- Summary

- Table Of Content

- Methodology

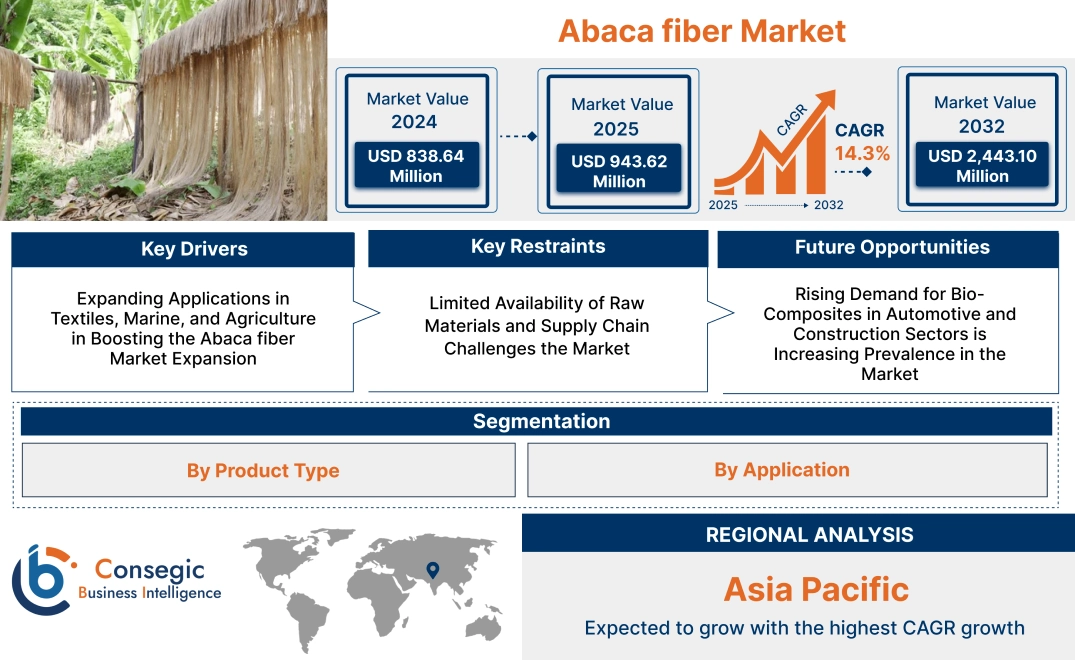

Abaca fiber Market Size:

Abaca fiber Market size is estimated to reach over USD 2,443.10 Million by 2032 from a value of USD 838.64 Million in 2024 and is projected to grow by USD 943.62 Million in 2025, growing at a CAGR of 14.3% from 2025 to 2032.

Abaca fiber Market Scope & Overview:

The abaca fiber focuses on the production and application of abaca, a natural fiber extracted from the leaf stalks of the abaca plant, known for its high tensile strength, durability, and sustainability. Abaca fibers are widely used in industries such as paper and pulp, textiles, and composites due to their eco-friendly nature and exceptional performance characteristics. Key features of abaca fiber include its biodegradability, resistance to saltwater, and lightweight construction, making it a preferred choice for diverse industrial and consumer applications. The benefits include enhanced product performance, reduced environmental impact, and versatility across various sectors. Applications span specialty paper production (including currency notes and tea bags), ropes, automotive composites, and geotextiles. End-users include paper manufacturers, automotive industries, and marine and agriculture sectors, driven by increasing trends for sustainable materials, advancements in fiber processing technologies, and supportive regulatory frameworks promoting biodegradable alternatives.

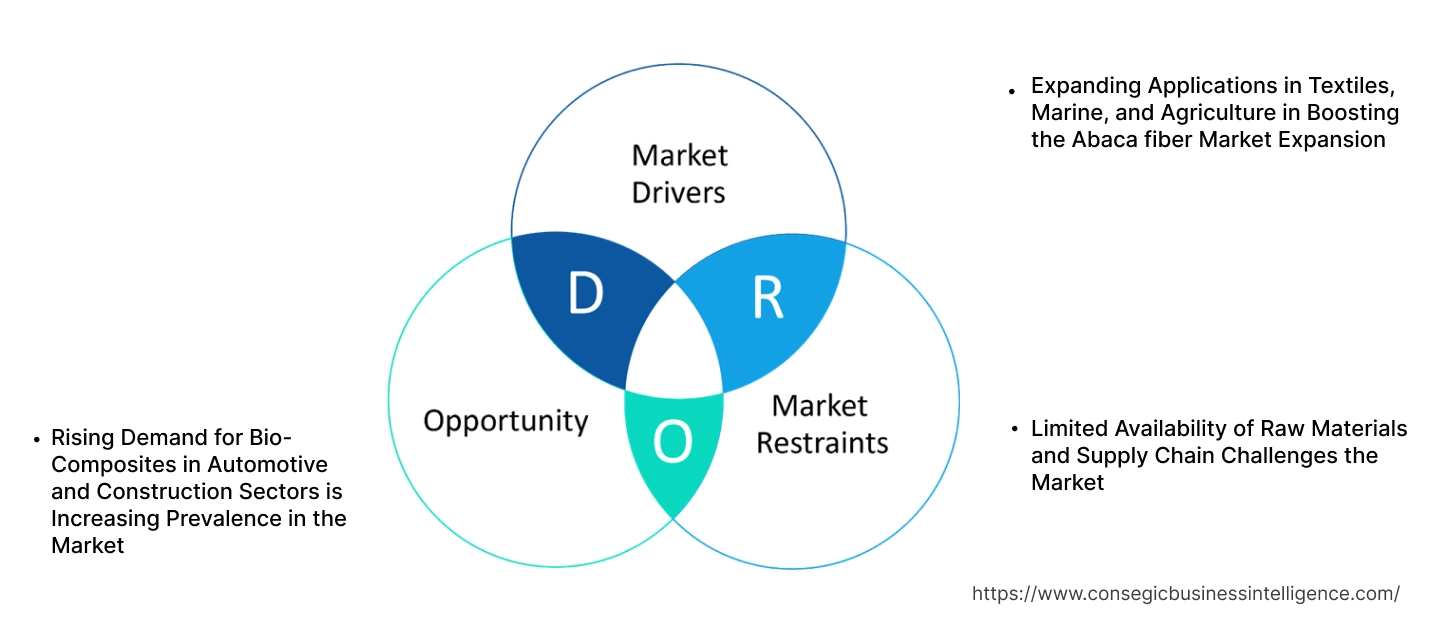

Abaca fiber Market Dynamics - (DRO) :

Key Drivers:

Expanding Applications in Textiles, Marine, and Agriculture in Boosting the Abaca fiber Market Expansion

Abaca fiber's high tensile strength, flexibility, and resistance to wear and tear make it an invaluable material across multiple industries, including textiles, marine, and agriculture. In the textile sector, abaca is used to create industrial ropes, nets, and specialty fabrics that are durable and capable of withstanding heavy-duty applications. These fibers are also gaining traction in creating eco-friendly alternatives for decorative and functional textiles in interior design and fashion, aligning with global trends favoring sustainable materials.

In the marine industry, abaca fiber is a preferred choice for producing ropes and cordage due to its resistance to water and salt, ensuring long-lasting performance in challenging maritime environments. Additionally, in agriculture, abaca fibers are employed for creating sacks, mats, and soil erosion control products. These applications emphasize the fiber's utility in enhancing sustainability and operational efficiency across diverse sectors, reinforcing its importance in industrial and environmental solutions.

Key Restraints:

Limited Availability of Raw Materials and Supply Chain Challenges the Market

The production of abaca fiber is heavily reliant on specific geographic regions, with the Philippines being the dominant supplier. This dependence creates vulnerabilities in the supply chain, including susceptibility to climate changes, natural disasters, and geopolitical disruptions. Such factors can result in inconsistent supply and increased raw material costs, affecting the availability of global abaca fiber markets.

Additionally, limited farming infrastructure and traditional cultivation methods in producing regions restrict the scalability of abaca production. Transporting raw materials to processing facilities and international markets expansion further adds to logistical costs and delays, particularly in times of worldwide supply chain disruptions. Addressing these challenges through investment in modern agricultural practices and diversified sourcing is essential for ensuring the steady supply of abaca fiber to meet evolving industry needs.

Future Opportunities :

Rising Demand for Bio-Composites in Automotive and Construction Sectors is Increasing Prevalence in the Market

The automotive and construction industries are increasingly integrating bio-composites to enhance sustainability and reduce environmental footprints. Abaca fiber, known for its lightweight and durable properties, is a preferred reinforcement material in bio-composites used for vehicle interiors, panels, and structural applications. Its ability to reduce the weight of components while maintaining strength and reliability aligns with sectors trends focusing on energy efficiency and sustainable manufacturing.

In the construction sector, abaca fiber is being used in composites for roofing, insulation, and reinforcement of concrete materials. These bio-composites not only improve the performance of construction materials but also support green building initiatives, which are gaining traction globally. Analysis indicates that as industries prioritize eco-friendly solutions, the adoption of abaca-based composites in automotive and construction applications is poised to increase, presenting significant opportunities for manufacturers to expand their market presence.

Abaca fiber Market Segmental Analysis :

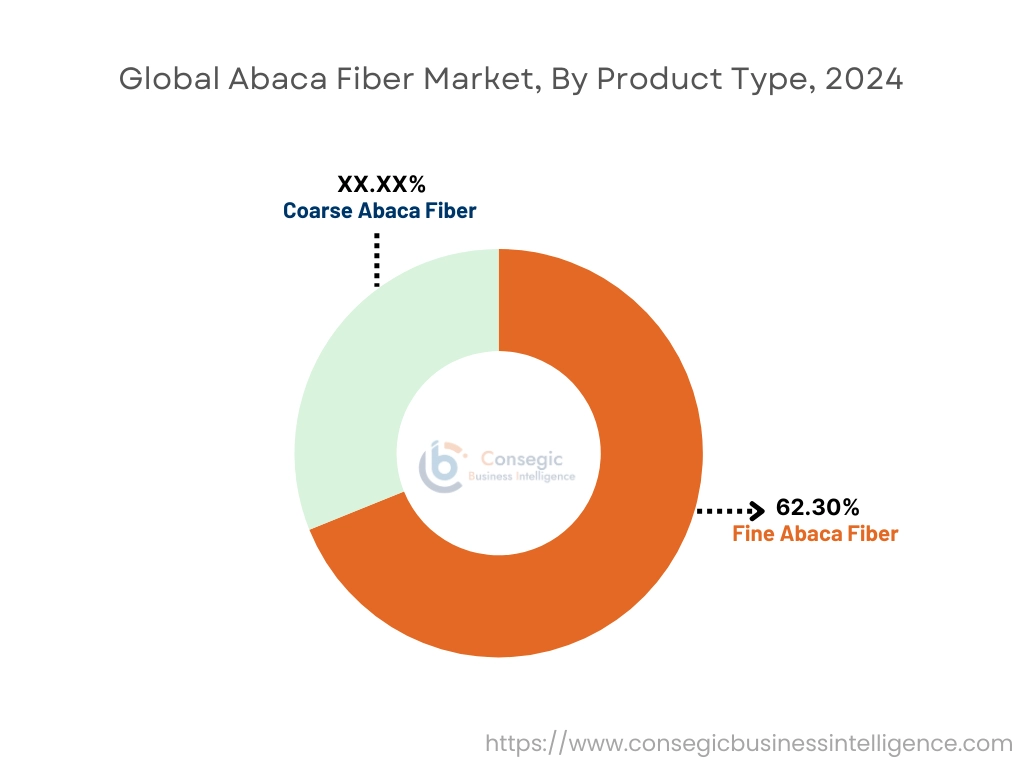

By Product Type:

Based on product type, the market is segmented into fine and coarse fibers.

The fine abaca fiber segment accounted for the largest revenue in abaca fiber market share of 62.30% in 2024.

- Fine abaca fibers are widely used in high-value applications, particularly in the pulp and paper industry for producing specialty papers such as currency notes, tea bags, and filter papers.

- These fibers are preferred due to their superior tensile strength, lightweight nature, and ability to create durable and thin sheets.

- The increasing adoption of eco-friendly materials in high-end applications has further boosted the abaca fiber market trends for fine abaca fibers.

- Additionally, fine fibers are increasingly used in the composites sectors for lightweight automotive and aerospace components, further driving their dominance.

- As per the abaca fiber market analysis, fine abaca fibers dominate the market due to their superior strength and extensive use in specialty paper and high-performance composite applications.

The coarse abaca fiber segment is anticipated to register steady growth during the forecast period.

- Coarse abaca fibers are primarily utilized in cordage, including ropes, twines, and fishing lines, due to their durability and high resistance to saltwater and abrasion.

- These fibers are also widely used in agricultural applications for making sacks and mats.

- The share of the marine and agriculture sectors, coupled with the increasing abaca fiber market trends for sustainable and biodegradable materials, is expected to support steady growth in this segment.

- Coarse abaca fibers continue to grow steadily as per the market analysis, driven by their widespread use in durable cordage and agricultural applications, particularly in marine and farming industries.

By Application:

Based on application, the market is segmented into pulp & paper, fine craft, cordage, ropes & yarns, composites, and others.

The pulp & paper segment accounted for the largest revenue in abaca fiber market share in 2024.

- The pulp and paper sectors is the largest consumer of abaca fibers, particularly for the production of high-quality specialty papers, including currency notes, tea bags, and filter papers.

- The exceptional tensile strength and durability of abaca fibers make them ideal for these applications, where quality and longevity are critical.

- The increasing global focus on sustainable and biodegradable paper products, especially in light of stricter environmental regulations, has further fueled for abaca fiber market demand in this segment.

- As per the market analysis, Pulp & paper leads the market, driven by the high trends for durable specialty papers and the worldwide shift towards sustainable and eco-friendly products.

The composites segment is anticipated to register the fastest CAGR during the forecast period.

- The composites sectors is rapidly adopting abaca fibers as a sustainable alternative to synthetic fibers for producing lightweight, durable components.

- Abaca fibers are increasingly used in the automotive and aerospace sectors for making interior panels, reinforcements, and other structural components.

- The growing emphasis on reducing carbon emissions and adopting renewable materials in manufacturing is driving the trends for abaca fibers in composites.

- Innovations in fiber processing and the development of bio-composites are further propelling abaca fiber market growth in this segment.

- Composites are expected to grow rapidly, driven by increasing abaca fiber market opportunities for lightweight, sustainable materials in the automotive and aerospace industries.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

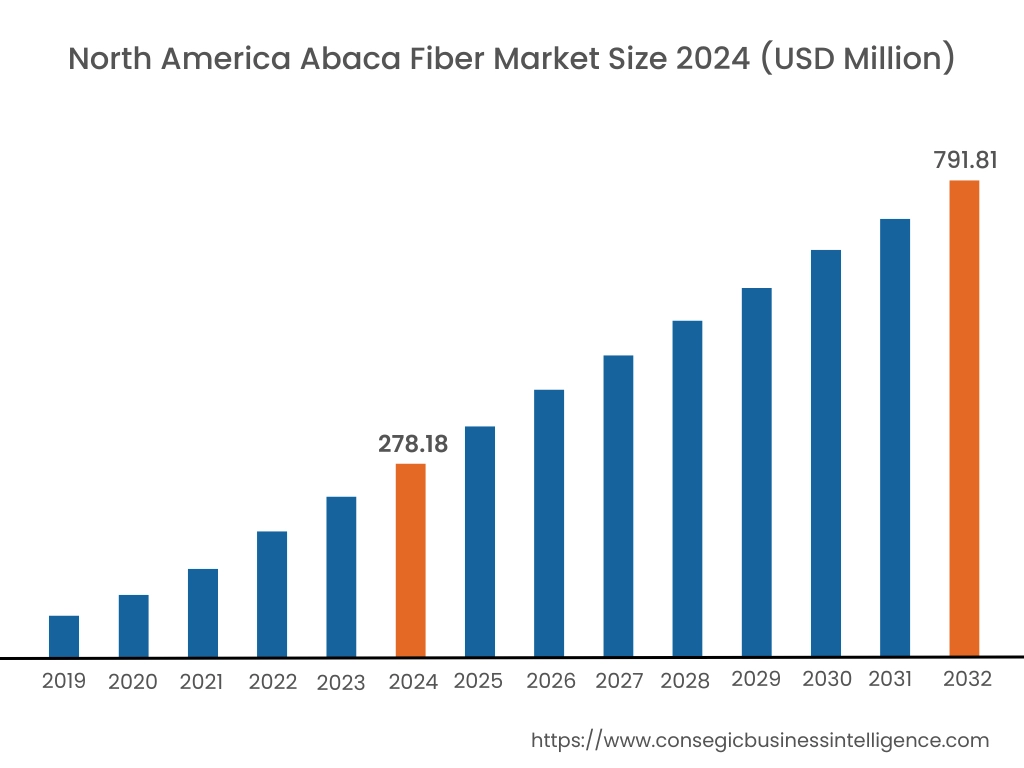

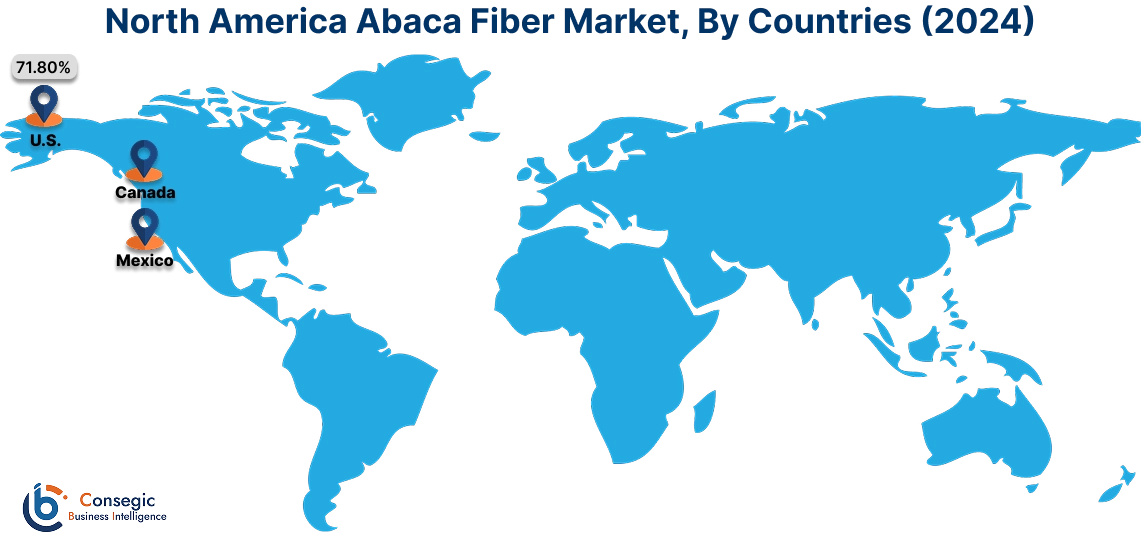

In 2024, North America was valued at USD 278.18 Million and is expected to reach USD 791.81 Million in 2032. In North America, the U.S. accounted for the highest share of 71.80% during the base year of 2024. As per the abaca fiber market analysis, North America holds a significant share, due to increasing demand for sustainable and biodegradable materials across industries. The U.S. leads the region with strong applications in specialty paper products such as tea bags, currency paper, and filter paper. Growing interest in eco-friendly packaging solutions also supports the use of abaca fiber in composite materials for automotive and industrial applications. Canada contributes to the market with rising adoption of natural fibers in niche applications like sustainable textiles. However, limited local production of abaca fiber and reliance on imports may pose challenges for the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 14.8% over the forecast period. Asia-Pacific is the largest producer and consumer of abaca fiber as per the analysis, with the Philippines dominating the global market as the primary producer of high-quality abaca. The region benefits from strong abaca fiber market demand in applications like ropes, marine cordage, and pulp for specialty papers. The Philippines and Indonesia are the main suppliers, catering to both domestic and international markets. China is a significant importer, using abaca fiber in industrial and packaging applications, while Japan incorporates it into specialty papers and automotive composites. India is witnessing abaca fiber market growth in its trends for abaca fiber in textiles and agricultural applications. However, fluctuating production due to climatic conditions and farming challenges may affect the supply chain.

Europe is a prominent market for abaca fiber, driven by its focus on sustainability and strict regulations on single-use plastics. Countries like Germany, the UK, and France are leading contributors. Germany’s automotive sectors increasingly uses abaca fiber in composite materials to enhance lightweighting and sustainability. The UK and France emphasize its application in specialty paper products and biodegradable packaging. The European Union’s focus on reducing environmental impact has led to rising adoption of abaca fiber in various eco-friendly applications. However, the high cost of processing and transportation for imported abaca fiber can impact the market in the region.

The Middle East & Africa region is experiencing gradual progress in the abaca fiber market expansion, driven by increasing interest in sustainable materials for packaging and construction applications. The UAE and Saudi Arabia are exploring the use of natural fibers like abaca in eco-friendly packaging and construction composites. In Africa, South Africa is emerging as a market for abaca fiber in agricultural products and industrial textiles. However, limited awareness and lack of local production facilities restrict the broader adoption of abaca fiber in this region.

Latin America is an emerging market for abaca fiber, with growing interest in sustainable materials for packaging and industrial applications. As the regional analysis Brazil is a key market in the region, leveraging abaca fiber for agricultural applications and export opportunities. Mexico is exploring its use in automotive composites and eco-friendly packaging. The region also benefits from its favorable climatic conditions, which are suitable for natural fiber production, though abaca farming is not yet widely adopted. Economic instability and lack of established supply chains may pose challenges to the market's growth in Latin America.

Top Key Players & Market Share Insights:

The abaca fiber market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global abaca fiber market. Key players in the abaca fiber industry include -

- Ching Bee Trading Corporation (Philippines)

- MAP Enterprises (Philippines)

- Peral Enterprises (Philippines)

- Simor Abaca Products (Philippines)

- SAMATOA (Cambodia)

- Tag Fibers, Inc. (Philippines)

- Selinrail International Trading (Philippines)

- The Fiber World (Philippines)

- Italfil Expo Bags Company Limited (Philippines)

- Yzen Handicraft Export Trading (Philippines)

Recent Industry Developments :

Innovation:

- In July 2021, PALTEX introduced its new Abaca fibers collection, a sustainable textile innovation made from Musa, a banana species native to the Philippines. Abaca fibers are 100% biodegradable, highly breathable, durable, and pesticide-free, offering a sustainable alternative to cotton. The development focuses on using Abaca fibers for textiles, including woven and knitted fabrics, which are ideal for outdoor shirts and sportswear. This environmentally friendly option has garnered attention due to its performance benefits and its eco-friendly, sustainable production processes. The use of Abaca fibers demonstrates PALTEX's commitment to sustainability in the textile industry, helping meet the growing demand for eco-conscious materials in the fashion and apparel sectors.

Abaca fiber Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2,443.10 Million |

| CAGR (2025-2032) | 14.3% |

| By Product Type |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Abaca Fiber Market by 2032? +

Abaca fiber Market size is estimated to reach over USD 2,443.10 Million by 2032 from a value of USD 838.64 Million in 2024 and is projected to grow by USD 943.62 Million in 2025, growing at a CAGR of 14.3% from 2025 to 2032.

What are the primary drivers for the Abaca Fiber Market? +

The market growth is driven by the rising demand for sustainable and biodegradable materials, expanding applications in textiles, marine, and agriculture, and the growing adoption of abaca-based composites in the automotive and construction sectors.

Which product type dominates the Abaca Fiber Market? +

Fine abaca fibers dominate the market due to their extensive use in high-value applications such as specialty papers (currency notes, tea bags) and lightweight composites for automotive and aerospace industries.

Which application segment is growing the fastest? +

The composites segment is anticipated to register the fastest growth, driven by increasing demand for lightweight, durable, and sustainable materials in automotive and construction industries.