- Summary

- Table Of Content

- Methodology

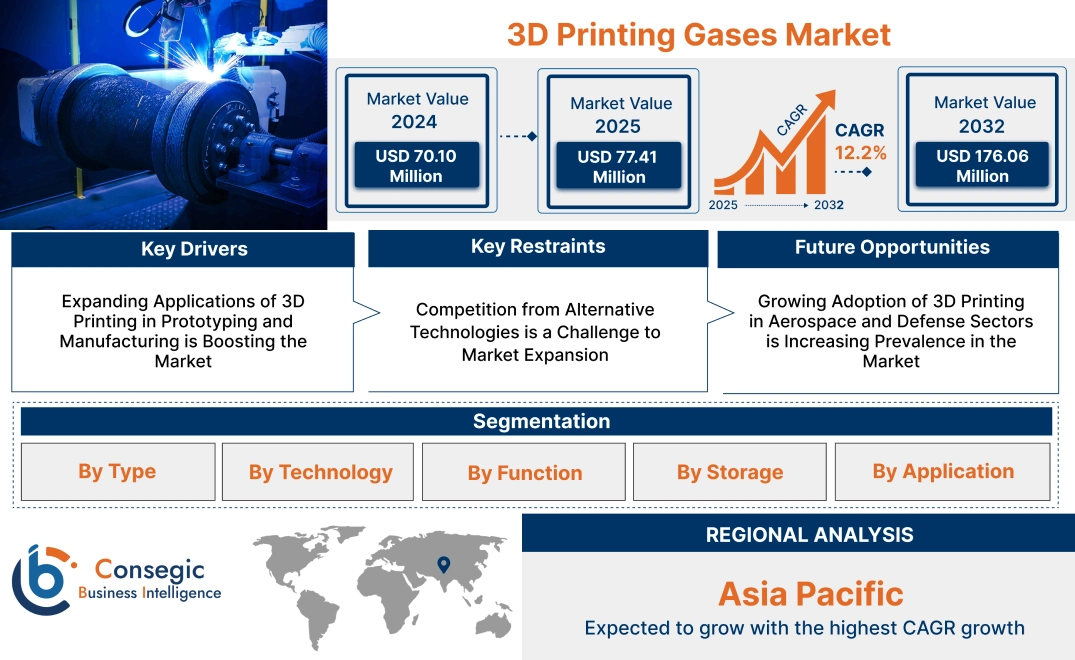

3D Printing Gases Market Size:

3D Printing Gases Market size is estimated to reach over USD 176.06 Million by 2032 from a value of USD 70.10 Million in 2024 and is projected to grow by USD 77.41 Million in 2025, growing at a CAGR of 12.2% from 2025 to 2032.

3D Printing Gases Market Scope & Overview:

The 3D printing gases focuses on the production and utilization of specialty gases essential for enhancing the performance and quality of additive manufacturing processes. These gases, including argon, nitrogen, and helium, are used for metal sintering, fusion, and creating controlled atmospheres in 3D printing applications. Key characteristics of 3D printing gases include high purity, stability, and the ability to prevent oxidation and contamination during printing. The benefits of using these gases include improved part precision, enhanced material properties, and reduced defects in printed components. Applications span aerospace, automotive, healthcare, and electronics industries, where 3D printing is employed for prototyping, tooling, and manufacturing functional parts. End-users include manufacturers, research institutions, and service providers, driven by the growing adoption of additive manufacturing, advancements in 3D printing technologies, and increasing opportunities for lightweight and complex components.

3D Printing Gases Market Dynamics - (DRO) :

Key Drivers:

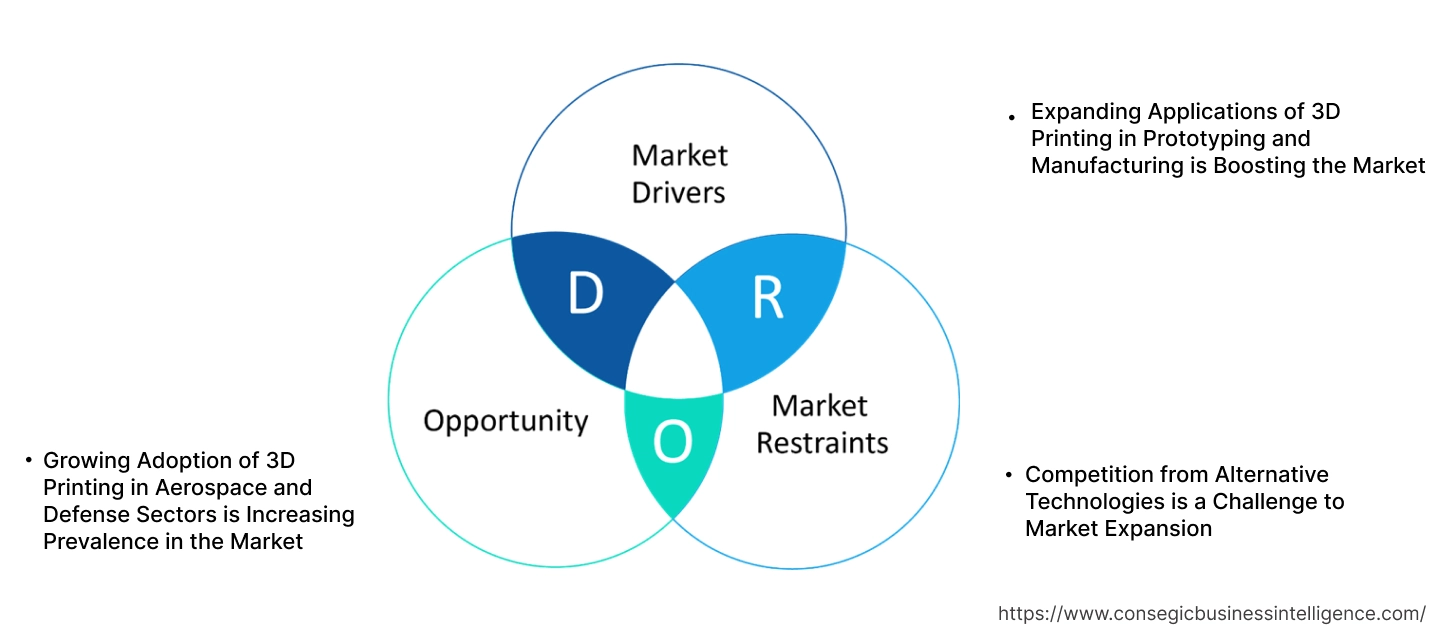

Expanding Applications of 3D Printing in Prototyping and Manufacturing is Boosting the Market.

The expanding use of 3D printing for prototyping and manufacturing is transforming production methods across industries such as automotive, healthcare, and electronics. This technology enables the creation of intricate designs, customized components, and low-volume production runs with unparalleled precision and efficiency. High-purity gases like nitrogen, argon, and helium play an essential role in stabilizing the printing environment, preventing oxidation, and enhancing the physical properties of printed parts.

In the automotive sector, 3D printing gases market trends include the development of lightweight prototypes and components for performance testing, while in electronics, intricate sensors and circuit boards are fabricated using controlled atmospheres provided by specialized gases. Healthcare applications are particularly noteworthy, where 3D printing allows the production of patient-specific implants, prosthetics, and surgical tools with high accuracy. As industries increasingly adopt innovative manufacturing techniques, the analysis highlights the growing importance of these gases in ensuring reliable and high-quality outputs across various applications.

Key Restraints:

Competition from Alternative Technologies is a Challenge to Market Expansion .

The 3D printing gases market opportunities faces challenges from alternative technologies, which continue to dominate in applications where cost and scalability are critical. Methods such as CNC machining, injection molding, and traditional subtractive manufacturing remain preferred options for industries requiring bulk production or standardized components. These established processes often do not require the controlled environments facilitated by 3D printing gases, limiting their adoption in sectors where traditional techniques meet performance needs.

For example, injection molding is commonly used in mass production due to its cost-efficiency and speed, making it a viable alternative in applications where customization is not a priority. This competitive landscape restricts the penetration of 3D printing gases, particularly in emerging markets where infrastructure for advanced manufacturing is still developing. However, analysis indicate that as additive manufacturing gains traction in high-precision and low-waste production, the advantages of 3D printing gases may increasingly offset these challenges.

Future Opportunities :

Growing Adoption of 3D Printing in Aerospace and Defense Sectors is Increasing Prevalence in the Market

The aerospace and defense industries are leveraging 3D printing technologies to enhance manufacturing processes, creating substantial opportunities for the 3D printing gases market. Additive manufacturing is widely used to produce lightweight and complex components such as turbine blades, brackets, and structural parts that meet stringent safety and performance standards. Inert gases like argon and nitrogen are critical in these processes, ensuring the mechanical integrity and precision of parts by preventing oxidation and contamination during production.

Current 3D printing gases market trends in aerospace include the rapid prototyping of complex designs and the on-demand production of spare parts, which reduce lead times and minimize waste. The analysis also highlights the integration of 3D printing in defense operations, where components with high-performance requirements are manufactured under controlled atmospheres facilitated by these gases. As sustainability and resource efficiency become priorities in these industries, 3D printing technologies and supporting gases are positioned to play a pivotal role in reshaping manufacturing methodologies.

3D Printing Gases Market Segmental Analysis :

By Type:

Based on type, the 3D printing gases market is segmented into argon, nitrogen, gas mixtures, and argon mixtures.

The argon segment accounted for the largest revenue in 3D printing gases market share in 2024.

- Argon is widely used in 3D printing applications for its inert properties, which prevent oxidation during the printing process.

- It is particularly essential in metal-based additive manufacturing, where maintaining a controlled environment is critical for achieving high-quality outputs.

- The rise of adopting advanced metal 3D printing techniques in aerospace, automotive, and healthcare industry has driven the 3D printing gases market growth for argon.

- Furthermore, the increasing use of argon mixtures for improving the precision of complex components supports its dominance in the market.

- Argon leads the market due to its role in ensuring high-quality outputs in metal-based additive manufacturing and increasing applications in advanced industries.

The gas mixtures segment is anticipated to register the fastest CAGR during the forecast period.

- Gas mixtures, including argon-nitrogen and argon-carbon dioxide combinations, are gaining traction for their ability to enhance the efficiency of specific 3D printing processes.

- These mixtures are increasingly used in industries requiring tailored solutions for printing high-performance materials.

- The trends of customizing gas environments to achieve precise material properties has significantly driven growth for gas mixtures.

- Gas mixtures are expected to grow rapidly, driven by the rising dominance in adopting tailored gas solutions for high-performance 3D printing applications.

By Technology:

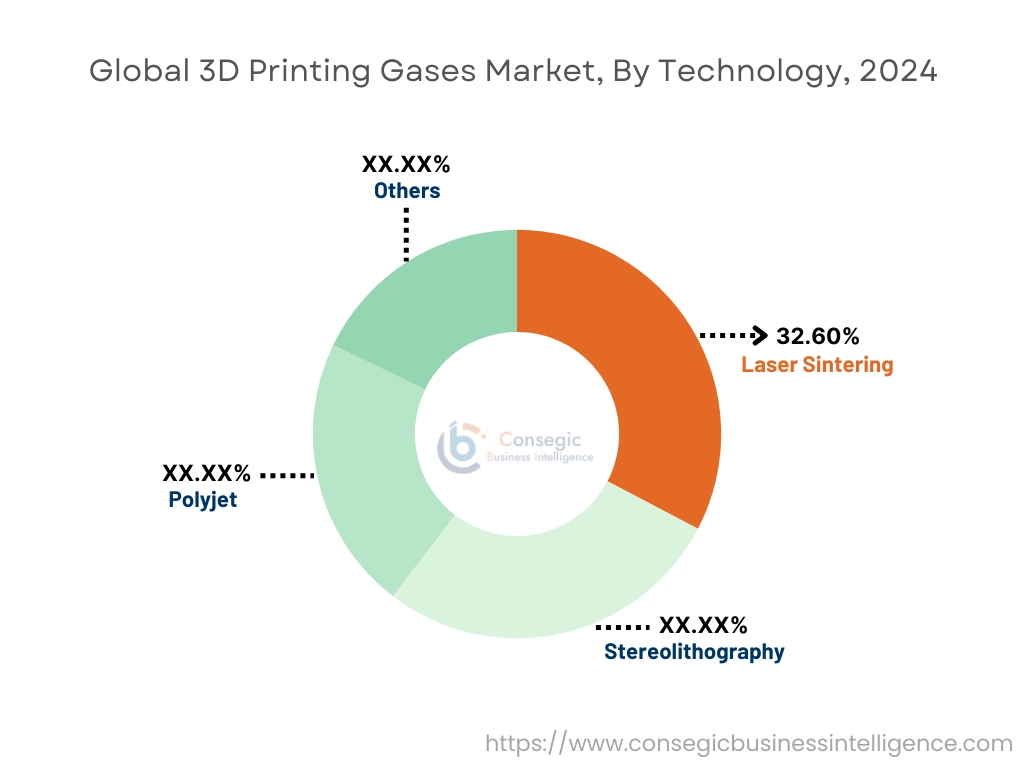

Based on technology, the market is segmented into laser sintering, stereolithography, polyjet, and others.

The laser sintering segment accounted for the largest revenue share of 32.60% in 2024.

- Laser sintering is a widely adopted technology in 3D printing, particularly for industrial applications.

- The trends of utilizing laser sintering for manufacturing durable and complex metal and polymer components has significantly driven 3D printing gases market growth for specialized gases like argon and nitrogen.

- Additionally, its capability to produce high-precision parts for industries such as aerospace, automotive, and healthcare supports its dominance in the market.

- Laser sintering dominates the market due to its extensive application in high-precision manufacturing across critical industries.

The polyjet segment is anticipated to register the fastest CAGR during the forecast period.

- Polyjet technology, known for its ability to print multi-material components with high accuracy, is gaining traction in consumer products and healthcare applications.

- The demand for 3D printing gases to maintain optimal printing conditions and enhance material performance is driving this segment.

- The trends of using polyjet for rapid prototyping and complex product designs highlights its growing adoption.

- Polyjet technology is expected to grow rapidly, supported by its versatility in printing multi-material components and increasing use in consumer and healthcare applications.

By Function:

Based on function, the market is segmented into insulation, cooling, and illumination.

The insulation segment accounted for the largest revenue share in 2024.

- Insulation plays a critical role in maintaining the stability of printing environments, particularly in metal additive manufacturing processes.

- The aim of using advanced thermal insulation techniques to enhance the efficiency of 3D printing operations has driven 3D printing gases market demand for this segment.

- Additionally, the rising focus on achieving energy-efficient manufacturing processes supports its market dominance.

- Insulation dominates the market, driven by its critical role in stabilizing 3D printing environments for high-performance manufacturing.

The cooling segment is anticipated to register the fastest CAGR during the forecast period.

- Cooling functions are essential in high-temperature 3D printing processes to prevent material degradation and ensure precision.

- The trends of adopting advanced cooling technologies in large-scale manufacturing facilities to enhance product quality and reduce material wastage is driving this segment.

- Cooling is expected to grow rapidly, supported by its importance in maintaining product quality and reducing material wastage in high-temperature printing processes.

By Storage:

Based on storage, the market is segmented into merchant liquid/bulk, cylinders & packaged gas, and tonnage.

The merchant liquid/bulk segment accounted for the largest revenue share in 2024.

- Merchant liquid and bulk distribution systems are widely used by large-scale manufacturers due to their cost efficiency and ability to support high-volume operations.

- The trends of centralizing gas supply systems in manufacturing facilities to ensure uninterrupted operations has driven demand for this segment.

- Additionally, industries requiring consistent gas quality, such as aerospace and automotive, rely heavily on merchant liquid/bulk distribution.

- Merchant liquid/bulk dominates the market, supported by its efficiency in meeting the high-volume requirements of large-scale manufacturers.

The cylinders & packaged gas segment is anticipated to register the fastest CAGR during the forecast period.

- Cylinders and packaged gases are preferred for their portability and convenience, particularly in small- to medium-scale operations.

- The trends of adopting decentralized manufacturing systems and flexible production setups has increased the 3D printing gases market demand for this distribution channel.

- Additionally, their application in research and development activities supports their growth.

- Cylinders & packaged gases are expected to grow rapidly, driven by their convenience and increasing use in decentralized production systems and R&D activities.

By Application:

Based on application, the market is segmented into design & manufacturing, consumer products, healthcare, and others.

The design & manufacturing segment accounted for the largest revenue share in 2024.

- Design and manufacturing applications rely heavily on these gases to ensure precision and quality in prototypes and finished products.

- The trends of adopting additive manufacturing in industrial sectors for cost-effective production of complex geometries is a major driver for this segment.

- Furthermore, the increasing use of 3D printing in customized manufacturing, particularly in automotive and aerospace, supports its market dominance.

- Design & manufacturing leads the market, driven by the growing 3D printing Gases market expansion of adopting additive manufacturing for cost-efficient and complex production processes.

The healthcare segment is anticipated to register the fastest CAGR during the forecast period.

- Healthcare applications, including the production of implants, prosthetics, and surgical instruments, are increasingly utilizing 3D printing gases to ensure precision and biocompatibility.

- The trends of adopting patient-specific solutions in healthcare has propelled the growth for advanced additive manufacturing processes, further boosting the role of gases in this segment.

- Healthcare is expected to grow rapidly, supported by the increasing demand for patient-specific solutions and precision manufacturing in medical applications.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

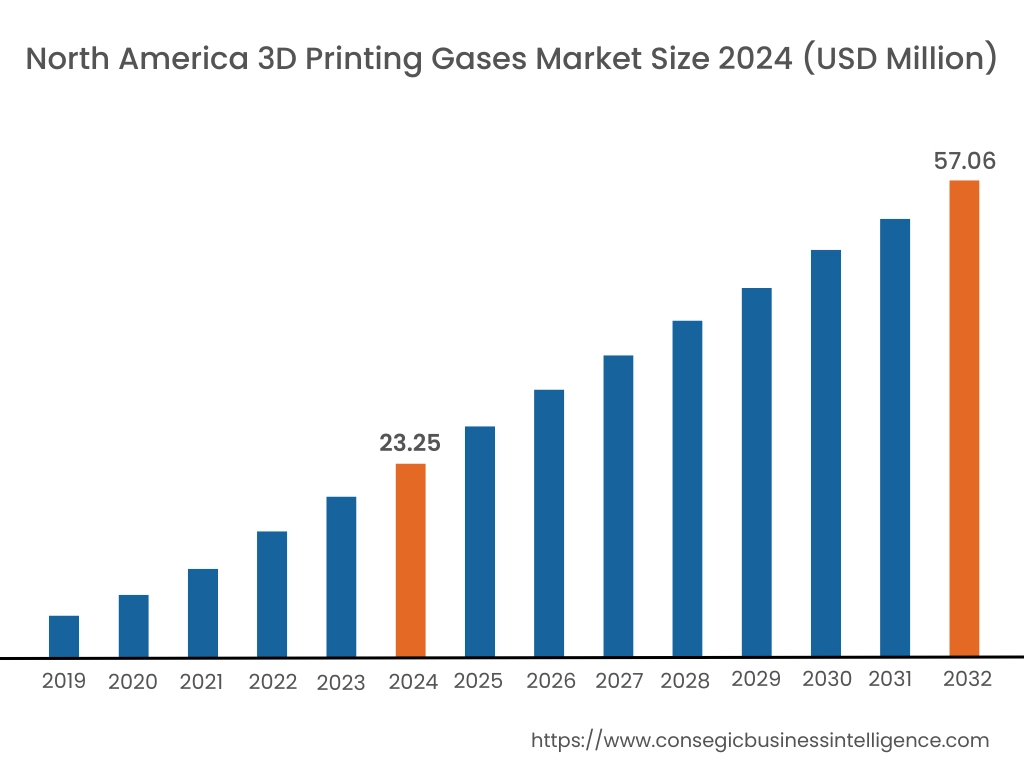

In 2024, North America was valued at USD 23.25 Million and is expected to reach USD 57.06 Million in 2032. In North America, the U.S. accounted for the highest share of 71.50% during the base year of 2024. North America holds a significant stake of the 3D printing gases market analysis, driven by the widespread adoption of 3D printing technology across industries such as aerospace, healthcare, and automotive. The U.S. leads the region with its robust manufacturing base and continuous R&D investments in additive manufacturing. The use of gases such as argon, nitrogen, and helium for improving material properties during 3D printing processes enhances market prospects. Canada also contributes significantly, particularly in the healthcare and industrial manufacturing sectors. However, the high cost of specialty gases and logistical challenges in gas distribution may limit market expansion in some areas.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 12.7% over the forecast period. Asia-Pacific is the fastest-growing region in the 3D printing gases market analysis, driven by rapid industrialization, expanding manufacturing capabilities, and increasing adoption of 3D printing technology in China, Japan, and India. China leads the market with its extensive use in automotive and electronics manufacturing. Japan’s focus on high-precision industries, including aerospace and healthcare, boosts growth for inert and specialty gases. India is witnessing rising adoption of 3D printing in prototyping and industrial applications, supported by growing awareness and government initiatives promoting advanced manufacturing technologies. However, limited infrastructure for specialty gas production and distribution in some areas may hinder market growth.

Europe is a prominent region for the 3D printing gases market, supported by strong adoption of additive manufacturing in advanced industries. Countries like Germany, the UK, and France analysis are portraying major contributors, with Germany leading due to its advanced engineering and automotive sectors. The UK is emphasizing 3D printing applications in aerospace and medical devices, requiring high-purity gases for precise manufacturing. France is witnessing increasing use of 3D printing gases in prototyping and industrial applications. However, regulatory complexities and high energy costs associated with gas production can pose challenges for manufacturers in the region.

The Middle East & Africa region is experiencing steady advancements in the 3D printing gases market, primarily driven by increasing adoption of 3D printing in construction and industrial applications. The UAE and Saudi Arabia are at the forefront, leveraging 3D printing technologies for infrastructure projects and healthcare applications. In Africa, South Africa is emerging as a key market with growing adoption of 3D printing in mining and manufacturing industries. However, challenges such as limited local production capabilities for high-purity gases and dependence on imports may impact the market’s development in the region.

Latin America is an emerging market for 3D printing gases, with Brazil and Mexico leading the region. Brazil’s growing automotive and industrial sectors drive the use of 3D printing and associated gases for prototyping and manufacturing applications. Mexico’s expanding aerospace and electronics industries further enhance the demand for specialty gases. The region is also exploring the use of 3D printing gases in healthcare for medical device manufacturing. However, economic volatility and insufficient infrastructure for specialty gas production can limit the market’s potential in the region.

Top Key Players & Market Share Insights:

The 3D printing gases market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global 3D printing gases market. Key players in the 3D printing gases industry include -

- BASF SE (Germany)

- The Linde Group (Germany)

- Matheson Tri-Gas Inc. (United States)

- Iceblick Ltd. (Ukraine)

- Universal Cryo Gas, LLC (United States)

- Air Liquide S.A. (France)

- Praxair Inc. (United States)

- Air Products and Chemicals Inc. (United States)

- Messer Group GmbH (Germany)

- Iwatani Corporation (Japan)

3D Printing Gases Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 176.06 Million |

| CAGR (2025-2032) | 12.2% |

| By Type |

|

| By Technology |

|

| By Function |

|

| By Storage |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the estimated size of the 3D Printing Gases Market by 2032? +

The market is projected to reach over USD 176.06 Million by 2032.

Which region is expected to grow the fastest? +

Asia pacific is the fastest-growing region, driven by industrialization, expanding manufacturing capabilities, and increasing adoption of 3D printing technologies in China, Japan, and India.

Which segment is expected to grow the fastest? +

Gas mixtures are anticipated to grow the fastest, driven by their tailored solutions for enhancing 3D printing performance.

Which gas type holds the largest market share? +

Argon accounts for the largest share due to its extensive use in metal-based additive manufacturing processes.