- Summary

- Table Of Content

- Methodology

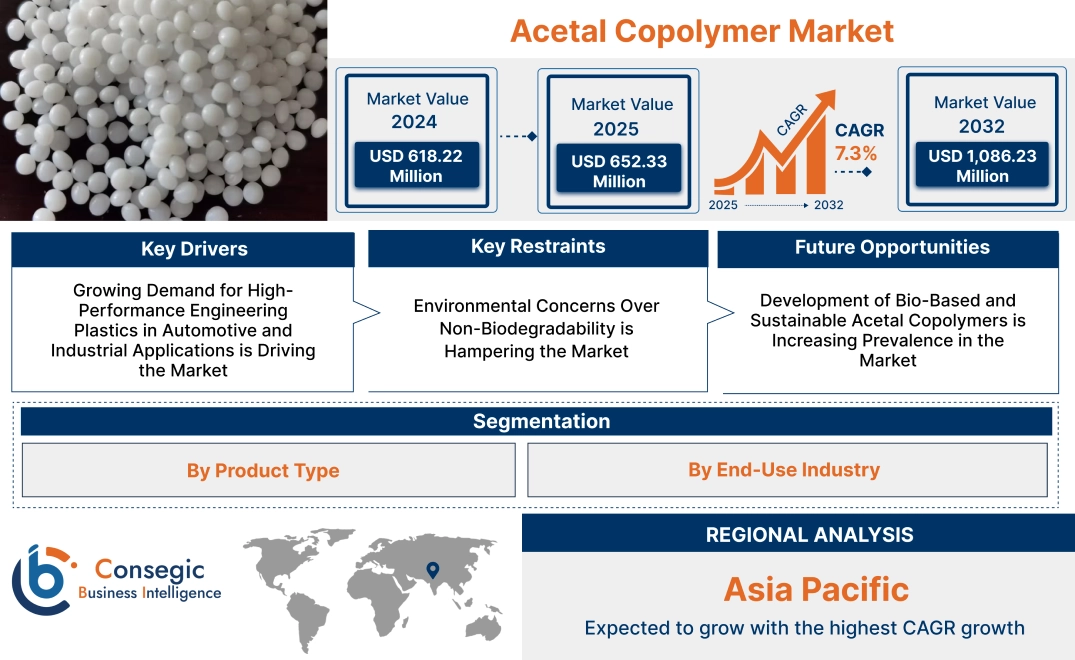

Acetal Copolymer Market Size:

Acetal Copolymer Market size is estimated to reach over USD 1,086.23 Million by 2032 from a value of USD 618.22 Million in 2024 and is projected to grow by USD 652.33 Million in 2025, growing at a CAGR of 7.3% from 2025 to 2032.

Acetal Copolymer Market Scope & Overview:

The acetal copolymer focuses on high-performance engineering thermoplastics known for their excellent mechanical properties, dimensional stability, and resistance to wear and chemicals. Acetal copolymers, commonly referred to as polyoxymethylene (POM), are used in various industrial applications requiring durability and precision. Its key characteristics include low friction, high stiffness, and excellent thermal stability, making them suitable for replacing metals in demanding environments. Their benefits range from lightweight solutions and reduced maintenance costs to enhanced durability in harsh conditions. Applications span automotive components, consumer goods, industrial machinery, and medical devices, where precision engineering and reliability are critical. End-users include automotive manufacturers, electronics producers, and industrial equipment manufacturers, driven by increasing growth for lightweight and cost-effective materials, advancements in manufacturing technologies, and rising industrial automation.

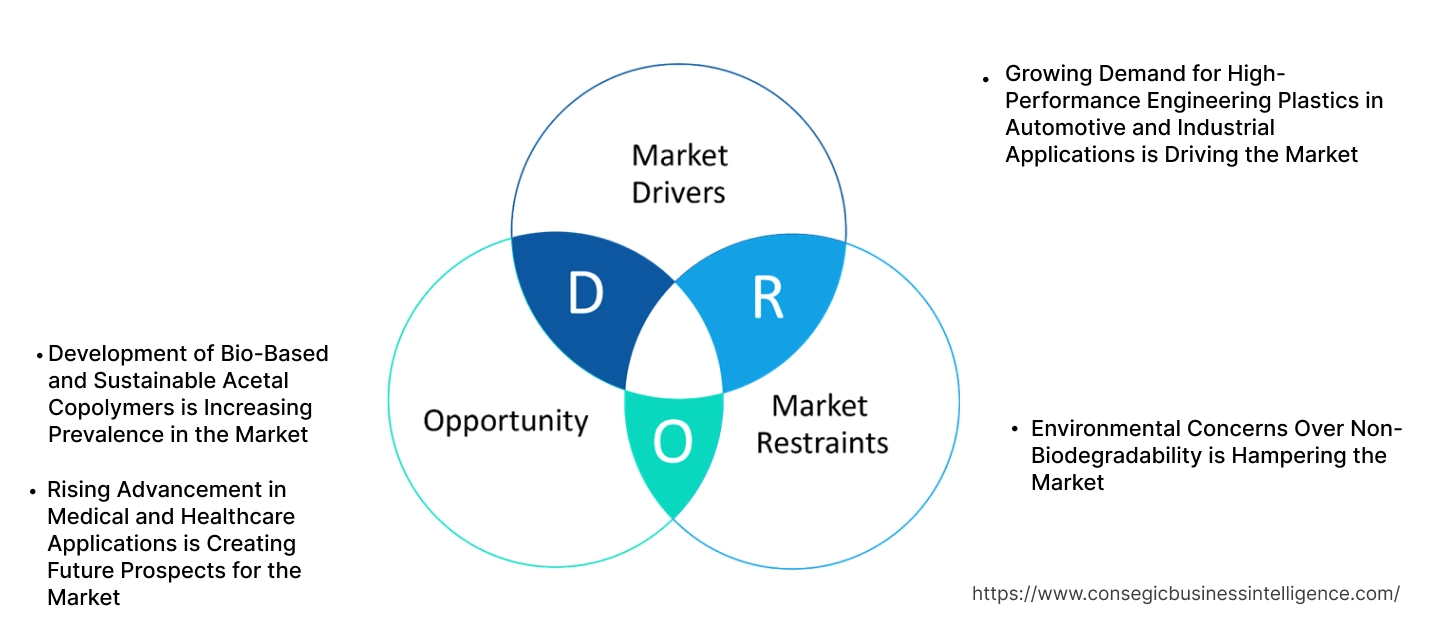

Acetal Copolymer Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for High-Performance Engineering Plastics in Automotive and Industrial Applications is Driving the Market

The increasing reliance on acetal copolymers in automotive and industrial applications is significantly shaping the market. They are known for their high stiffness, excellent wear resistance, and low friction properties, and are becoming indispensable in manufacturing lightweight and durable components such as gears, bushings, and fuel system parts. In the automotive sector, these materials are widely used to reduce vehicle weight, thereby improving fuel efficiency and lowering emissions, aligning with global trends toward sustainability and efficiency in transportation.

In industrial applications, they provide solutions for demanding environments where components are subjected to mechanical stress, chemical exposure, or high temperatures. Industries such as electronics, packaging, and machinery benefit from the material's dimensional stability and resistance to deformation, making it an ideal choice for critical parts. As manufacturers continue to prioritize performance and longevity, the acetal copolymer market expansion is expected in various high-performance applications.

Key Restraints:

Environmental Concerns Over Non-Biodegradability is Hampering the Market

Despite their advantages, the non-biodegradable nature of acetal copolymers presents significant environmental challenges. Derived from petroleum-based sources, these materials contribute to plastic waste, raising concerns in regions with stringent environmental regulations and increasing public awareness of sustainability. Their inability to decompose naturally adds to the burden on landfills and recycling systems, making them a less favorable choice in industries focusing on eco-friendly practices.

Moreover, the rising scrutiny of single-use plastics and the push for greener alternatives are encouraging trends for industries to explore bio-based or fully recyclable materials. This shift puts competitive pressure on them, particularly in applications where environmentally sustainable options are becoming a priority. Addressing these concerns through innovations in production processes and recycling technologies is crucial to maintaining the market's relevance in an eco-conscious world.

Future Opportunities :

Development of Bio-Based and Sustainable Acetal Copolymers is Increasing Prevalence in the Market

The growing emphasis on sustainability and environmental responsibility is driving innovation in bio-based and sustainable acetal copolymers. Manufacturers are investing in the development of materials derived from renewable sources, such as plant-based feedstocks, to reduce dependency on petroleum-based inputs. These bio-based alternatives offer comparable mechanical and chemical properties to conventional ones while aligning with global trends toward greener manufacturing practices.

Additionally, advancements in recycling technologies are enabling the production of circular economy-friendly copolymers. Processes that facilitate efficient recovery and reuse of these materials are helping manufacturers address environmental concerns while retaining the performance characteristics demanded by end-users. As industries and consumers alike prioritize sustainability, the development of bio-based and recyclable versions represents a promising avenue for acetal copolymer market opportunity and innovation.

Rising Advancement in Medical and Healthcare Applications is Creating Future Prospects for the Market

The medical and healthcare sectors are emerging as significant markets for acetal copolymers due to their unique properties, including biocompatibility, dimensional stability, and resistance to chemicals. These materials are increasingly used in the production of precision medical devices, such as inhalers, surgical instruments, and diagnostic equipment, where accuracy and durability are critical.

The expansion of disposable medical products, such as syringes and insulin pens, is also driving its adoption. Their ability to withstand sterilization processes and provide consistent performance under stringent conditions makes them an ideal material for healthcare applications. Furthermore, advancements in medical technology, including minimally invasive surgical tools and wearable healthcare devices, are creating new opportunities for the market. As the growth for innovative and high-performance materials in healthcare grows, acetal copolymer market growth are set to play a pivotal role in advancing medical solutions globally.

Acetal Copolymer Market Segmental Analysis :

By Product Type:

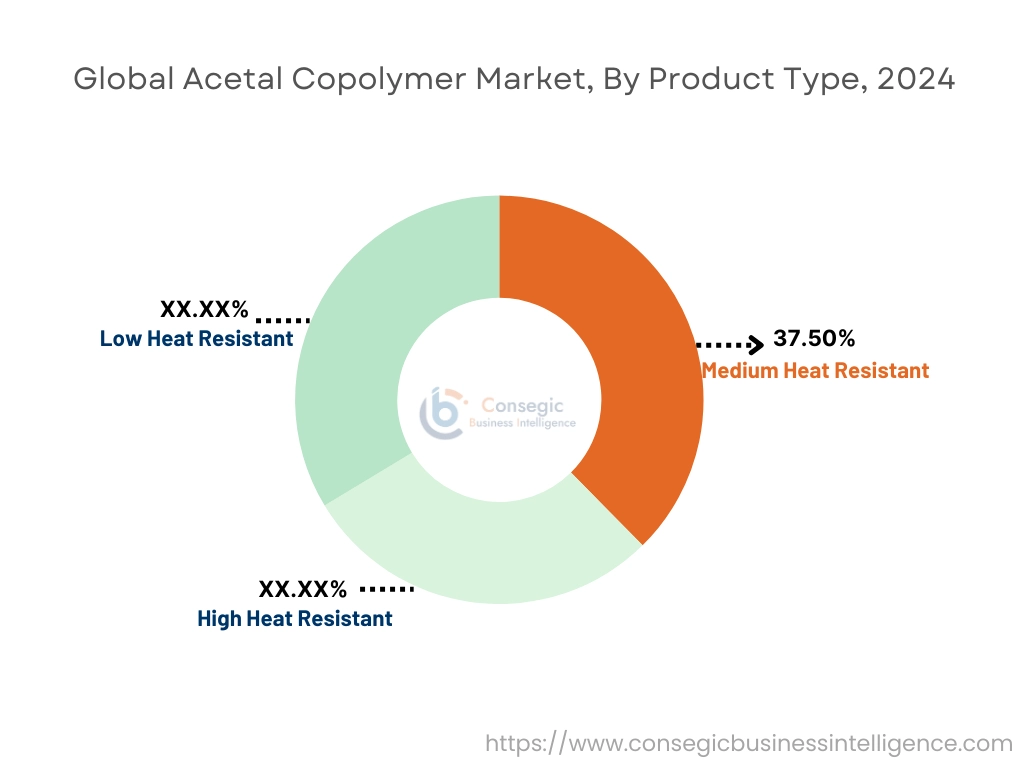

Based on product type, the market is segmented into low heat resistant, medium heat resistant, and high heat resistant.

The medium heat resistant segment accounted for the largest acetal copolymer market share of 37.50% in 2024.

- Medium heat resistant copolymers are extensively used across various industries, including automotive, consumer goods, and electronics.

- These materials offer an optimal balance of mechanical strength and thermal resistance, making them suitable for a wide range of applications, such as gears, bushings, and housings.

- The acetal copolymer market trend of adopting durable and lightweight materials to improve product efficiency has significantly boosted surge for medium heat resistant.

- Additionally, their affordability compared to high heat-resistant variants further supports their market dominance.

- Therefore, the medium heat resistant segment dominates the market analysis due to their versatility, cost-effectiveness, and broad application range.

The high heat resistant segment is anticipated to register the fastest CAGR during the forecast period.

- High heat resistant copolymers are gaining traction in fields requiring advanced performance in harsh operating conditions, such as automotive and industrial machinery.

- The increasing acetal copolymer market trend of miniaturization in electronics and the need for materials that can withstand higher thermal stress have driven the acetal copolymer market demand.

- Moreover, advancements in polymer technology have enhanced their thermal and dimensional stability, further boosting adoption in critical applications.

- As per acetal copolymer market analysis, the high heat resistant type are expected to grow rapidly, driven by their superior performance in high-temperature environments and increasing use in advanced industrial applications.

By End-Use Industry:

Based on end-use industry, the market is segmented into automotive, electronics, industrial machinery, consumer goods, medical devices, and others.

The automotive segment accounted for the largest revenue in acetal copolymer market share in 2024.

- The automotive sectors extensively use them for manufacturing components such as fuel systems, connectors, and safety belts.

- The trend of adopting lightweight materials to enhance fuel efficiency and reduce emissions has propelled rise in acetal copolymer market demand.

- Additionally, their ability to resist wear, friction, and chemicals makes them indispensable in modern automotive applications.

- The growing focus on electric vehicles further supports its adoption for lightweight and durable components.

- Thus, the automotive segmental analysis leads the market, driven by the increasing opportunities for lightweight and durable materials in conventional and electric vehicle manufacturing.

The electronics segment is anticipated to register the fastest CAGR during the forecast period.

- They are widely used in the electronics sectors for applications such as switches, connectors, and insulation components.

- The increasing trend of miniaturization in electronic devices and the demand for materials with excellent dimensional stability and dielectric properties have boosted their adoption.

- Additionally, the rising production of consumer electronics and smart devices is further fueling its applications in this sector.

- Thus, the electronics segmental analysis is expected to grow rapidly, supported by the increasing acetal copolymer market opportunities for miniaturized components and the expansion of the consumer electronics market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

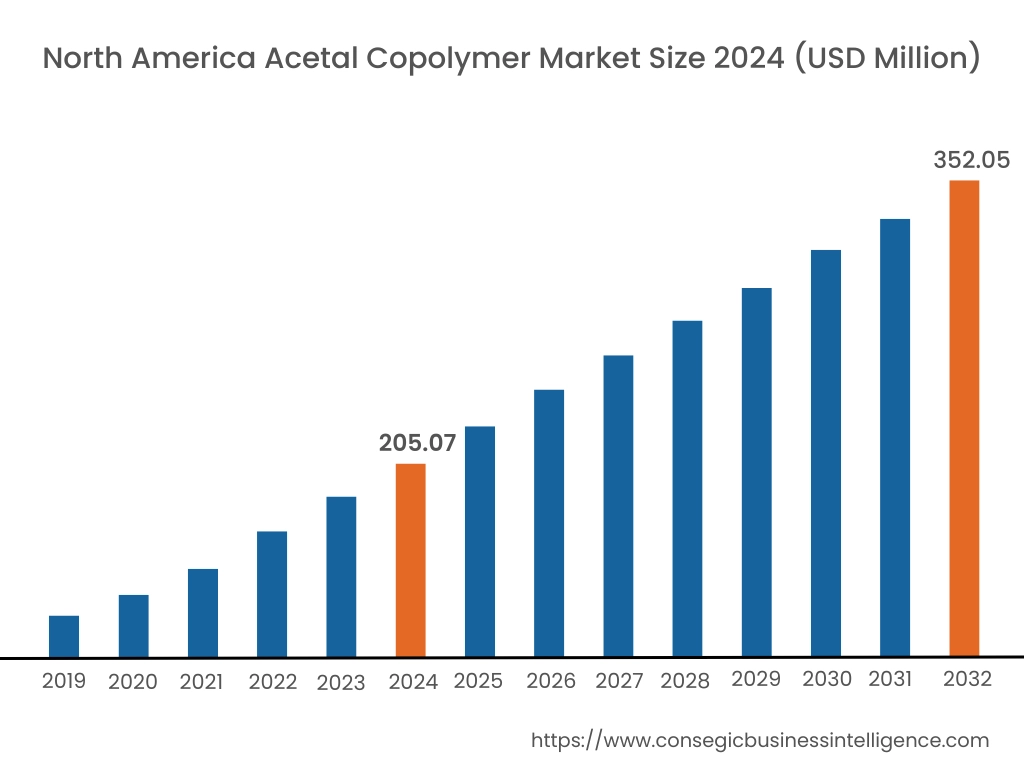

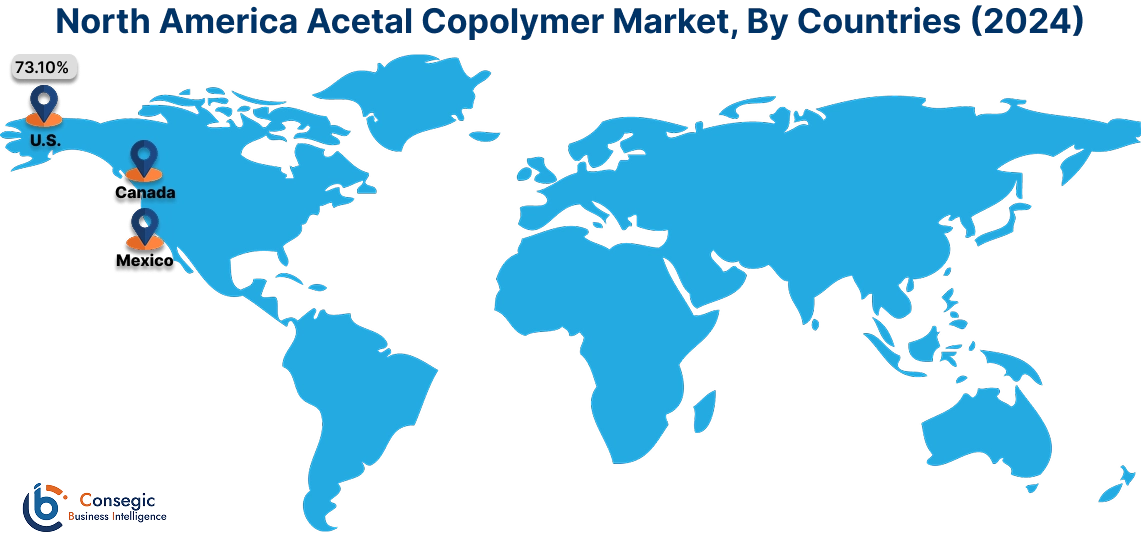

In 2024, North America was valued at USD 205.07 Million and is expected to reach USD 352.05 Million in 2032. In North America, the U.S. accounted for the highest share of 73.10% during the base year of 2024. North America holds a significant stake in the acetal copolymer industry, driven by the demand for high-performance engineering plastics in the automotive, electronics, and industrial sectors. The U.S. leads the region due to its widespread use in manufacturing precision components such as gears, bearings, and fasteners. The increasing adoption of lightweight materials in automotive applications to improve fuel efficiency further enhances the market. Canada contributes to the market with its rise use in industrial machinery and consumer goods. However, environmental regulations on plastic production and recycling present challenges for manufacturers.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.7% over the forecast period. Asia Pacific is the fastest-growing region in the acetal copolymer market analysis, driven by rapid industrialization, urbanization, and expanding automotive and electronics sectors in China, Japan, and India. China dominates the region with its large-scale production capabilities and increasing use in electrical components, consumer goods, and automotive parts. India’s growing automotive industry and emphasis on modernizing industrial processes support the acetal copolymer market growth in machinery components. Japan’s focus on advanced manufacturing techniques and high-precision applications in electronics and medical devices further boosts the market. However, limited recycling infrastructure and environmental concerns over plastic waste management are challenges in some parts of the region.

Europe is a prominent market, supported by the region's advanced automotive and electronics industries. Countries like Germany, France, and the UK are key contributors, with extensive use in automotive components, electrical connectors, and precision parts. Germany’s strong automotive manufacturing sector and focus on lightweight, durable materials drive the market, while France emphasizes eco-friendly applications in consumer goods. The UK is witnessing increasing use in medical devices due to their biocompatibility and chemical resistance. However, stringent EU regulations on plastic materials and high raw material costs pose challenges for manufacturers.

The Middle East & Africa region analysis shows steady advancements in the acetal copolymer market, primarily driven by the growth of the automotive and construction sectors. Countries like Saudi Arabia and the UAE are key markets, utilizing them in industrial applications and construction materials to improve durability and performance. South Africa is witnessing increasing use in consumer goods and electrical components due to growing manufacturing activities. However, limited local production capabilities and reliance on imported raw materials may restrict broader market development in the region.

Latin America is an emerging market, with Brazil and Mexico being primary contributors. Brazil’s automotive and consumer goods sectors rely heavily on engineering plastics, driving its adoption for durable and lightweight components. Mexico’s expanding manufacturing base, particularly in electronics and automotive industries, supports the use of these polymers in precision applications. The region is also seeing growing interest in eco-friendly and recyclable plastic solutions. However, economic volatility and inconsistent regulatory policies across countries can hinder acetal copolymer market expansion.

Top Key Players & Market Share Insights:

The acetal copolymer market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global acetal copolymer market. Key players in the acetal copolymer industry include -

- BASF SE (Germany)

- Celanese Corporation (United States)

- RTP Company, Inc. (United States)

- Polyplastics Co., Ltd. (Japan)

- Mitsubishi Engineering-Plastics Corporation (Japan)

- DuPont de Nemours, Inc. (United States)

- McNeal Enterprises, Inc. (United States)

- Blackwell Plastics LP (United States)

- ALBIS Distribution GmbH & Co. KG (Germany)

- Asahi Kasei Corporation (Japan)

Recent Industry Developments :

Product Launch:

In October 2024, Celanese introduced Hostaform/Celcon ECO-C acetal, marking a significant development in sustainable materials. This new acetal copolymer is made from low-carbon, ISCC CFC-certified methanol produced at Celanese’s Texas plant, making it the company’s lowest carbon footprint acetal product. The ECO-C acetal retains all the essential properties of traditional acetal, such as high stiffness, thermal stability, and wear resistance, while contributing to sustainability goals. This development highlights the growing trend of using low-carbon and recycled feedstocks to produce high-performance engineering plastics, particularly in sectors focused on sustainability and electric vehicles.

Acetal Copolymer Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,086.23 Million |

| CAGR (2025-2032) | 7.3% |

| By Product Type |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Acetal Copolymer Market by 2032? +

The market is expected to reach over USD 1,086.23 Million by 2032.

Which product type dominates the market? +

The medium heat-resistant segment holds the largest market share due to its balance of thermal resistance, mechanical strength, and cost-effectiveness.

What is the fastest-growing product type in the market? +

The high heat-resistant segment is anticipated to grow at the fastest CAGR, driven by its applications in harsh operating conditions, including automotive and industrial machinery.

Which end-use industry accounts for the largest market share? +

The automotive sector leads the market, utilizing acetal copolymers for lightweight, durable components like gears, bushings, and fuel systems to enhance fuel efficiency and reduce emissions.

Which end-use industry is expected to grow the fastest? +

The electronics industry is projected to grow rapidly, supported by the miniaturization of devices and the increasing demand for precise, high-performance components in consumer electronics and smart devices.