- Summary

- Table Of Content

- Methodology

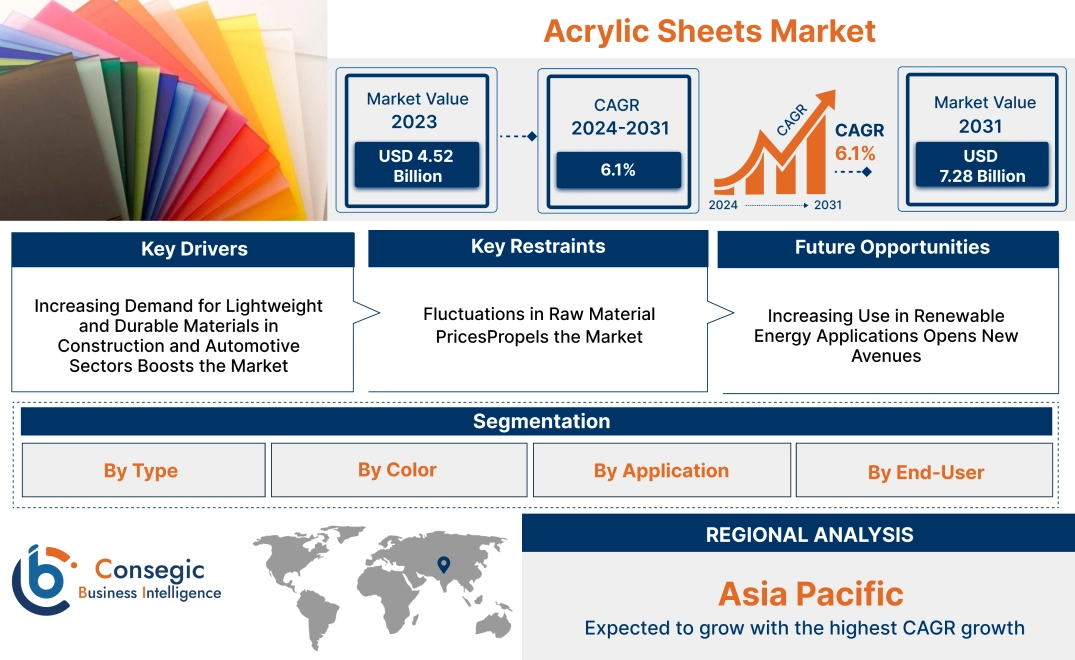

Acrylic Sheets Market Size:

Acrylic Sheets Market size is estimated to reach over USD 7.28 Billion by 2031 from a value of USD 4.52 Billion in 2023 and is projected to grow by USD 4.72 Billion in 2024, growing at a CAGR of 6.1% from 2024 to 2031.

Acrylic Sheets Market Scope & Overview:

Acrylic sheets are transparent plastic materials made from polymethyl methacrylate (PMMA), known for their high durability, lightweight nature, and superior optical clarity. These sheets serve as an alternative to glass in various applications due to their shatter-resistant properties and ease of fabrication. They are widely used in industries such as construction, automotive, signage, and interior design for applications including windows, skylights, displays, and protective barriers. Their flexibility in terms of customization and color options further enhances their appeal across different sectors. Technological advancements in manufacturing processes have improved the quality and versatility of these sheets, further supporting the market. End-use industries, including construction, automotive, and signage, are leading adopters, as acrylic sheets continue to be favored for their strength, clarity, and cost-effectiveness.

Acrylic Sheets Market Dynamics - (DRO) :

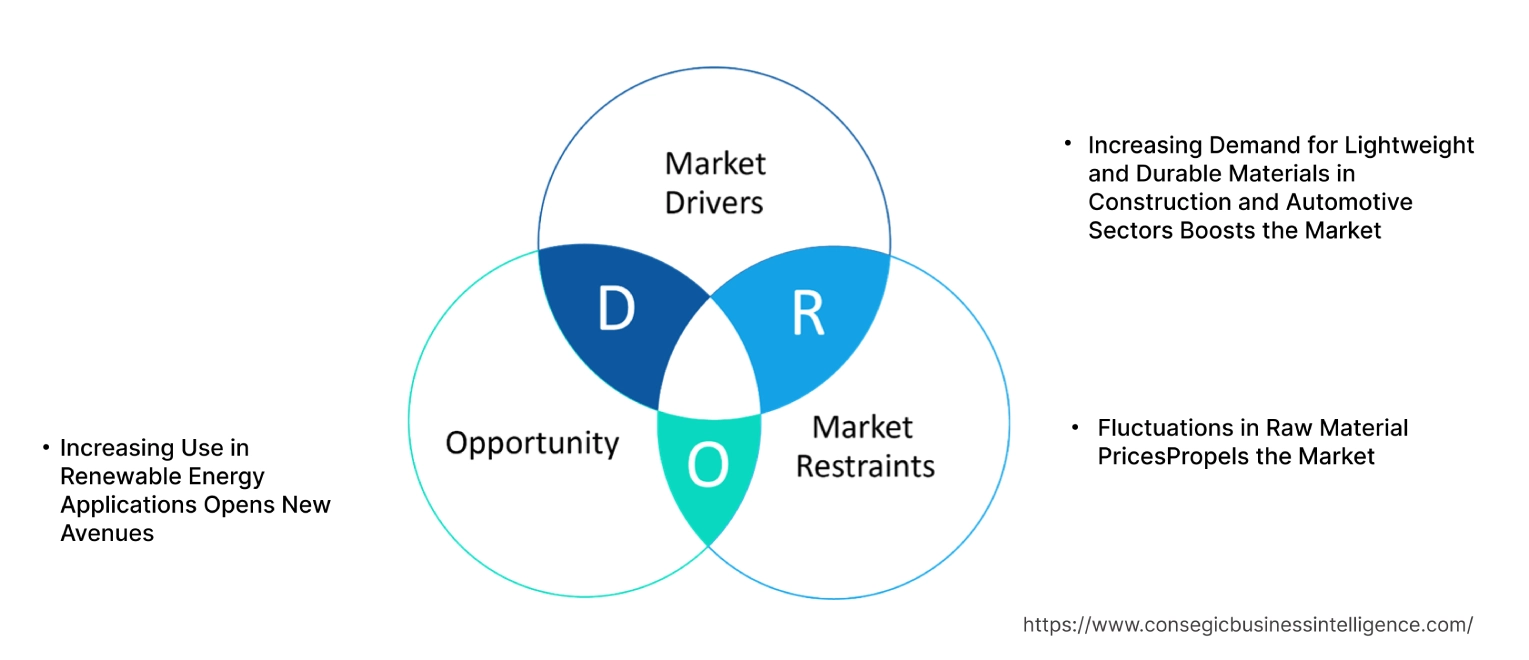

Key Drivers:

Increasing Demand for Lightweight and Durable Materials in Construction and Automotive Sectors Boosts the Market

The rising demand for lightweight, durable, and versatile materials in the construction and automotive sectors is a major driver of the acrylic sheets market demand. These sheets offer a high degree of clarity, strength, and impact resistance, making them an ideal alternative to glass in various applications such as windows, partitions, skylights, and displays. The growing emphasis on energy efficiency and modern design trends in construction has accelerated the adoption of the sheets, particularly in commercial and residential projects. Additionally, in the automotive industry, the shift towards lighter materials to improve fuel efficiency and reduce emissions has spurred the use of the sheets in vehicle components like windows, lighting, and interior panels. Their ability to withstand environmental stress without yellowing or cracking makes them an attractive option in industries focused on both aesthetics and functionality.

Key Restraints :

Fluctuations in Raw Material Prices Propels the Market

The acrylic sheets market faces significant challenges due to the volatility in raw material prices, particularly polymethyl methacrylate (PMMA), the primary component of these sheets. The price of PMMA is closely linked to crude oil prices, as it is derived from petrochemicals. Fluctuations in oil prices, driven by geopolitical tensions, supply-demand imbalances, and regulatory policies, directly affect the production costs of these sheets. This price instability makes it difficult for manufacturers to maintain stable pricing strategies, especially in competitive markets. Furthermore, the high production cost of these sheets compared to alternatives like polycarbonate and glass has led some manufacturers and end-users to opt for more cost-effective materials, restraining acrylic sheets market growth.

Future Opportunities :

Increasing Use in Renewable Energy Applications Opens New Avenues

The growing focus on renewable energy, particularly solar energy, presents acrylic sheets market opportunities. Acrylic sheets are increasingly being used in the production of solar panels and photovoltaic modules due to their excellent light transmission and weather resistance properties. These sheets enhance the efficiency of solar energy systems by providing a durable, transparent cover that protects the delicate components from environmental damage while allowing maximum light penetration. With the global shift toward sustainable energy solutions and the increasing investment in solar energy infrastructure, the adoption of high-performance acrylic sheets in the sector is expected to rise. Manufacturers that develop specialized acrylic sheets tailored for renewable energy applications are well-positioned to capitalize on the expanding market segment.

Acrylic Sheets Market Segmental Analysis :

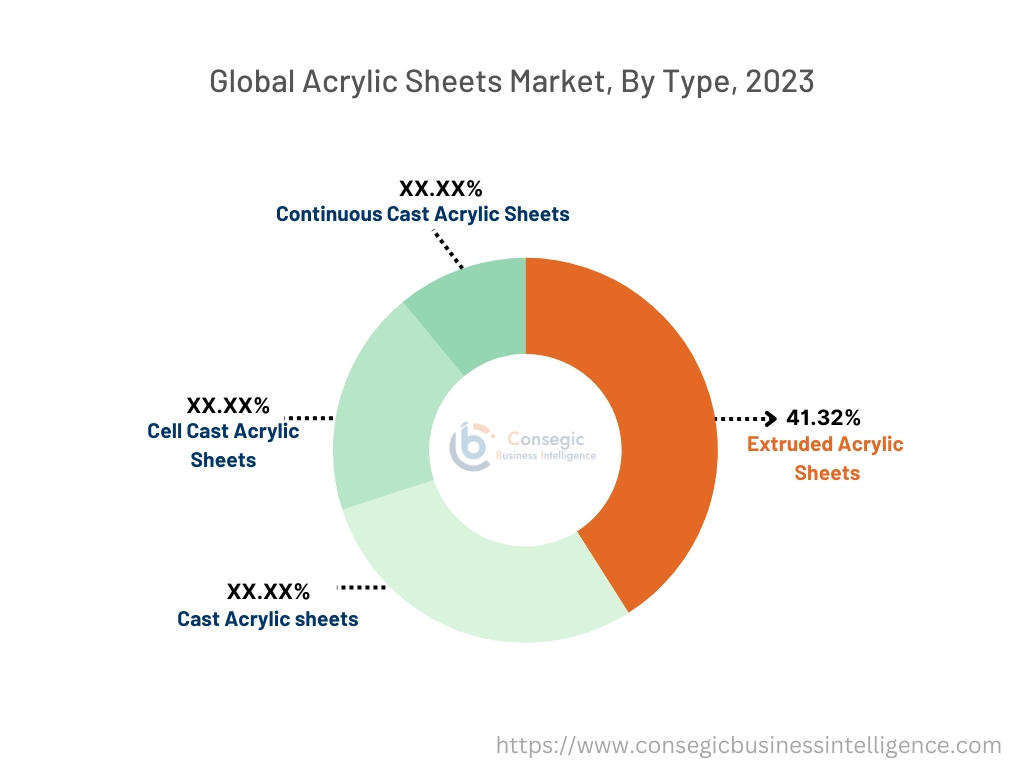

By Type:

Based on type, the market is segmented into extruded acrylic sheets, cast acrylic sheets, cell cast acrylic sheets, and continuous cast acrylic sheets.

The extruded acrylic sheets segment accounted for the largest revenue share of 41.32% in 2023.

- Extruded acrylic sheets are favored for their consistent thickness, lower cost, and ease of fabrication, making them a popular choice for a variety of applications such as signage, displays, and construction.

- The controlled manufacturing process of extruded sheets results in less material waste and better cost-efficiency, which appeals to industries focused on high-volume production.

- Additionally, the versatility of these sheets in creating custom shapes and sizes further drives their adoption across multiple sectors.

- Thus, the market trends analysis shows that extruded sheets dominate the market due to their cost-effectiveness, ease of fabrication, and widespread use in high-volume applications like signage and construction, boosting the acrylic sheets market demand.

The cell cast acrylic sheets segment is anticipated to register the fastest CAGR during the forecast period.

- Cell cast acrylic sheets offer superior optical clarity and higher molecular weight compared to extruded acrylic sheets, making them ideal for applications requiring premium aesthetics and durability.

- These sheets are particularly favored in industries such as automotive, architecture, and luxury signage, where quality and appearance are critical.

- The increasing demand for high-quality, aesthetically appealing materials, particularly in luxury retail and automotive displays, is expected to drive the segment.

- Hence, the segmental trends analysis depicts that the cell cast sheets are expected to grow rapidly due to their superior optical clarity and use in high-end applications where aesthetics and durability are essential, propelling the acrylic sheets market trends.

By Color:

Based on color, the market is segmented into transparent, opaque, and translucent.

The transparent segment accounted for the largest revenue of the total acrylic sheets market share in 2023.

- Transparent acrylic sheets are widely used in applications requiring high optical clarity, such as display cases, protective barriers, and windows.

- Their lightweight nature and shatter resistance make them a preferred alternative to glass in many industries, including retail, construction, and transportation.

- The rising usage of transparent sheets in protective applications, particularly in response to the COVID-19 pandemic, has further driven the adoption of this segment.

- Additionally, their use in signage, where visibility and clarity are paramount, reinforces the dominance of the transparent segment.

- Thus, the acrylic sheets market analysis shows that transparent sheets lead the market due to their high optical clarity, shatter resistance, and increasing demand in both protective and display applications.

The translucent segment is anticipated to register the fastest CAGR during the forecast period.

- Translucent acrylic sheets offer a balance between light diffusion and opacity, making them ideal for applications such as lighting fixtures, privacy panels, and illuminated signage.

- The growing trend of using illuminated signage in commercial spaces, retail outlets, and public infrastructure is a key driver for this segment.

- Additionally, the use of translucent sheets in modern interior design, where lighting plays a crucial aesthetic role, is contributing to the segment's growth.

- Therefore, as per the market trends, translucent sheets are expected to grow rapidly due to their increasing use in illuminated signage and interior design applications where light diffusion is essential, driving the acrylic sheets market expansion.

By Application:

Based on application, the market is segmented into signage & displays, transportation, building, furniture & interior design, electronics devices, medical devices, and others.

The signage & displays segment accounted for the largest revenue share in 2023.

- Acrylic sheets are widely used in signage and display applications due to their optical clarity, weather resistance, and ease of customization.

- They are commonly used in advertising boards, illuminated signs, and retail displays, where visibility and aesthetics are crucial.

- The rising demand for advertising and promotional signage in retail, transportation hubs, and commercial spaces is driving the segment.

- Additionally, the versatility of these sheets in being molded into various shapes and sizes further supports their widespread adoption in the signage industry.

- The segment trends depicts that the signage & displays segment dominates the market as acrylic sheets offer high visibility, weather resistance, and versatility, making them ideal for advertising and promotional applications.

The transportation segment is anticipated to register the fastest CAGR during the forecast period.

- Acrylic sheets are increasingly used in the transportation industry for applications such as windows, windshields, and interior partitions in vehicles, boats, and aircraft.

- Their lightweight, shatter-resistant properties make them an attractive alternative to glass, particularly in aviation and automotive sectors where weight reduction is critical for fuel efficiency.

- Additionally, the use of these sheets in electric vehicles (EVs), where lightweight materials are essential for extending battery life, is further boosting this segment's growth.

- Thus, the transportation segment is expected to grow rapidly, driven by the increasing use of lightweight, shatter-resistant acrylic sheets in vehicles and aircraft to improve fuel efficiency and safety, boosting the acrylic sheets market trends.

By End-User:

Based on application, the acrylic sheets market is segmented into building, furniture & interior design, electronics devices, medical devices, and others.

The building segment accounted for the largest revenue share in 2023.

- Acrylic sheets are extensively used in the building and construction sector for windows, skylights, doors, and partitions due to their durability, weather resistance, and aesthetic appeal.

- The increasing use of the sheets in modern architectural designs, where transparency and light transmission are key elements, is driving the segment.

- Additionally, their use as a lightweight alternative to glass in both residential and commercial buildings contributes to the segment.

- Thus, as per the analysis, the building segment leads the market, driven by the increasing adoption of acrylic sheets in modern architectural designs, where durability and aesthetic appeal are critical.

The electronics devices segment is anticipated to register the fastest CAGR during the forecast period.

- Acrylic sheets are increasingly being used in electronics devices for display screens, protective covers, and electronic enclosures.

- Their optical clarity, scratch resistance, and ability to withstand impact make them ideal for protecting delicate electronic components.

- The growing demand for consumer electronics, such as smartphones, tablets, and televisions, is driving the adoption of the sheets in this segment.

- Additionally, advancements in display technologies, including touchscreens and OLED displays, further boost the use of acrylic sheets in the electronics industry.

- Therefore, the market analysis shows that the electronics devices segment is expected to grow rapidly, driven by the rising usage for the sheets in consumer electronics for display screens and protective covers, where clarity and impact resistance are essential, proliferating the acrylic sheets market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

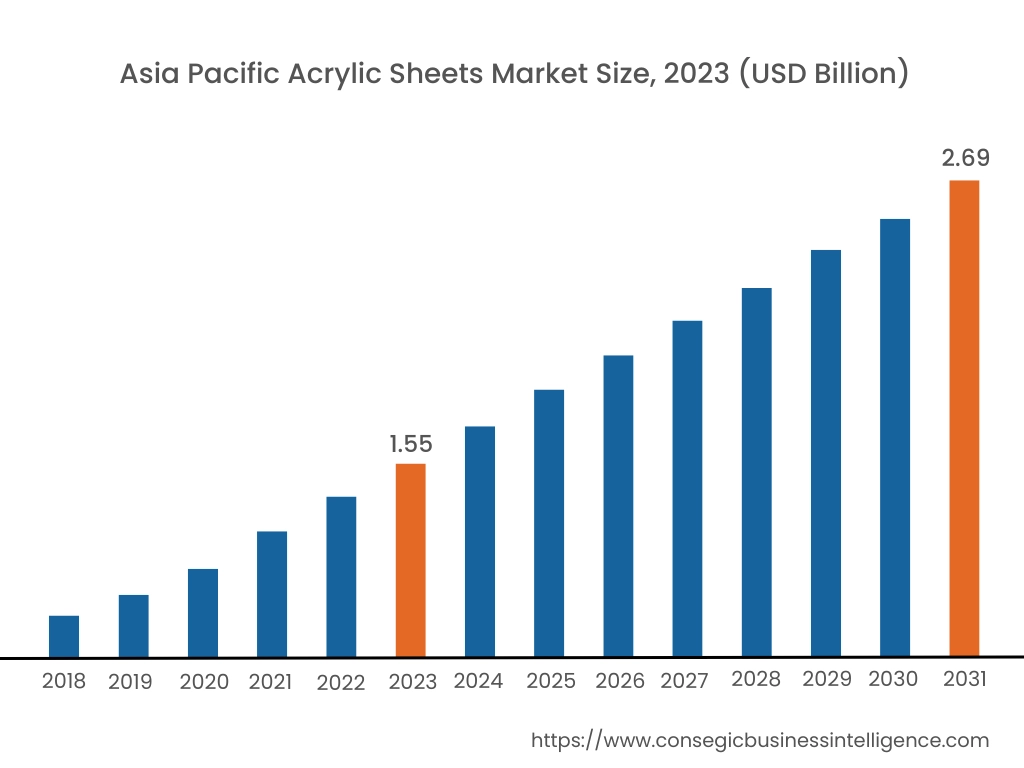

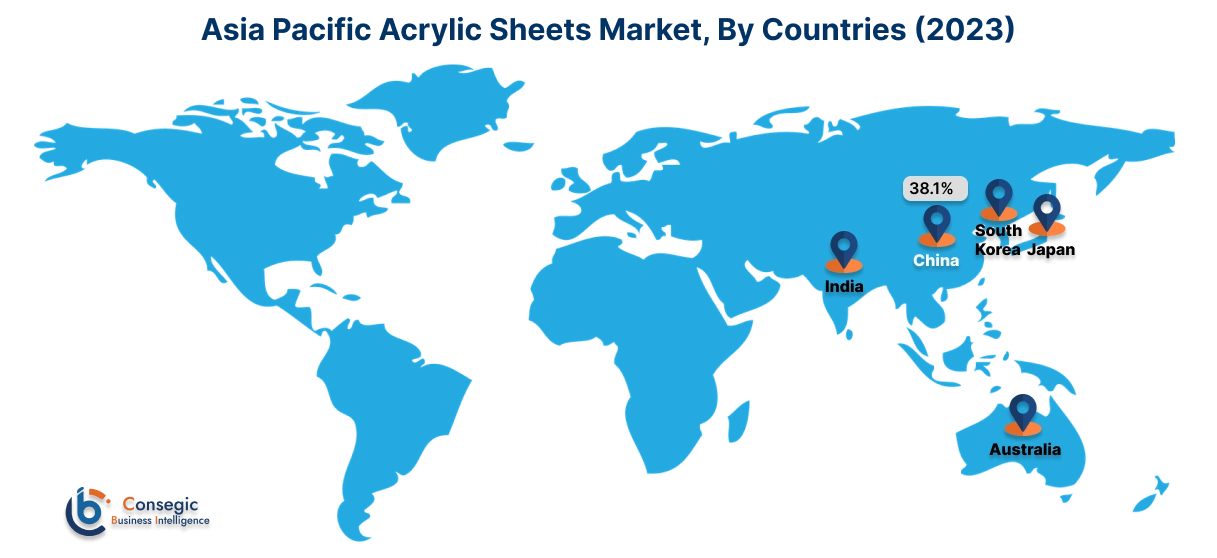

Asia Pacific region was valued at USD 1.55 Billion in 2023. Moreover, it is projected to grow by USD 1.63 Billion in 2024 and reach over USD 2.69 Billion by 2031. Out of this, China accounted for 38.1% of the total market share. As per the acrylic sheets market analysis, Asia-Pacific is the fastest-growing region, with China, Japan, and India leading the market due to rapid urbanization and industrialization. The growing construction sector, increasing demand for signage and displays, and the expansion of automotive and electronics manufacturing are driving the market. China's dominance in manufacturing and lower production costs also contribute to market expansion. However, fluctuating raw material prices and environmental concerns around plastic waste are key challenges for the region.

North America holds a substantial share of the market, driven by demand from industries such as construction, automotive, signage, and advertising. The U.S. leads in market adoption due to its widespread use in architectural applications, particularly for interior design and glazing. The automotive sector's focus on lightweight materials has further boosted the market. However, competition from glass alternatives and increasing environmental regulations around plastic use pose challenges for market growth.

Europe is a key player in the market, with countries like Germany, the UK, and France being significant contributors. The region's market is driven by demand in construction, retail displays, and automotive sectors, especially with the rising focus on energy-efficient buildings. The European Green Deal and sustainability trends have increased the use of the sheets in renewable energy projects, particularly in solar panel covers. However, stringent environmental regulations around plastic usage and recycling can affect the market's growth trajectory.

The Middle East & Africa region is experiencing steady growth in the market, particularly driven by construction and infrastructural development in countries like the UAE and Saudi Arabia. The demand for the sheets in architectural projects, particularly in luxury and modern infrastructure, supports market development. Additionally, the region's growing tourism industry increases demand for signage and display applications. However, limited local production capabilities and dependency on imports may hinder market growth in some areas.

Latin America is an emerging market, led by Brazil and Mexico. The region's demand is driven by construction, advertising, and automotive industries. Brazil's growing infrastructure projects, along with increasing demand for lightweight and durable materials in the automotive sector, are driving market growth. Mexico's strong manufacturing base also contributes to demand in various industries. However, economic instability and inconsistent regulatory frameworks across the region pose challenges for the market.

Top Key Players & Market Share Insights:

The acrylic sheets market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global acrylic sheets market. Key players in the acrylic sheets industry include -

- Altuglas International (France)

- Evonik Industries AG (Germany)

- Mitsubishi Chemical Corporation (Japan)

- Plaskolite, LLC (USA)

- Lucite International (UK)

- 3A Composites Holding AG (Switzerland)

- Asia Poly Industrial Sdn Bhd (Malaysia)

- Aristech Surfaces LLC (USA)

- PolyOne Corporation (USA)

- Madreperla S.p.A. (Italy)

Recent Industry Developments :

Product Launch:

- In April 2024, Unisub, launched Unisub Sublimation Acrylic panels. These precision-engineered acrylic panels are specifically designed to enable vibrant and striking sublimation printing.

Mergers and Acquisitions:

- In July 2021, materials supplier Trinseo completed the acquisition of Aristech Surfaces LLC for USD 445 million. This acquisition enables Trinseo to expand its range of polymethyl methacrylates (PMMA) technology.

- In June 2021, Trinseo acquired Aristech Surfaces LLC for USD 445 million, a deal facilitated by Falcon Private Holdings. This acquisition aimed to enhance Trinseo's portfolio in polymer resins and plastic sheets, leveraging the existing workforce and management of Aristech Surfaces LLC, which has a valuation of USD 1.4 billion.

Acrylic Sheets Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 7.28 Billion |

| CAGR (2024-2031) | 6.1% |

| By Material Type |

|

| By Color |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Acrylic Sheets Market? +

Acrylic Sheets Market size is estimated to reach over USD 7.28 Billion by 2031 from a value of USD 4.52 Billion in 2023 and is projected to grow by USD 4.72 Billion in 2024, growing at a CAGR of 6.1% from 2024 to 2031.

What are the primary uses of acrylic sheets? +

Acrylic sheets are widely used in applications such as signage, automotive parts, construction materials, and furniture due to their high transparency, weather resistance, and ease of fabrication. They are also frequently used as an alternative to glass in various industries.

Which region is expected to experience the highest growth in the Acrylic Sheets Market? +

The Asia-Pacific region is expected to experience the highest growth, driven by rapid industrialization, infrastructure development, and increased usage in sectors like automotive, construction, and advertising, particularly in countries like China and India.

What are the key trends influencing the Acrylic Sheets Market? +

Key trends include the rising demand for lightweight materials in automotive and aerospace industries and the shift towards eco-friendly and recyclable acrylic sheets. Manufacturers are also focusing on developing high-performance variants that offer improved scratch resistance and UV protection.