- Summary

- Table Of Content

- Methodology

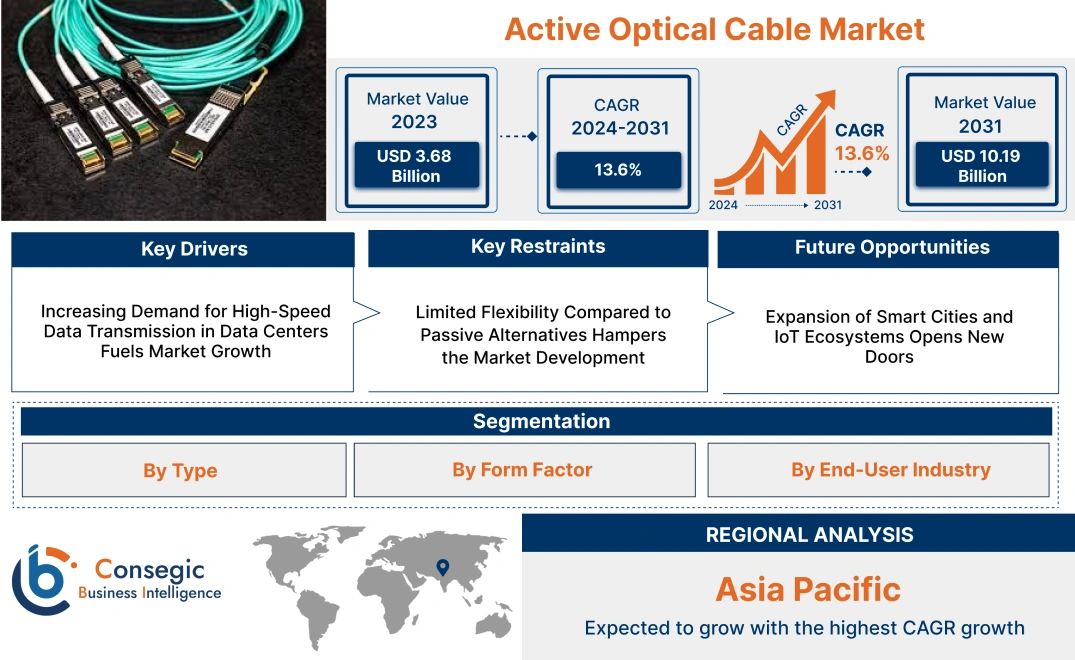

Active Optical Cable Market Size:

Active Optical Cable Market size is estimated to reach over USD 10.19 Billion by 2031 from a value of USD 3.68 Billion in 2023 and is projected to grow by USD 4.11 Billion in 2024, growing at a CAGR of 13.6% from 2024 to 2031.

Active Optical Cable Market Scope & Overview:

An active optical cable is a high-performance cable designed to transmit data over long distances using optical fiber technology integrated with electronic components. These cables are equipped with signal processing and conversion modules that enhance transmission quality, providing faster data transfer rates, lower power consumption, and extended reach compared to traditional copper cables. It is widely used in data centers, high-performance computing (HPC), and telecommunications, where high-speed, reliable data transmission is essential.

These cables are available in various configurations, such as HDMI, USB, InfiniBand, and DisplayPort, catering to different application requirements. Their lightweight structure and resistance to electromagnetic interference (EMI) make them ideal for environments requiring uninterrupted data flow. Additionally, it supports plug-and-play functionality, ensuring easy installation and compatibility with a wide range of devices and systems.

End-users of these cables include data center operators, IT infrastructure providers, and industries such as aerospace, healthcare, and media, where efficient and high-bandwidth connectivity is critical. Active optical cables are integral to enabling seamless communication, reducing latency, and supporting advanced networking solutions in modern technology ecosystems.

Active Optical Cable MarketDynamics - (DRO) :

Key Drivers:

Increasing Demand for High-Speed Data Transmission in Data Centers Fuels Market Growth

The global expansion of data centers, driven by the growing reliance on cloud computing, AI workloads, and big data analytics, is creating significant demand for high-speed data transmission solutions. Data centers require efficient communication across servers, switches, and storage systems to handle ever-increasing data volumes with minimal latency. Active optical cables (AOCs) have emerged as a critical solution, offering ultra-fast transmission speeds and superior bandwidth over long distances, which is essential for supporting modern data center architectures. Unlike traditional copper cables, AOCs minimize signal degradation and electromagnetic interference, ensuring reliable connectivity in dense data center environments.

As cloud service providers and enterprises adopt virtualization technologies, the need for scalable interconnect solutions like AOCs continues to grow. Moreover, the rise of AI workloads, which require high-speed data exchange between GPUs, CPUs, and accelerators, further highlights the importance of AOCs in enabling efficient processing. Additionally, hyperscale data centers are deploying AOCs to optimize their rack-to-rack and intra-data center communications, ensuring seamless scalability to meet future requirements. As per the market trends analysis, the ongoing shift toward high-performance computing makes AOCs indispensable for next-generation data centers further fueling the active optical cable market growth.

Key Restraints :

Limited Flexibility Compared to Passive Alternatives Hampers the Market Development

Active optical cables (AOCs) are inherently less mechanically flexible than traditional copper cables, posing constraints in environments where frequent movement, bending, or reconfiguration is required. The optical fibers within AOCs are highly sensitive to stress and strain, making them susceptible to physical damage such as micro-fractures or signal degradation when bent beyond their tolerance limits. This lack of robustness increases the likelihood of failure during installation or repeated handling, especially in dynamic environments like event production, broadcasting, or temporary networking setups.

Additionally, the integrated design of AOCs, which combines optical fibers with active components like transceivers, adds to their fragility. Excessive bending or improper handling compromises both the optical and electrical functionalities, requiring costly replacements. Industries that prioritize durability and adaptability, such as industrial manufacturing or military operations, may find AOCs unsuitable for deployments in harsh or high-mobility conditions. Furthermore, the use of protective sheathing to enhance durability often increases the overall cost and weight of AOCs, further reducing their appeal in scenarios where lightweight and flexible cabling solutions are preferred, which hinders the active optical cable market demand.

Future Opportunities :

Expansion of Smart Cities and IoT Ecosystems Opens New Doors

The rapid development of smart city infrastructure and the widespread adoption of IoT ecosystems present substantial growth opportunities for active optical cables (AOCs). Smart cities depend on seamless connectivity between a diverse range of devices, including environmental sensors, surveillance cameras, traffic management systems, and energy grids. These interconnected systems require high-speed, low-latency communication networks to process and transmit real-time data efficiently, ensuring smooth urban operations.

AOCs are uniquely suited to meet these needs, offering superior bandwidth and reliability compared to traditional cabling solutions. Their ability to support high-frequency data transmission over long distances without signal degradation makes them essential for the backbone of smart city networks, such as fiber-to-the-home (FTTH) installations and centralized control systems. Additionally, AOCs facilitate the scalability needed for expanding urban IoT networks, enabling the seamless addition of new devices and applications as cities grow. Moreover, as smart cities integrate more advanced applications like autonomous vehicles, connected public transportation systems, and smart healthcare services, the need for robust and scalable communication infrastructure further drives significant active optical cable market opportunities, solidifying their role in modern urban ecosystems.

Active Optical Cable Market Segmental Analysis :

By Type:

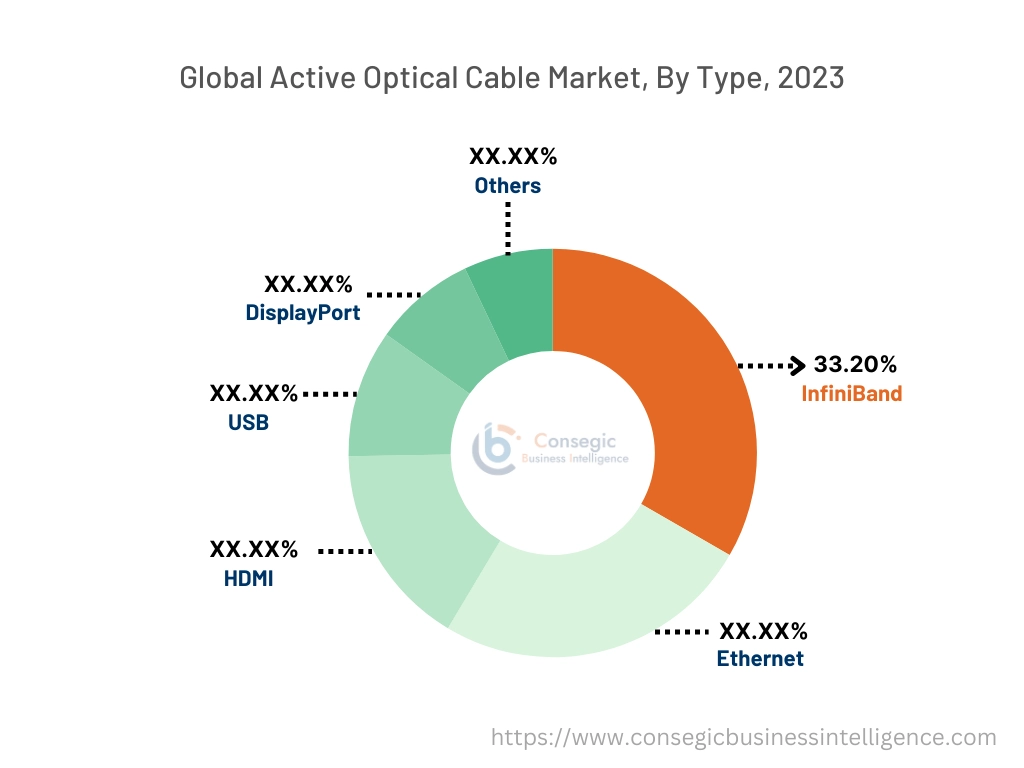

Based on type, the market is segmented into InfiniBand, Ethernet, HDMI, USB, DisplayPort, and Others.

The InfiniBand segment held the largest revenue of 33.20% of the total active optical cable market share in 2023.

- InfiniBand cables are widely adopted in data centers and high-performance computing (HPC) systems due to their low latency and high data transfer rates.

- They are essential for connecting servers and storage systems, enabling seamless communication in large-scale computing environments.

- The increasing complexity of workloads in data centers is driving the adoption of InfiniBand solutions for efficient data transmission.

- As per segmental trends analysis, InfiniBand remains a preferred choice for applications requiring robust connectivity and high bandwidth, particularly in IT & telecom sectors, contributing to the active optical cable market expansion.

The Ethernet segment is expected to register the fastest CAGR during the forecast period.

- Ethernet cables are extensively used in telecommunications and enterprise networking, offering compatibility with a wide range of devices and systems.

- Innovations in Ethernet technology, including 400G and beyond, are enabling faster data transfer and greater network scalability.

- The rapid growth of this segment is supported by trends in cloud computing and IoT, which demand reliable and efficient networking solutions.

- As per active optical cable market trends, Ethernet’s adaptability and cost-effectiveness make it a key player in modern networking infrastructure.

By Form Factor:

Based on form factor, the market is segmented into QSFP, SFP, CXP, CX4, Mini-SAS, and Others.

The QSFP (Quad Small Form Factor Pluggable) segment held the largest revenue of the total active optical cable market share in 2023.

- QSFP connectors are widely used in data centers for high-speed interconnections, supporting up to 100G Ethernet and InfiniBand networks.

- Their compact design and high-density port capabilities make them ideal for scaling networking systems without compromising on space or performance.

- Trends in data center modernization and the transition to higher-speed networks are driving the adoption of QSFP-based solutions across industries.

- As per active optical cable market analysis, the dominance of QSFP connectors reflects their critical role in enabling efficient, high-speed data communication in the IT and telecom sectors.

The Mini-SAS segment is expected to register the fastest CAGR during the forecast period.

- Mini-SAS connectors are commonly used in storage systems and enterprise applications, providing reliable and high-speed data transfer for short-distance connections.

- These connectors are gaining traction in industries like healthcare and media for transferring large data files, such as medical images and video content.

- The segment's proliferation is attributed to the increasing focus on storage optimization and efficient data management across industries.

- The active optical cable market trends analysis highlights Mini-SAS as a reliable solution for compact and high-performance connectivity in specialized applications, driving active optical cable market growth.

By End-User Industry:

Based on the end-user industry, the market is segmented into IT & Telecom, Healthcare, Consumer Electronics, Automotive, Aerospace & Defense, and Media & Entertainment.

The IT & Telecom segment accounted for the largest revenue share in 2023.

- Active optical cables are integral to the IT & telecom sector, supporting high-speed data transfer in cloud computing, edge computing, and 5G infrastructure.

- Data centers rely heavily on these cables for efficient networking and storage, enabling seamless communication and reduced latency.

- As per market analysis, trends in digital transformation and the increasing adoption of AI-driven applications are fueling the demand for high-performance connectivity solutions.

- This segment's dominance reflects its pivotal role in supporting global communication networks and digital ecosystems, fueling the active optical cable market demand.

The Media & Entertainment segment is expected to register the fastest CAGR during the forecast period.

- The media industry leverages active optical cables for transmitting high-definition (HD) and ultra-high-definition (UHD) video content across production and broadcasting systems.

- These cables are widely used in live streaming and virtual production environments, where low latency and high-speed data transfer are critical.

- As the requirement for immersive media experiences grows, including VR and AR content, the adoption of AOCs in this industry is expanding.

- The segment’s rapid growth is supported by advancements in video resolution standards and the proliferation of digital media platforms, encouraging the active optical cable market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

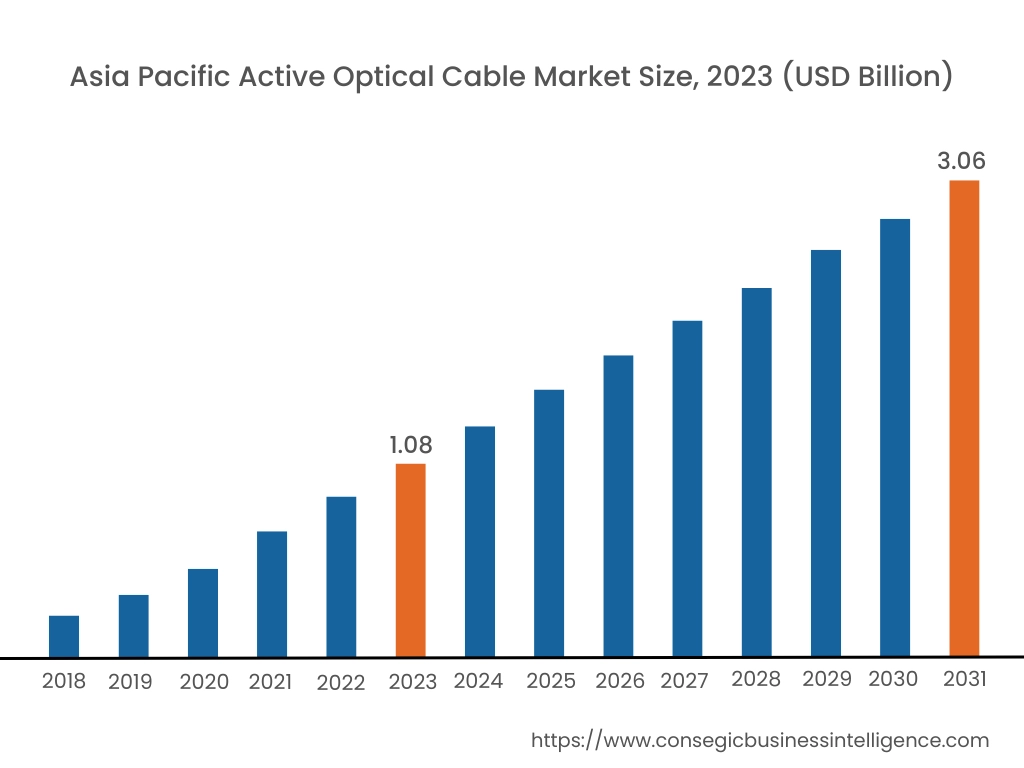

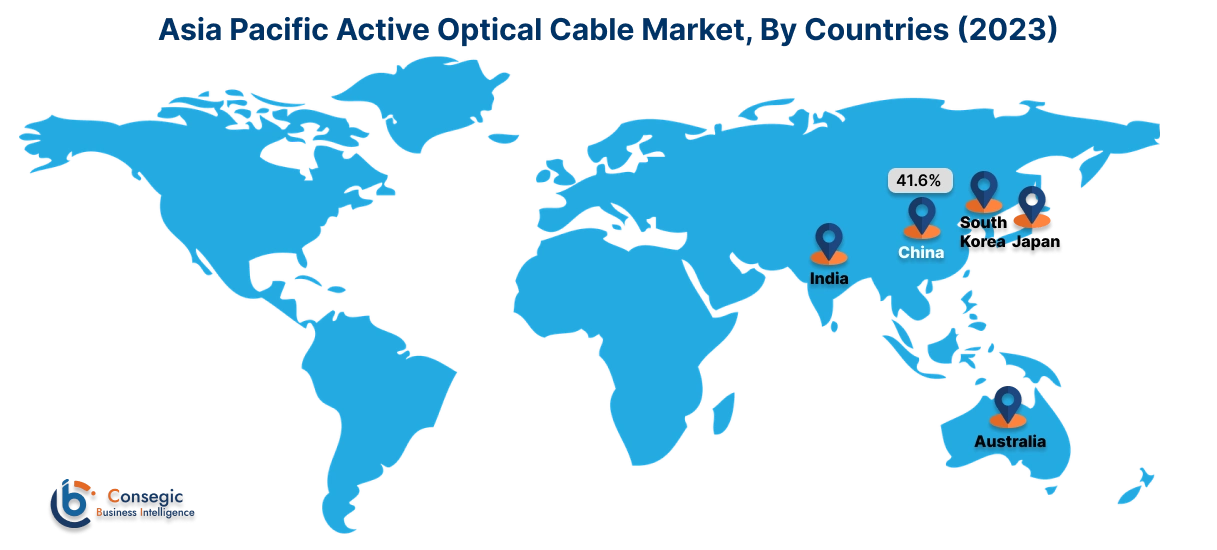

Asia Pacific region was valued at USD 1.08 Billion in 2023. Moreover, it is projected to grow by USD 1.21 Billion in 2024 and reach over USD 3.06 Billion by 2031. Out of these, China accounted for the largest share of 41.6% in 2023. Asia-Pacific is experiencing rapid adoption of AOCs, driven by the development of telecommunications networks and the proliferation of consumer electronics. Nations such as China, Japan, and South Korea are investing heavily in upgrading their data transmission capabilities, thereby creating active optical cable market opportunities.

North America is estimated to reach over USD 3.35 Billion by 2031 from a value of USD 1.22 Billion in 2023 and is projected to grow by USD 1.37 Billion in 2024. This region holds a significant share of the AOC market, primarily due to the extensive deployment of data centers and high-performance computing systems. The United States, in particular, has seen substantial adoption of AOCs to meet the increasing need for high-speed data transmission in sectors such as cloud computing and telecommunications.

In Europe, countries like Germany, France, and the United Kingdom are at the forefront of AOC adoption. As per active optical cable market analysis, the region's emphasis on technological innovation and the modernization of IT infrastructure has led to the integration of AOCs in various applications, including consumer electronics and digital signage.

The Middle East & Africa region is gradually embracing AOC technology, particularly in countries like the United Arab Emirates and South Africa. As per active optical cable market trends, the focus on enhancing digital infrastructure and the growing adoption of high-speed internet services contribute to the market's growth.

Latin America presents emerging opportunities for the AOC market, with Brazil and Mexico leading the charge. The increasing focus on digital transformation and the modernization of communication networks are key factors driving market growth.

Top Key Players & Market Share Insights:

The Active Optical Cable market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Active Optical Cable market. Key players in the Active Optical Cable industry include –

- Coherent Corp. (USA)

- Broadcom Inc. (USA)

- Sumitomo Electric Industries, Ltd. (Japan)

- JPC Connectivity (Taiwan)

- Shenzhen Sopto Technology Co., Ltd. (China)

- Linkreal Co., Ltd. (China)

- Lightwave Inc. (USA)

- Black Box (USA)

- ACT (Taiwan)

- IOI Technology Corporation (Taiwan)

Recent Industry Developments :

Product Launches:

- In August 2024, Chord Company launched the Clearway HDMI AOC, a high-performance active optical cable supporting 8K at 60Hz and 4K at 120H Designed for home cinema and gaming, it offers long-distance transmission up to 20 meters with low interference and high durability. The Clearway HDMI AOC ensures superior audio-visual experiences with its lightweight, flexible build and premium materials, meeting HDMI 2.1 specifications. It emphasizes reliability and top-notch performance for demanding AV applications.

- In November 2023, Credo Semiconductor unveiled the world’s first 800G DSP for linear receive optics, designed for hyperscale and AI data centers. The DSP supports Credo's High-Bandwidth and Low-Power Retimed Linear Optics (HALO), delivering optimal performance with reduced power consumption. Targeting next-gen interconnects, it aligns with industry needs for energy efficiency in data centers while ensuring robust high-speed data handling.

- In September 2023, Pure-Fi unveiled its Pro HDMI 2.1 Active Optical Cable (AOC). Designed for Pro A/V professionals, it features a modular design with detachable Tx and Rx modules for easy in-wall installation and future upgrades. Certified CL3-rated for safety, it supports 8K at 60Hz and 4K at 120Hz over 1,000 feet with 48 Gbps throughput and near-zero EMI. Durable and flexible, it is ideal for home theaters, gaming, and professional AV setups.

- In September 2023, MaxLinear unveiled its 5nm Keystone PAM4 DSP (MxL93684) with integrated VCSEL drivers for 800G and 400G multimode short-reach optical modules and Active Optical Cables (AOCs). Offering <10W power consumption for 800G links, it supports AI/ML clusters and data centers.

Active Optical Cable Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 140.29 Billion |

| CAGR (2024-2031) | 6.7% |

| By Type |

|

| By Form Factor |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Active Optical Cable Market? +

Active Optical Cable Market size is estimated to reach over USD 10.19 Billion by 2031 from a value of USD 3.68 Billion in 2023 and is projected to grow by USD 4.11 Billion in 2024, growing at a CAGR of 13.6% from 2024 to 2031.

What specific segmentation details are covered in the Active Optical Cable Market report? +

The Active Optical Cable Market report includes segmentation details by type (InfiniBand, Ethernet, HDMI, USB, DisplayPort, Others), form factor (QSFP, SFP, CXP, CX4, Mini-SAS, Others), end-user industry (IT & Telecom, Healthcare, Consumer Electronics, Automotive, Aerospace & Defense, Media & Entertainment), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Active Optical Cable Market? +

The Ethernet segment is expected to register the fastest CAGR during the forecast period. Ethernet cables are increasingly being used in telecommunications and enterprise networking, driven by innovations in Ethernet technology (including 400G and beyond) that enable faster data transfer and greater network scalability.

Who are the major players in the Active Optical Cable Market? +

The major players in the Active Optical Cable Market include Coherent Corp. (USA), Broadcom Inc. (USA), Sumitomo Electric Industries, Ltd. (Japan), JPC Connectivity (Taiwan), Shenzhen Sopto Technology Co., Ltd. (China), Linkreal Co., Ltd. (China), Lightwave Inc. (USA), Black Box (USA), ACT (Taiwan), and IOI Technology Corporation (Taiwan).