- Summary

- Table Of Content

- Methodology

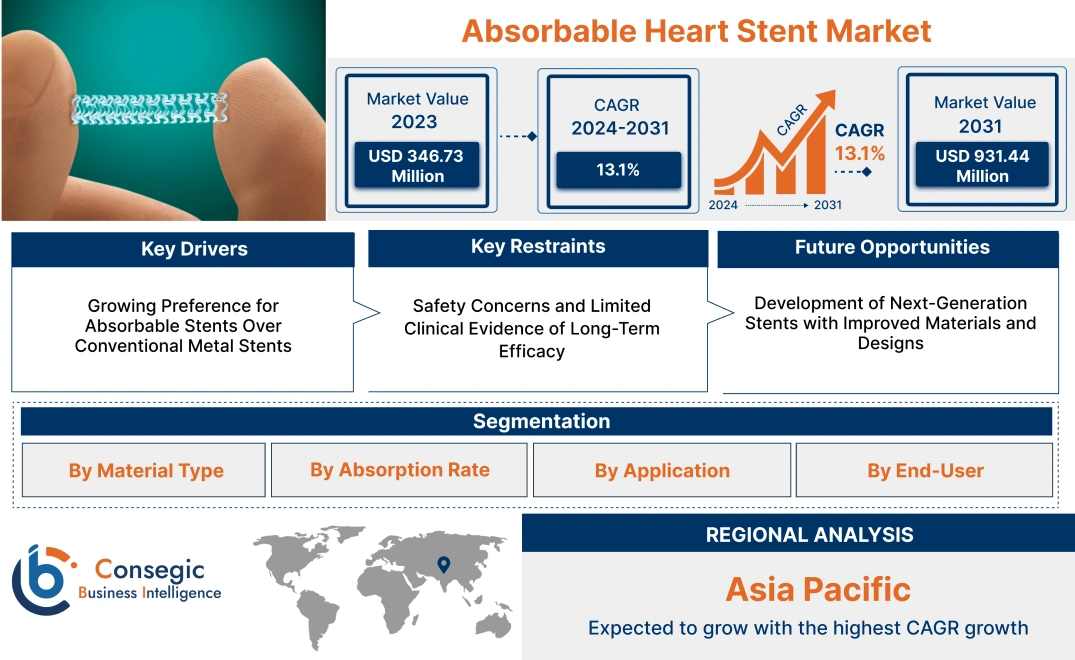

Absorbable Heart Stent Market Size:

Absorbable Heart Stent Market size is estimated to reach over USD 1,025.07 Million by 2032 from a value of USD 383.96 Million in 2024 and is projected to grow by USD 427.27 Million in 2025, growing at a CAGR of 13.1% from 2025 to 2032.

Absorbable Heart Stent Market Scope & Overview:

Absorbable heart stents, also known as bioresorbable stents, are medical devices used to open blocked coronary arteries and restore blood flow to the heart. Unlike traditional metal stents, absorbable stents are designed to gradually dissolve after serving their purpose, reducing long-term risks such as vessel scarring or restenosis. Made from materials like polylactic acid, these stents provide temporary support to the artery, promoting natural healing and minimizing the need for permanent implants. Hospitals, specialty cardiac centers, and clinics are key end-users of absorbable heart stents. As healthcare providers increasingly adopt advanced stenting technologies to enhance patient outcomes, the market is expected to witness substantial growth, driven by the increasing prevalence of cardiovascular diseases and the shift toward bioresorbable solutions.

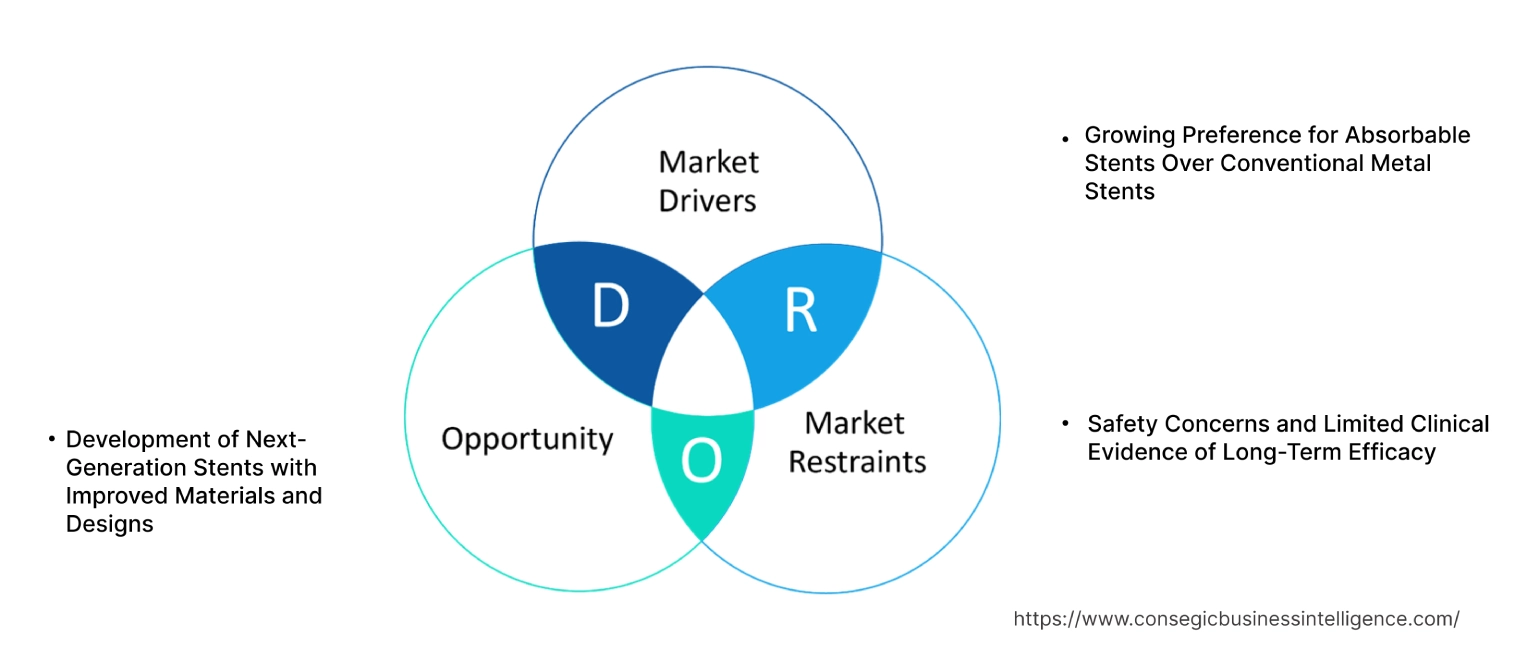

Absorbable Heart Stent Market Dynamics - (DRO) :

Key Drivers:

Growing Preference for Absorbable Stents Over Conventional Metal Stents

The absorbable heart stent market growth is primarily driven by the increasing preference for bioabsorbable stents over traditional metal stents in the treatment of coronary artery disease (CAD). Unlike metal stents, which remain in the body permanently, absorbable stents gradually dissolve after serving their purpose of keeping the artery open during the critical healing period. This reduces long-term complications such as in-stent restenosis (narrowing of the artery due to scar tissue) and the need for prolonged dual antiplatelet therapy (DAPT). The ability of absorbable stents to reduce the long-term risks of inflammation and thrombosis, combined with their capacity to restore natural vasomotion after dissolution, has made them an attractive option for both physicians and patients. As a result, absorbable stents are gaining traction, especially among younger patients and those who require future coronary interventions. This shift in clinical preference is fueling the market demand for more advanced bioabsorbable stent technologies.

Key Restraints :

Safety Concerns and Limited Clinical Evidence of Long-Term Efficacy

Despite the potential advantages, the market faces significant challenges due to safety concerns and limited long-term clinical data. Early generations of bioabsorbable stents, particularly those made of polylactic acid (PLA), have been associated with higher rates of device failure, including late stent thrombosis and increased risk of restenosis compared to traditional metal stents. These issues have raised concerns about the overall efficacy and safety profile of absorbable stents, particularly in complex coronary cases or high-risk patients. Additionally, the lack of extensive long-term clinical trials validating the performance of newer bioabsorbable stents has limited their widespread adoption. Regulatory authorities have imposed stricter approval criteria, demanding comprehensive clinical evidence to ensure the safety and effectiveness of these devices, which has delayed absorbable heart stent market expansion and increased the cost of bringing new products to market.

Future Opportunities :

Development of Next-Generation Stents with Improved Materials and Designs

The development of next-generation absorbable stents using advanced materials and innovative designs presents a significant absorbable heart stent market opportunity. Recent advancements in materials science, such as the use of magnesium alloys and new polymer coatings, have shown promise in addressing the limitations of earlier stent designs. These new materials offer faster degradation rates, improved mechanical strength, and enhanced biocompatibility, reducing the risk of thrombosis and restenosis. Additionally, innovations in stent architecture, such as thinner struts and more flexible designs, are improving deliverability and reducing procedural complications. These next-generation stents are expected to provide better long-term outcomes, positioning them as viable alternatives to both traditional metal stents and earlier bioabsorbable stents. As research progresses and more clinical evidence becomes available, the adoption of these advanced stents is anticipated to increase, particularly in markets that are focused on minimizing long-term complications and improving patient outcomes.

Absorbable Heart Stent Market Segmental Analysis :

By Material Type:

Based on material type, the market is segmented into polymer-based stents and metal-based stents.

The polymer-based stents segment accounted for the largest revenue share of the total absorbable heart stent market share in 2024.

- Polymer-based absorbable stents are widely preferred in interventional cardiology due to their biocompatibility and ability to degrade naturally within the body after serving their purpose of maintaining vessel patency.

- These stents are designed to dissolve over time, eliminating the need for a permanent implant and reducing long-term complications such as in-stent restenosis and thrombosis.

- Advancements in polymer technology, including the development of bioresorbable materials with enhanced mechanical properties, have improved the performance of polymer-based stents, making them the leading choice for both coronary and peripheral artery disease treatments.

- Thus, as per the market trends analysis, polymer-based stents dominate the market due to their biocompatibility, ability to degrade naturally, and advancements in bioresorbable material technology that enhance patient outcomes, boosting the absorbable heart stent market demand.

The metal-based stents segment is anticipated to register the fastest CAGR during the forecast period.

- Metal-based absorbable stents, particularly those made from magnesium alloys, are gaining traction in the market due to their high strength and rapid degradation properties.

- These stents offer immediate radial support to the arterial wall, similar to traditional metal stents while being gradually absorbed by the body.

- The growing focus on developing metal-based stents that combine the benefits of traditional stents with the safety profile of bioresorbable materials is driving their adoption, especially in high-risk patients where stronger initial support is required.

- As per the segmental trends, metal-based stents are expected to grow rapidly due to their strong initial support and the increasing development of bioresorbable metal materials that enhance patient safety, boosting the absorbable heart stent market trends.

By Absorption Rate:

Based on absorption rate, the market is segmented into fast absorption stents and slow absorption stents.

The fast absorption stents segment accounted for the largest revenue share of the overall absorbable heart stent market share in 2024.

- Fast absorption stents are designed to dissolve quickly, typically within a year, providing temporary support to the artery during the healing process and minimizing long-term risks.

- These stents are particularly suited for younger patients or those at lower risk of complications, where a shorter support period is adequate.

- The reduced risk of chronic inflammation and restenosis, along with a lower incidence of late thrombosis, has driven the demand for fast absorption stents in coronary artery disease treatments.

- Thus, the segmental trends depict that fast absorption stents lead the market due to their ability to provide temporary arterial support while minimizing long-term risks, making them an ideal choice for low-risk patients, and boosting the absorbable heart stent market demand.

The slow absorption stents segment is anticipated to register the fastest CAGR during the forecast period.

- Slow absorption stents offer extended support to arteries, typically dissolving over two to three years.

- These stents are often preferred in complex or high-risk cases where prolonged mechanical support is necessary to ensure arterial patency.

- Advances in material science have allowed for better control over degradation rates, ensuring that these stents provide support over an extended period while gradually being absorbed by the body.

- The increasing incidence of complex cardiovascular conditions, where long-term arterial support is crucial, is driving the growth of this segment.

- Therefore, the analysis of the segmental trends shows that slow absorption stents are expected to grow rapidly due to their extended support, making them essential for high-risk patients requiring prolonged arterial patency, creating absorbable heart stent market opportunities.

By Application:

Based on application, the market is segmented into coronary artery disease and peripheral artery disease.

The coronary artery disease segment accounted for the largest revenue share of 70.54% in 2024.

- Coronary artery disease (CAD) is one of the leading causes of death globally, and absorbable stents have emerged as a promising solution for treating blockages in coronary arteries.

- These stents provide the necessary support to restore blood flow while reducing the long-term risks associated with permanent stents, such as in-stent restenosis and late thrombosis.

- The growing adoption of absorbable stents in CAD is driven by their ability to reduce long-term complications and provide better patient outcomes.

- Additionally, the rising incidence of CAD due to lifestyle factors and aging populations is contributing to the demand for these innovative stents.

- The coronary artery disease segment dominates the market, driven by the rising incidence of CAD and the benefits of absorbable stents in reducing long-term complications and improving patient outcomes, driving the absorbable heart stent market growth.

The peripheral artery disease segment is anticipated to register the fastest CAGR during the forecast period.

- Peripheral artery disease (PAD) affects the arteries outside the heart, particularly in the legs, and absorbable stents are increasingly being used to treat blockages in these arteries.

- Absorbable stents offer an advantage in PAD treatment by providing temporary support to the arteries, which can be beneficial in reducing the risk of complications in these often complex cases.

- The ability of absorbable stents to minimize long-term vessel damage and the growing adoption of these stents in peripheral interventions are driving the rapid growth of this segment.

- The peripheral artery disease segment is expected to grow rapidly due to the increasing adoption of absorbable stents in peripheral interventions, where temporary support can significantly reduce long-term complications, boosting the absorbable heart stent market trends.

By End-User:

Based on end-users, the market is segmented into hospitals, ambulatory surgical centers (ASCs), cardiac centers, and others.

The hospitals segment accounted for the largest revenue share of the global absorbable heart stent market share in 2024.

- Hospitals are the primary setting for cardiovascular interventions, including the placement of absorbable stents.

- The availability of advanced diagnostic and therapeutic facilities, coupled with the presence of specialized healthcare professionals, makes hospitals the largest consumers of absorbable stents.

- As the demand for minimally invasive procedures continues to rise, hospitals are increasingly adopting advanced technologies like absorbable stents to improve patient outcomes and reduce recovery times.

- The growing number of hospital-based cardiovascular procedures globally supports the dominant position of this segment.

- As per the absorbable heart stent market analysis, hospitals dominate the market as the primary consumers of absorbable stents, driven by the increasing demand for minimally invasive cardiovascular procedures and the availability of specialized healthcare facilities.

The ambulatory surgical centers (ASCs) segment is anticipated to register the fastest CAGR during the forecast period.

- ASCs are increasingly becoming a preferred setting for cardiovascular interventions, including stent placements, due to their cost-effectiveness and shorter patient stays.

- These centers are particularly attractive for lower-risk patients who can benefit from same-day procedures with quicker recovery times.

- The adoption of absorbable stents in ASCs is growing as these centers expand their capabilities to perform advanced cardiovascular interventions.

- The rise in outpatient cardiovascular procedures and the demand for cost-effective treatments are driving the growth of this segment.

- Ambulatory surgical centers are expected to grow rapidly as the demand for cost-effective and minimally invasive cardiovascular procedures increases, positioning them as key adopters of absorbable stents.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

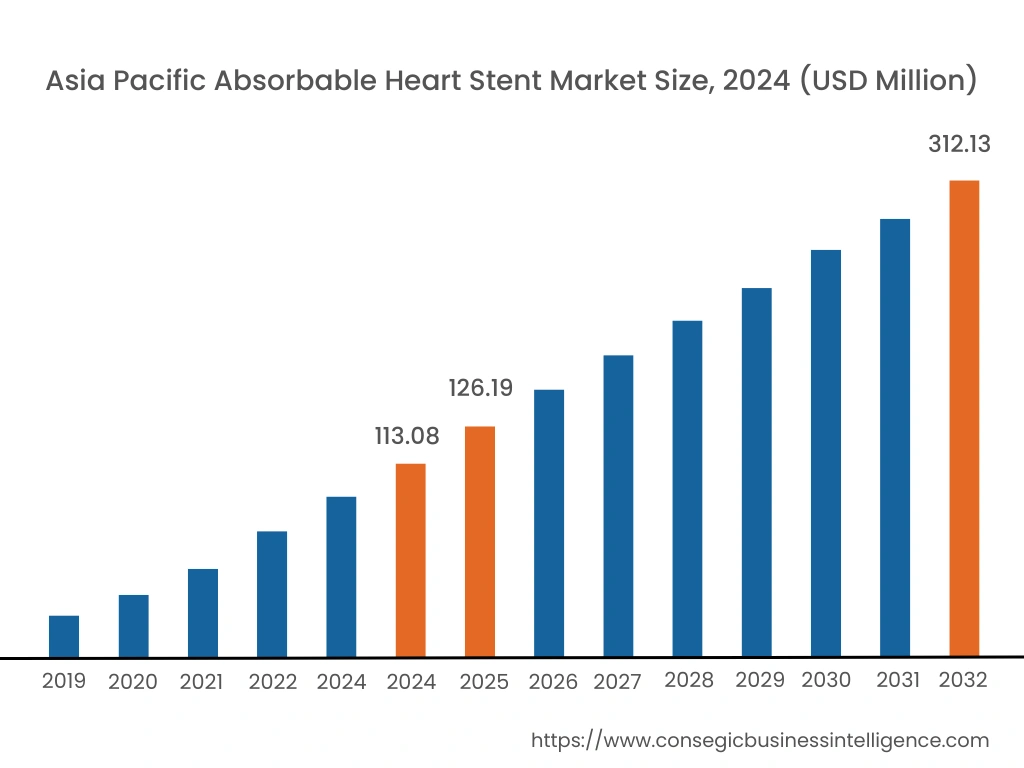

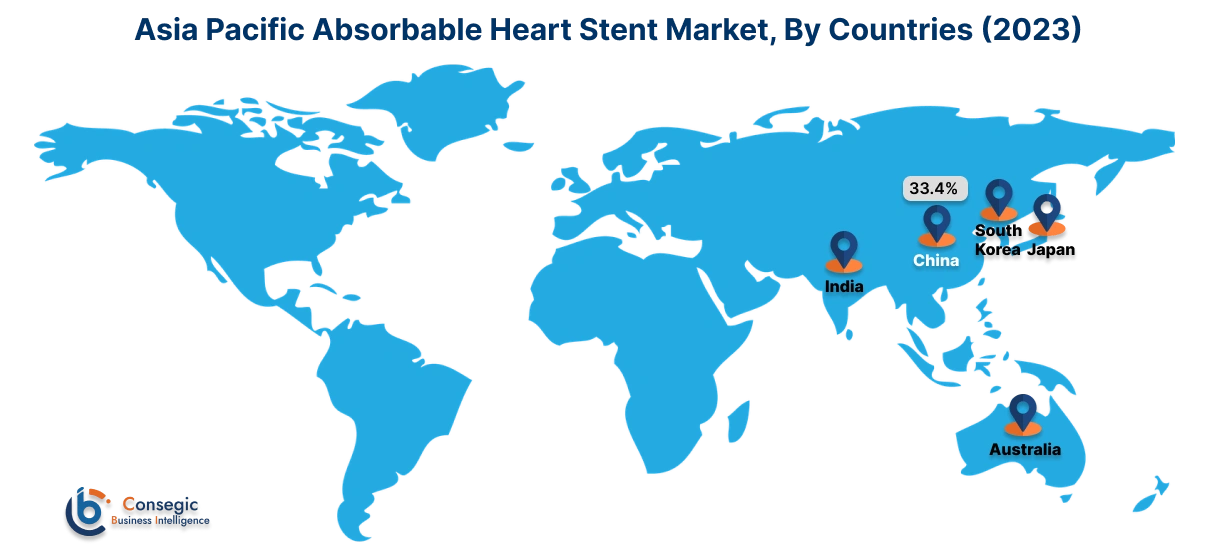

Asia Pacific region was valued at USD 113.08 Million in 2024. Moreover, it is projected to grow by USD 126.19 Million in 2025 and reach over USD 312.13 Million by 2032. Out of this, China accounted for 33.4% of the total market share. Asia-Pacific is witnessing the fastest growth in the market, driven by an increasing burden of cardiovascular diseases in countries like China, Japan, and India. Improving healthcare infrastructure, rising healthcare spending, and growing adoption of advanced cardiovascular treatments are fueling market expansion. Government initiatives to improve cardiac care facilities and a large, aging population further support market growth. However, challenges such as affordability issues and limited awareness in rural areas may impede the uptake of absorbable stents, particularly in less urbanized regions.

The absorbable heart stent market analysis depicts that North America commands a leading share in the market, particularly due to the advanced cardiovascular care infrastructure and increasing prevalence of coronary artery disease (CAD). The U.S. is a key contributor, driven by high healthcare expenditure, robust adoption of innovative cardiovascular technologies, and the presence of major medical device manufacturers like Abbott Laboratories. Rising awareness about minimally invasive procedures also boosts the market. However, strict FDA approval processes and concerns over the long-term efficacy of absorbable stents could slow down broader adoption.

Europe represents a significant portion of the global market, with Germany, France, and the UK being the major contributors. The region benefits from strong government support for cardiovascular disease management and advanced healthcare facilities. Furthermore, ongoing clinical trials and research efforts on bioabsorbable stents, particularly in Germany, are enhancing the adoption of this technology. However, the high costs of absorbable stents and stringent CE marking requirements for medical devices could challenge rapid market growth.

The Middle East & Africa region shows promising potential in the market, particularly in countries like Saudi Arabia, the UAE, and South Africa. Increasing healthcare investments and rising incidences of coronary artery diseases drive the demand for advanced stent technologies in this region. The expanding medical tourism sector, particularly in the UAE, where high-quality cardiovascular treatments are offered, further supports market growth. Nonetheless, limited local manufacturing capabilities and the high cost of absorbable stents remain barriers to broader market penetration in this region.

The regional analysis shows that Latin America is an emerging market for absorbable heart stents, with Brazil and Mexico being the primary growth drivers. The rising prevalence of coronary heart disease and increasing focus on improving healthcare infrastructure contribute to the market's expansion. Government initiatives aimed at enhancing access to advanced cardiovascular treatments, combined with the region's increasing awareness of bioabsorbable stents, support market growth. However, economic constraints and unequal access to advanced healthcare technologies in some areas present challenges to market development in this region.

Top Key Players & Market Share Insights:

The absorbable heart stent market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global absorbable heart stent market. Key players in the absorbable heart stent industry include -

- Abbott Laboratories (USA)

- Boston Scientific Corporation (USA)

- Medtronic plc (Ireland)

- BIOTRONIK SE & Co. KG (Germany)

- Terumo Corporation (Japan)

- Elixir Medical Corporation (USA)

- REVA Medical, Inc. (USA)

- Arterial Remodeling Technologies (France)

- Kyoto Medical Planning Co., Ltd. (Japan)

- Amaranth Medical, Inc. (USA)

Recent Industry Developments :

Approvals:

- In April 2024, Abbott's Esprit™ BTK Everolimus Eluting Resorbable Scaffold System was FDA-approved for treating chronic limb-threatening ischemia (CLTI) below the knee. This dissolvable stent offers better outcomes than balloon angioplasty, helping to heal arteries and reduce disease progression.

Absorbable Heart Stent Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,025.07 Million |

| CAGR (2025-2032) | 13.1% |

| By Material Type |

|

| By Absorption Rate |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Absorbable Heart Stent Market? +

In 2024, the Absorbable Heart Stent market was USD 383.96 million.

What will be the potential market valuation for the Absorbable Heart Stent by 2032? +

In 2032, the market size of Absorbable Heart Stent is expected to reach USD 1,025.07 million.

What are the segments covered in the Absorbable Heart Stent market report? +

The material types, absorption rates, applications, and end-user industries are the segments covered in this report.

Who are the major players in the Absorbable Heart Stent market? +

Abbott Laboratories (USA), Boston Scientific Corporation (USA), Medtronic plc (Ireland), BIOTRONIK SE & Co. KG (Germany), Terumo Corporation (Japan), Elixir Medical Corporation (USA), REVA Medical, Inc. (USA), Arterial Remodeling Technologies (France), Kyoto Medical Planning Co., Ltd. (Japan), Amaranth Medical, Inc. (USA) are the major players in the Absorbable Heart Stent market.