- Summary

- Table Of Content

- Methodology

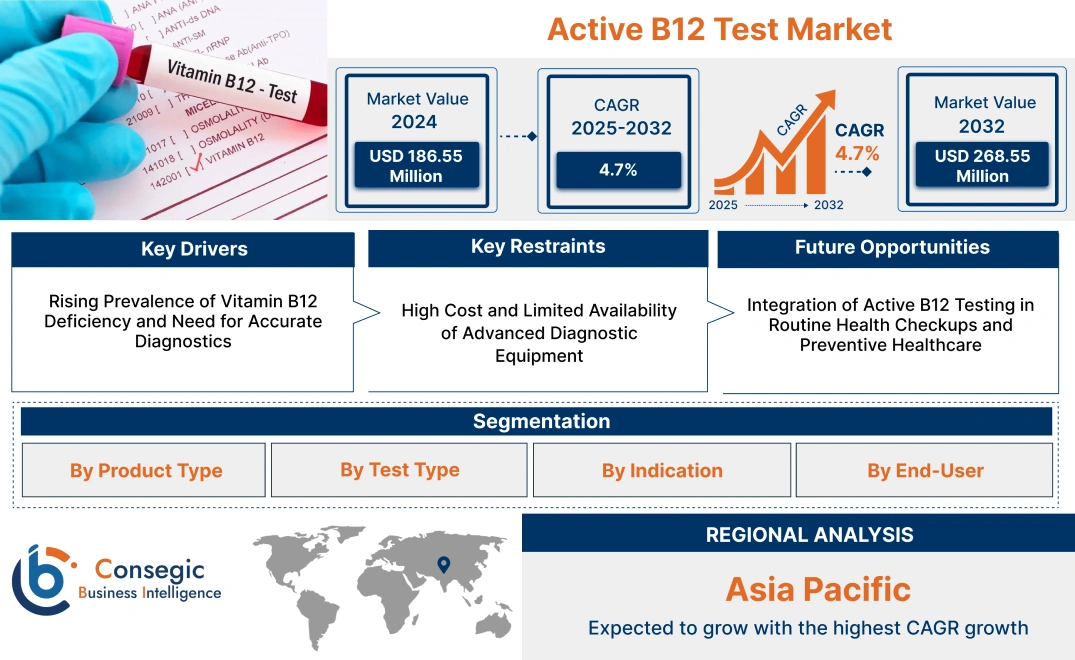

Active B12 Test Market Size:

Active B12 Test Market size is estimated to reach over USD 268.55 Million by 2032 from a value of USD 186.55 Million in 2024 and is projected to grow by USD 191.92 Million in 2025, growing at a CAGR of 4.70 % from 2025 to 2032.

Active B12 Test Market Scope & Overview:

The Active B12 Test is a diagnostic tool that measures the biologically active form of vitamin B12, known as holotranscobalamin, in the bloodstream. This test enables early detection of vitamin B12 deficiencies, which can lead to serious health issues like neurological and hematological disorders if untreated. By focusing on the active portion of vitamin B12, it offers a more precise diagnosis than conventional total B12 tests, allowing healthcare providers to initiate timely intervention. Primary end-users include hospitals, diagnostic laboratories, and research institutions, which rely on accurate and early diagnosis for effective patient management. As healthcare providers focus more on preventive diagnostics, the market is expected to witness consistent growth driven by heightened health awareness and technological advancements.

Active B12 Test Market Dynamics - (DRO) :

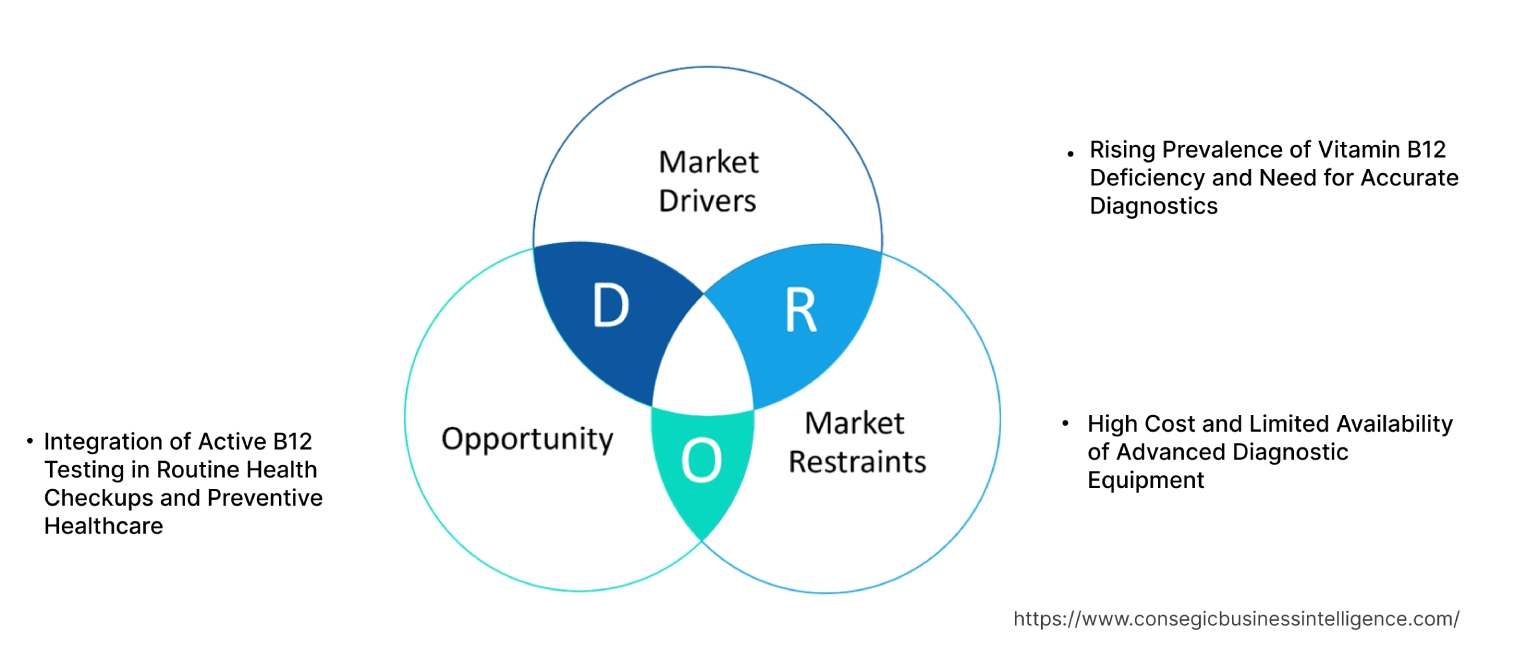

Key Drivers:

Rising Prevalence of Vitamin B12 Deficiency and Need for Accurate Diagnostics

The growing prevalence of vitamin B12 deficiency worldwide, particularly in aging populations, is a primary driver for the active B12 test market growth. Vitamin B12 deficiency is linked to a range of health issues, including neurological disorders, anemia, and cardiovascular problems, underscoring the need for accurate and early diagnosis. Unlike total B12 tests, which measure inactive B12 bound to haptocorrin, active B12 tests provide a more precise indication of the bioavailable form of the vitamin (holotranscobalamin), which is directly involved in cellular metabolism. This differentiation is especially important for diagnosing deficiencies in patients where conventional tests may yield ambiguous results. Healthcare providers are increasingly relying on active B12 tests to improve diagnostic accuracy and deliver targeted treatment for deficiencies, particularly in high-risk groups such as the elderly, individuals with gastrointestinal disorders, and vegetarians. The expanding awareness among clinicians about the clinical benefits of active B12 testing is propelling the demand for this specific diagnostic solution in both developed and emerging markets.

Key Restraints :

High Cost and Limited Availability of Advanced Diagnostic Equipment

Despite its diagnostic advantages, the active B12 test market demand is restrained by the high cost of advanced testing equipment and the limited availability of specialized diagnostic facilities, particularly in low- and middle-income regions. Active B12 testing requires sophisticated immunoassay equipment, which can be costly for healthcare providers, especially smaller clinics and labs operating with limited budgets. Additionally, as active B12 tests are relatively recent compared to traditional B12 assays, not all diagnostic facilities have the infrastructure or trained personnel to conduct these tests. This limits the accessibility of active B12 testing in rural areas and emerging markets, where conventional diagnostic methods are more prevalent. Thus, market analysis shows that the high costs associated with upgrading diagnostic equipment and training healthcare personnel further restrict the widespread adoption of active B12 testing, impacting market penetration, especially in resource-constrained settings.

Future Opportunities :

Integration of Active B12 Testing in Routine Health Checkups and Preventive Healthcare

The integration of active B12 testing into routine health checkups presents a substantial active B12 test market opportunity, particularly as preventive healthcare becomes a greater priority globally. Early detection of B12 deficiency can prevent serious health complications, and active B12 testing provides a more accurate assessment, which is essential for timely intervention. Many healthcare systems and providers are recognizing the value of incorporating active B12 tests into regular screenings, especially for high-risk populations such as older adults, individuals with dietary restrictions, and those with conditions affecting nutrient absorption. Additionally, with the rise of at-home diagnostics and telemedicine, there is potential for the development of simplified, user-friendly active B12 testing kits that patients can use outside of clinical settings. This trend toward preventive healthcare, coupled with technological advancements in point-of-care testing, positions the active B12 test market for expansion. Companies focusing on making active B12 testing more accessible and cost-effective for routine use are well-positioned to capture a growing share of this market.

Active B12 Test Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into reagents & kits, analyzers, and consumables.

The reagents & kits segment accounted for the largest revenue of the total active B12 test market share in 2024.

- Reagents & kits are essential for the accurate detection of active B12 levels, which are critical in diagnosing deficiencies and related disorders.

- These kits are widely used in hospitals, diagnostic laboratories, and research institutes due to their compatibility with various immunoassay technologies, such as ELISA and CLIA.

- The convenience of pre-packaged kits and their role in ensuring consistent and reliable test results drive their high demand in the market.

- Increasing awareness of B12 deficiencies and the availability of high-quality reagents have further strengthened this segment's dominance.

- Therefore, the analysis of segmental trends shows that reagents & kits lead the market due to their widespread use in diagnostics and their compatibility with various assay technologies, driving the active B12 test market growth.

The analyzers segment is anticipated to register the fastest CAGR during the forecast period.

- Analyzers play a crucial role in automating and streamlining the active B12 testing process, providing quick and accurate results.

- As laboratories and diagnostic centers move towards high-throughput testing, the demand for advanced analyzers with enhanced accuracy and speed is increasing.

- Additionally, advancements in analyzer technology, such as integration with CLIA and ELISA platforms, are driving the segment.

- The trend towards automation in diagnostics and the growing need for high-efficiency testing solutions contribute to the rapid growth of this segment.

- Thus, the segmental trends depict that analyzers are expected to grow rapidly, driven by the increasing need for high-throughput, automated testing solutions that enhance efficiency and accuracy in active B12 diagnostics, boosting the active B12 test market trends.

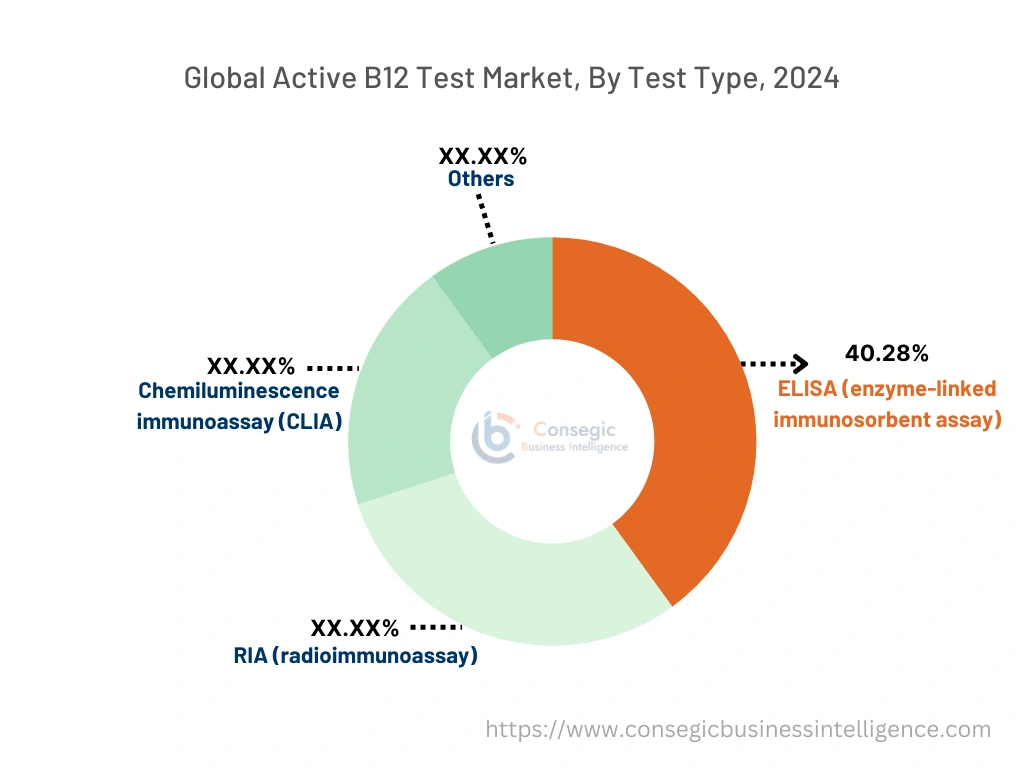

By Test Type:

Based on test type, the market is segmented into ELISA (enzyme-linked immunosorbent assay), RIA (radioimmunoassay), chemiluminescence immunoassay (CLIA), and others.

The ELISA segment accounted for the largest revenue share of 40.28% in 2024.

- ELISA is a widely used method in active B12 testing due to its accuracy, reliability, and ability to detect even low concentrations of active B12 in blood samples.

- This method is extensively adopted in diagnostic laboratories and hospitals, where precise and efficient testing is required for diagnosing B12-related deficiencies.

- The low cost, ease of use, and standardization associated with ELISA kits make it a preferred choice among healthcare providers. Its versatility in being used across various indications, such as pernicious anemia and neurological disorders, further supports its leading market position.

- Thus, the market trends analysis shows that ELISA leads the market due to its accuracy, cost-effectiveness, and wide adoption in clinical settings, boosting the active B12 test market demand.

The CLIA segment is anticipated to register the fastest CAGR during the forecast period.

- CLIA technology is increasingly favored in high-throughput settings due to its enhanced sensitivity, faster turnaround times, and compatibility with automation.

- CLIA's ability to deliver precise results efficiently makes it ideal for large diagnostic centers handling high test volumes.

- The rising demand for automated, high-sensitivity testing solutions in larger healthcare facilities and research institutions is propelling the CLIA segment.

- Additionally, CLIA's versatility in integrating with advanced analyzer systems is enhancing its adoption in the market.

- Therefore, the segmental trends portray that CLIA is expected to grow rapidly, driven by its high sensitivity, quick processing times, and suitability for automation, making it highly valuable for high-throughput diagnostic environments, creating lucrative active B12 test market opportunities.

By Indication:

Based on indication, the market is segmented into pernicious anemia, folate deficiency, vitamin B12 deficiency, neurological disorders, and others.

The vitamin B12 deficiency segment accounted for the largest revenue of the overall active B12 test market share in 2024.

- Vitamin B12 deficiency is a common condition with potentially severe health implications, including anemia and neurological issues.

- Active B12 testing is crucial for the accurate diagnosis of B12 deficiency, allowing for early intervention and management.

- The rising incidence of B12 deficiency due to dietary habits, especially in vegan and elderly populations, is driving demand for active B12 testing.

- Additionally, increased awareness about the impact of B12 deficiency on overall health has led to higher testing rates in both developed and developing regions.

- Hence, Vitamin B12 deficiency leads the market as the primary indication for testing, driven by the rising incidence of deficiency-related health issues and the need for early, accurate diagnosis, propelling the active B12 test market expansion.

The neurological disorders segment is anticipated to register the fastest CAGR during the forecast period.

- Neurological disorders, often linked to vitamin B12 deficiency, require precise diagnostic measures to prevent long-term complications.

- Active B12 testing helps in identifying B12-related neurological issues, enabling timely treatment and management.

- With an aging population and the rising incidence of neurodegenerative diseases, demand for active B12 testing in neurological applications is expected to grow significantly.

- The segment is further supported by ongoing research highlighting the connection between B12 levels and cognitive health, which has prompted increased testing in at-risk populations.

- Therefore, the neurological disorders segment is expected to grow rapidly, driven by the need for early diagnosis of B12-related neurological conditions and the growing awareness of B12's role in cognitive health, boosting the active B12 test market trends.

By End-User:

Based on end-users, the Active B12 Test market is segmented into hospitals, diagnostic laboratories, research institutes, specialty clinics, and others.

The diagnostic laboratories segment accounted for the largest revenue share in 2024.

- Diagnostic laboratories are the primary providers of active B12 testing, handling a high volume of tests due to their specialized infrastructure and capabilities for advanced testing methods like ELISA, RIA, and CLIA.

- These laboratories serve as referral centers for hospitals and clinics, processing large batches of samples with high precision.

- The central role of diagnostic laboratories in healthcare, coupled with their ability to provide efficient, accurate, and high-throughput testing, has established them as the largest segment in the active B12 testing market.

- Diagnostic laboratories lead the market as the main providers of active B12 testing, supported by their specialized infrastructure and capacity for high-throughput, accurate testing.

The hospital segment is anticipated to register the fastest CAGR during the forecast period.

- Hospitals are increasingly adopting active B12 testing due to the rising number of in-patient cases related to B12 deficiency and associated health complications.

- Many hospitals are integrating advanced diagnostic equipment to offer on-site B12 testing, reducing turnaround times and improving patient care.

- The increasing adoption of active B12 testing in hospital settings for rapid diagnosis, particularly in emergency care, is driving the segment.

- As per the active B12 test market analysis, hospitals are expected to grow rapidly as they increasingly adopt active B12 testing for in-patient care and rapid diagnostics, supporting timely intervention and enhanced patient outcomes.

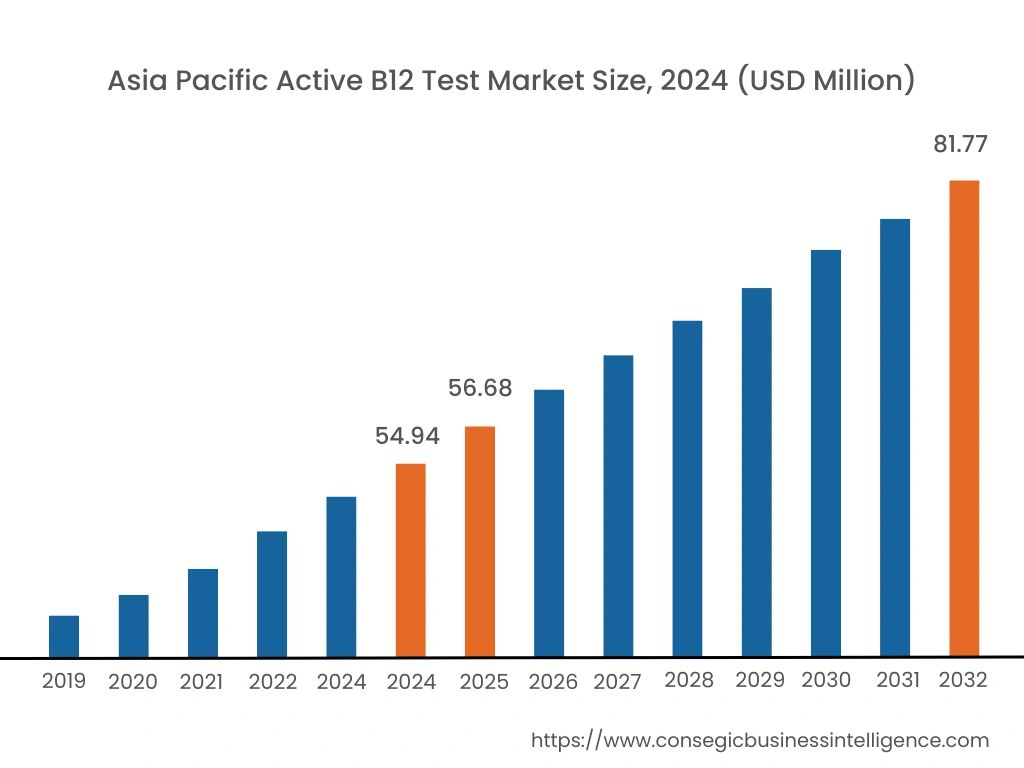

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

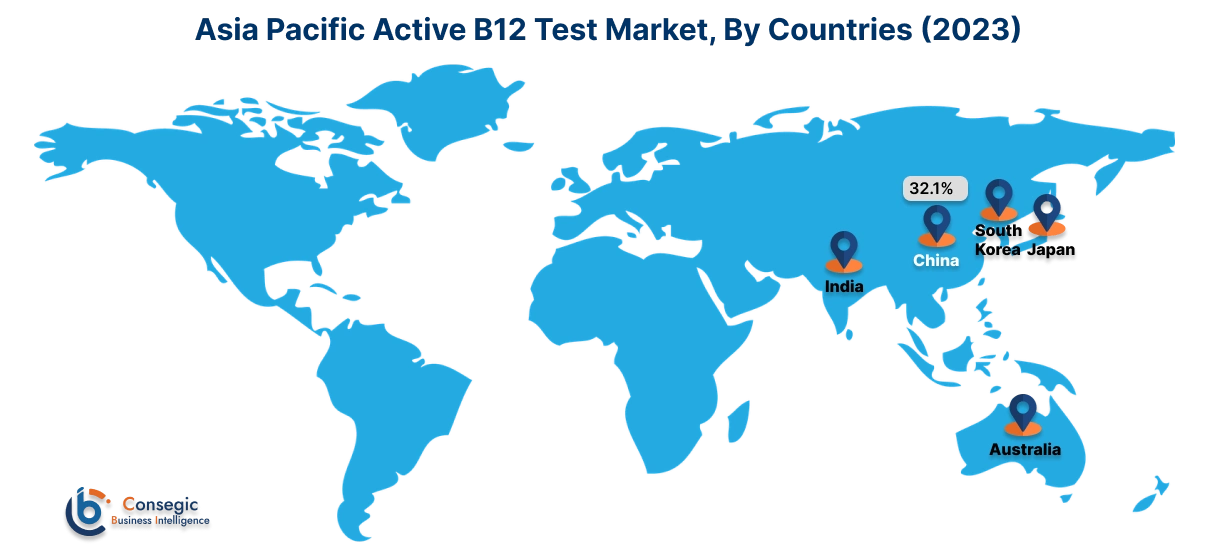

Asia Pacific region was valued at USD 54.94 Million in 2024. Moreover, it is projected to reach over USD 81.77 Million by 2032. Out of this, China accounted for 32.1% of the total market share. Asia-Pacific is witnessing the fastest growth in the market, driven by increasing healthcare investments and improving diagnostic capabilities in countries like China, Japan, and India. The rising prevalence of vitamin B12 deficiencies and growing awareness among healthcare professionals contribute to market expansion. Government initiatives to improve healthcare infrastructure and access to diagnostics further support growth. However, challenges such as limited access to specialized care in rural areas and affordability issues may impede the uptake of advanced diagnostic tests.

North America holds a substantial share of the market, primarily due to a well-established healthcare infrastructure and high awareness levels. The United States, in particular, has a significant patient population and access to advanced diagnostic options, including enzyme immunoassays and ELISA assays. The presence of major diagnostic companies investing in research and development further propels market growth. However, the high cost of testing and potential side effects may pose challenges to market expansion.

Europe represents a significant portion of the global market, with countries like Germany, France, and the UK leading in terms of diagnosis and treatment. The region benefits from strong government support for rare disease management and a robust healthcare system. Ongoing clinical trials and research efforts are enhancing the adoption of novel diagnostic methods. However, stringent regulatory frameworks and high costs associated with advanced diagnostics could challenge rapid market growth.

The active B12 test market analysis shows that the Middle East & Africa region shows promising potential in the market, particularly in countries like Saudi Arabia, the UAE, and South Africa. Increasing healthcare investments and rising incidences of vitamin B12 deficiencies drive the demand for advanced diagnostic options. The expanding medical tourism sector, particularly in the UAE, where high-quality diagnostics are offered, further supports market growth. Nonetheless, limited local manufacturing capabilities and the high cost of diagnostics remain barriers to broader market penetration in this region.

Latin America is an emerging market, with Brazil and Mexico being the primary growth drivers. The rising prevalence of vitamin B12 deficiencies and increasing focus on improving healthcare infrastructure contribute to the market's expansion. Government initiatives aimed at enhancing access to advanced diagnostics, combined with the region's increasing awareness of vitamin B12 deficiencies, support market growth. However, economic constraints and unequal access to advanced healthcare technologies in some areas present challenges to market development in this region.

Top Key Players & Market Share Insights:

The active B12 test market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global active B12 test market. Key players in the active B12 test industry include -

- Axis-Shield Diagnostics (UK)

- Abbott Laboratories (USA)

- Siemens Healthineers (Germany)

- Roche Diagnostics (Switzerland)

- LifeSpan BioSciences, Inc. (USA)

- Demeditec Diagnostics GmbH (Germany)

- DiaSorin S.p.A. (Italy)

Recent Industry Developments :

Product Launches:

- In April 2024, Abbott introduced a new Active B12 Test kit, offering improved accuracy and user-friendliness in clinical settings. This advanced assay technology ensures faster, more reliable results, reinforcing Abbott's commitment to enhancing patient care and capturing a larger share of the B12 testing market.

- In August 2021, OmegaQuant, known for its nutritional status tests for omega-3 fatty acids and vitamin D, announced the launch of a new at-home test to measure vitamin B12 levels. This convenient test detects methylmalonic acid (uMMA), which OmegaQuant identifies as the most accurate indicator for assessing low B12 status—higher uMMA levels suggest a greater likelihood of B12 deficiency.

Mergers and Acquisitions:

- In February 2024, Siemens merged with a leading diagnostics company to strengthen its position in the Active B12 Test sector. The merger combines both companies' expertise and market reach to drive innovation and enhance product offerings, aiming to provide healthcare providers with superior diagnostic tools.

- Axis-Shield Diagnostics announced the acquisition of a prominent biotech firm focused on vitamin deficiency diagnostics. This move is set to expand their Active B12 Test portfolio and enhance R&D, positioning the company to meet the growing demand for more advanced diagnostic solutions.

Active B12 Test Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 268.55 Million |

| CAGR (2025-2032) | 4.7% |

| By Product Type |

|

| By Test Type |

|

| By Indication |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the active B12 test Market? +

In 2024, the active B12 test market was USD 186.55 million.

What will be the potential market valuation for the active B12 test by 2032? +

In 2032, the market size of active B12 test is expected to reach USD 268.55 Million.

What are the segments covered in the active B12 test market report? +

The product type, test type, indication, and end-user are the segments covered in this report.

Who are the major players in the active B12 test market? +

Axis-Shield Diagnostics (UK), Abbott Laboratories (USA), Siemens Healthineers (Germany), DiaSorin S.p.A. (Italy), Roche Diagnostics (Switzerland), LifeSpan BioSciences, Inc. (USA), Demeditec Diagnostics GmbH (Germany) are the major players in the active B12 test market.