Out of this, China accounted for 34.6% of the total market share. Asia-Pacific is witnessing rapid growth in the ACS market, driven by rising cardiovascular cases linked to urbanization, dietary shifts, and aging populations, particularly in China, Japan, and South Korea. China is channeling substantial investments into cardiovascular health, including ACS research and patient outreach programs, as part of national health improvement efforts. Japan is also advancing precision medicine approaches for ACS treatment, supported by its extensive healthcare infrastructure. Many hospitals in India and Southeast Asia are increasingly adopting international cardiac treatment protocols, although access discrepancies between urban and rural areas remain a challenge, slowing overall adoption rates.

North America leads the market with its high concentration of advanced healthcare facilities and focus on innovative ACS management solutions. The U.S. healthcare system emphasizes early intervention and treatment of cardiovascular conditions, driving demand for advanced antiplatelet and antithrombotic therapies. Research institutions in the U.S. and Canada are actively involved in developing next-generation ACS treatments, including novel biologics and combination therapies to improve outcomes. The market is also shaped by the high availability of skilled healthcare professionals and specialized cardiac care centers, although the cost of ACS management remains a critical issue impacting patient access in some areas.

Europe's ACS market is bolstered by strong patient access to public healthcare systems and proactive cardiovascular disease prevention programs. Germany and the UK, in particular, are focusing on clinical trials for new ACS treatments, aiming to improve therapeutic efficacy and reduce hospital readmission rates. The region has been seeing investments in integrated care models where digital health solutions are employed to monitor at-risk populations and manage post-ACS patient care. While these innovations support growth, austerity measures, and strict pharmaceutical pricing regulations across several European countries often constrain market revenues.

The regional trends analysis shows that the Middle East and Africa is growing, with particular emphasis on tackling risk factors such as high obesity and diabetes rates, especially in Gulf countries. Saudi Arabia and the UAE are expanding their cardiology departments and establishing comprehensive care facilities to address the increasing demand for ACS treatments. These countries are also importing state-of-the-art medical devices for ACS intervention, with a rising focus on minimally invasive procedures. The limited availability of specialized cardiologists in several African countries, however, restricts access to advanced ACS care, leaving a gap in the market for locally trained professionals.

In Latin America, the ACS market is evolving, particularly in countries like Brazil, Argentina, and Chile. Government-backed health programs are increasingly prioritizing heart disease prevention, with a focus on lifestyle interventions and early-stage ACS management. Brazil is expanding the deployment of mobile health (mHealth) solutions to reach remote communities and monitor heart conditions, helping to bridge the urban-rural healthcare gap. Mexico is also focusing on public health campaigns targeting at-risk groups, while Argentina invests in improving emergency response systems for ACS cases. However, economic disparities and limited healthcare resources affect access to advanced ACS treatments across the region.

Top Key Players & Market Share Insights:

The acute coronary syndrome market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global acute coronary syndrome market. Key players in the industry include -

- Johnson & Johnson Services, Inc. (USA)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Portola Pharmaceuticals, Inc. (USA)

- AbbVie Inc. (USA)

- AstraZeneca (UK)

- Amgen Inc. (USA)

- Bayer AG (Germany)

- Eli Lilly and Company (USA)

- Daiichi Sankyo Company, Limited (Japan)

- GlaxoSmithKline plc (UK)

Acute Coronary Syndrome Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 13.11 Billion |

| CAGR (2025-2032) | 5.4% |

| By Drug Class |

|

| By Type |

|

| By Route of Administration |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the acute coronary syndrome market? +

In 2024, the acute coronary syndrome market was USD 8.63 billion.

What will be the potential market valuation for acute coronary syndrome by 2032? +

In 2032, the market size of acute coronary syndrome is expected to reach USD 13.11 billion.

What are the segments covered in the acute coronary syndrome market report? +

The drug class, type, route of administration, end user, and region are the segments covered in this report.

Who are the major players in the acute coronary syndrome market? +

Johnson & Johnson Services, Inc. (USA), Teva Pharmaceutical Industries Ltd. (Israel), Portola Pharmaceuticals, Inc. (USA), AbbVie Inc. (USA), AstraZeneca (UK), Amgen Inc. (USA), Bayer AG (Germany), Daiichi Sankyo Company, Limited (Japan), Eli Lilly and Company (USA), GlaxoSmithKline plc (UK) are the major players in the acute coronary syndrome market.