- Summary

- Table Of Content

- Methodology

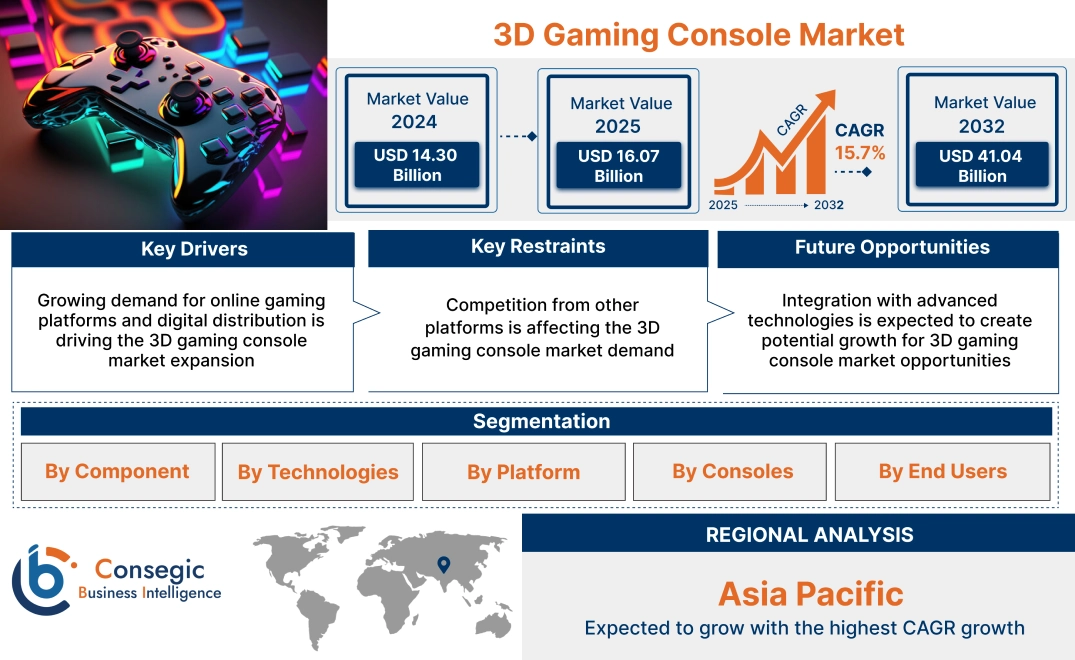

3D Gaming Console Market Size:

3D Gaming Console Market Size is estimated to reach over USD 41.04 Billion by 2032 from a value of USD 14.30 Billion in 2024 and is projected to grow by USD 16.07 Billion in 2025, growing at a CAGR of 15.7% from 2025 to 2032.

3D Gaming Console Market Scope & Overview:

3D gaming console offers users a more realistic and immersive gaming experience by providing depth perception and enhanced visual effects. It includes consoles such as PlayStation, Xbox, and Nintendo Switch, gaming laptops and PCs with high-performance graphics cards and processors, gaming peripherals like keyboards, mice, and controllers, as well as VR headsets and accessories. Manufacturers continually innovate to meet the evolving preferences of gamers, incorporating features such as faster processing speeds, higher resolution displays, ergonomic designs, and wireless connectivity. This convergence of gaming and immersive technologies has opened up new possibilities for innovation and has spurred competition among manufacturers to develop cutting-edge gaming consoles and accessories.

3D Gaming Console Market Dynamics - (DRO) :

Key Drivers:

Growing demand for online gaming platforms and digital distribution is driving the 3D gaming console market expansion

Online gaming platforms provide players with access to a vast library of games, enabling digital downloads, streaming services, and multiplayer capabilities that enhance the gaming experience beyond traditional physical media. This shift towards digital distribution has provided access to games, allowing developers to reach a global audience while reducing distribution costs and environmental impact associated with physical production.

Further, digital distribution platforms such as Steam, Epic Games Store, PlayStation Network, Xbox Live, and Nintendo eShop have become integral ecosystems for gamers, offering convenience, instant access to new releases, and a seamless user experience across multiple devices. These platforms facilitate continuous engagement through updates, downloadable content (DLC), and community features, fostering long-term player retention and monetization prospects through microtransactions and subscription models.

- For instance, in March 2025, Microsoft announced that the company has started working on 3D gaming experiences for Copilot, an AI-powered chatbot and productivity tool for Xbox platform. The tool integrates with various Microsoft applications and services, to assist users in tasks, such as gaming, content generation, and automation.

Thus, according to the 3D gaming console market analysis, the growing need for online gaming platforms is driving the 3D gaming console market size.

Key Restraints:

Competition from other platforms is affecting the 3D gaming console market demand

Traditional gaming consoles, such as Sony's PlayStation and Microsoft's Xbox, are facing increasing competition from emerging technologies like cloud gaming services and mobile gaming platforms. These alternative platforms offer convenience and accessibility, challenging the dominance of dedicated gaming consoles.

Cloud gaming services are characterized by platforms like Google Stadia, NVIDIA GeForce Now, and Microsoft's xCloud, allow users to stream high-quality games directly to their devices without the need for expensive hardware. This shift towards cloud gaming represents a significant threat to traditional console manufacturers, as it eliminates the barrier of entry posed by expensive consoles and opens up gaming to a wider audience. Therefore, the above analysis depicts that the aforementioned factors would further impact the 3D gaming console market size.

Future Opportunities :

Integration with advanced technologies is expected to create potential growth for 3D gaming console market opportunities

The global market has witnessed significant development over the past few years, driven by advancements in technology and the increasing need for immersive gaming experiences. 3D gaming consoles offer users a more realistic and engaging gaming experience by creating depth perception and enhancing visual effects. These consoles utilize stereoscopic technology to generate 3D images, providing players with a heightened sense of realism and immersion.

Further, companies are incorporating features such as virtual reality (VR) and augmented reality (AR) to create more immersive gameplay environments. VR headsets and accessories allow players to fully immerse themselves in virtual worlds, while AR technology overlays digital elements onto the real world, blending virtual and physical environments seamlessly.

- For instance, in March 2025, VividQ has ported Call of Duty: Modern Warfare II to its hologram compatible viewing format. For better immersive experience, the company advanced their frame rate, holographic image quality, and holographic hardware platform. With these advancements, players can stay immersed for longer periods.

Thus, based on the above 3D gaming console market analysis, these advancements in technology is expected to drive the 3D gaming console market opportunities.

3D Gaming Console Market Segmental Analysis :

By Component:

Based on component, the market is segmented into hardware and software.

Trends in the component:

- The growing popularity of several gaming platforms, which includes traditional consoles such as Sony PlayStation, Microsoft Xbox, and Nintendo Switch, is driving the growth of the segment. They typically feature high-performance hardware and software optimized for gaming, including advanced processors, graphics cards, and storage solutions.

- With the increasing popularity of online multiplayer gaming and the rise of game streaming services, the need for high-performance gaming systems continues to grow, which is driving the global market.

- Thus, the above factors are driving the 3D gaming console market demand.

The hardware segment accounted for the largest revenue in the year 2024.

- Hardware components play a pivotal role in delivering high-quality 3D gaming experiences. These include consoles, controllers, virtual reality (VR) headsets, and other peripherals.

- Smartphones and tablets have become prominent gaming devices, leveraging their portability, touchscreen interfaces, and connectivity features. Mobile gaming encompasses a vast ecosystem of gaming apps, from casual games to complex multiplayer titles.

- Smartphone manufacturers like Apple and Samsung, as well as app developers, continuously innovate to enhance gaming performance, graphics quality, and user experience.

- Mobile gaming also benefits from cloud gaming services that enable streaming of high-quality games to mobile devices, expanding access to console-like gaming experiences on-the-go.

- For instance, in November 2024, Tencent announced the partnership with Intel, to develop portable gaming console 3D visualization. The 3D One device is equipped with core ultra 7 258 SC based on Lunar Lake architecture and will receive 32 GB of LPDDR5x RAM and an SSD of up to 1 TB.

- With the integration of features like virtual reality (VR) and augmented reality (AR), gaming consoles continue to captivate gamers worldwide, driving the development of the segment.

- Thus, based on the above analysis, these factors are further driving the 3D gaming console market growth.

The software segment is anticipated to register the fastest CAGR during the forecast period.

- Software components encompass the games, as well as the operating systems and other applications that run on the consoles. Game developers are constantly pushing the boundaries in 3D gaming, creating visually stunning worlds with intricate gameplay mechanics.

- Additionally, operating systems play a crucial role in providing seamless user experience, optimizing performance, and facilitating access to digital storefronts where gamers can purchase new titles and downloadable content (DLC).

- Thus, based on the above analysis, these trends are expected to drive the 3D gaming console market share during the forecast period.

By Technologies:

Based on technologies, the market is segmented into active shutter technology, auto stereoscopy, KINECT motion gaming, leap motion, oculus rift, polarized shutter, project holodeck, virtual & augmented reality, and Xbox IllumiRoom.

Trends in the technologies:

- Cross-platform technology fosters a more inclusive gaming environment by enabling users to play together regardless of the devices they own. Developers also stand to gain from cross-platform compatibility as it expands their potential audience and increases engagement by allowing players to seamlessly transition between different platforms.

- The proliferation of cloud gaming platforms is fostering innovation and competition within the industry. Established players and new entrants alike are investing in cloud infrastructure and developing partnerships to enhance their gaming ecosystems. This competitive landscape is leading to improved services, such as faster streaming speeds, higher resolutions, and expanded game libraries.

The KINECT motion gaming accounted for the largest revenue share in the year 2024.

- The proliferation of affordable VR and AR devices, coupled with the growing adoption of gamification techniques, is fuelling segment expansion. These technologies offer interactive and engaging experiences, making learning more enjoyable and effective. As a result, businesses are investing significantly in immersive simulator solutions to stay ahead in a competitive landscape and address evolving training needs.

- The integration of artificial intelligence (AI) algorithms enhances scenario variability and adaptability, creating dynamic learning environments that adapt to gamer performance and behaviour.

- Thus, based on the above analysis, these factors would further supplement the 3D gaming console market

The virtual & augmented reality segment is anticipated to register the fastest CAGR during the forecast period.

- By leveraging advanced graphics, audio, and motion-tracking capabilities, VR gaming enables players to experience a sense of presence within virtual environments, fostering deeper engagement and emotional connection with the gaming experience.

- In AR gaming, players are not confined to virtual worlds displayed on a screen, instead, they interact with digital elements overlaid onto the real world through AR-enabled devices like smartphones or specialized headsets. This integration of virtual and physical realms creates a unique and dynamic gameplay experience, where players must navigate and interact with both their surroundings and digital content.

- For instance, in February 2023, Sony launched the PlayStation VR2, marking a new era in virtual reality gaming with enhanced features like haptic feedback and eye tracking. The device offers improved immersion, catering to a growing need for advanced VR gaming experiences.

- These developments in the virtual & augmented segment are anticipated to further drive the 3D gaming console market trends during the forecast period.

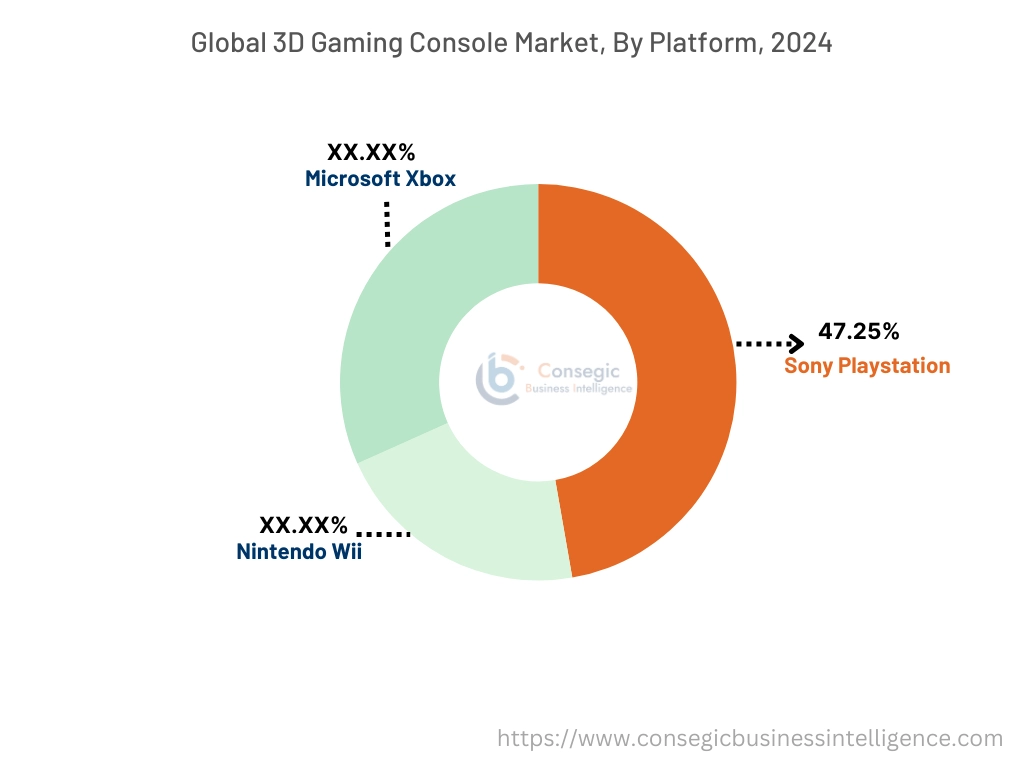

By Platform:

Based on platform, the market is segmented into Microsoft Xbox, Nintendo Wii, and Sony PlayStation.

Trends in the platform:

- The flexibility of hardware customization and the availability of extensive game libraries on platforms such as Steam are contributing to PC gaming's popularity among serious gamers, while driving the adoption of gaming platforms.

- Gaming platforms offer specialized gaming experiences or target specific demographics, contributing to the overall diversity of the 3D gaming console market. As the gaming industry evolves with advancements in technology and changing consumer preferences, these platforms play a crucial role in shaping the competitive landscape of the market.

The Sony PlayStation segment accounted for the largest revenue share of 47.25% the year 2024.

- Sony PlayStation is dominant player in the 3D gaming console market. It has powerful hardware and exclusive game titles.

- The growing investments in AR technology and gaming studios are further propelling the segment growth. These investments are driving advancements in AR hardware, software, and content development tools, enabling developers to create more sophisticated and immersive AR gaming experiences.

- The Sony PlayStation ecosystem offers immersive gaming experiences, coupled with features like PlayStation Network for online gaming and PlayStation Now for game streaming. These immersive experiences are driving the need for platform globally.

- Thus, based on the above analysis, these factors are driving the 3D gaming console market growth.

The Microsoft Xbox segment is anticipated to register the fastest CAGR during the forecast period.

- This platform features integrated displays, ergonomic controls, and a library of games tailored for mobile play.

- It appeals to gamers looking for dedicated gaming experiences without the need for additional peripherals or internet connectivity.

- The platform offers a balance between portability and gaming performance, making them popular among younger users.

- For instance, in September 2024, Xbox Research expanded its scope to include community of Xbox game developers. By directly employing with game developers, Xbox aims to get the data that improves the experience of gaming partners, while providing data and insights to future tools and services.

- These factors are anticipated to further drive the 3D gaming console market trends during the forecast period.

By Consoles:

Based on consoles, the 3D gaming console market is segmented into hand-held, home, dedicated, and micro.

Trends in consoles:

- Console gaming appeals to users seeking a more straightforward, immersive experience with exclusive titles and advanced graphics. Leading brands like Sony's PlayStation and Microsoft's Xbox have a large user base, with their consoles providing consistent performance and a rich gaming ecosystem.

- The plug-and-play nature of consoles, coupled with advancements in online multiplayer capabilities and cross-platform play, ensures their continued relevance in the market.

- The increasing need for exclusive game releases and high-profile franchises are significant factors that bolster console gaming's competitive edge.

The hand-held segment accounted for the largest revenue share in the year 2024.

- The rise of cross-platform gaming has fostered a more inclusive gaming community, enhancing multiplayer experiences and expanding the player base by creating larger, interconnected gaming ecosystems. This trend has been particularly beneficial for developers and publishers, as it encourages greater player engagement, longer play sessions, and increased monetization prospects through in-game purchases and subscriptions.

- Portable gaming consoles, such as handheld devices, have become an integral part of the gaming ecosystem, offering gamers a convenient and immersive gaming experience anytime, anywhere. These compact and versatile gaming devices cater to a diverse audience, ranging from casual gamers and dedicated gaming enthusiasts looking for high-quality graphics and gameplay on the move.

- For instance, in March 2025, Samsung introduced new Flex Gaming Console, a handheld gaming console with a display that can enlarge into a larger screen. This device can be integrated in multiple configurations and include controls such as PlayStation console and Nintendo DS.

- Thus, based on the above factors, these developments in the hand-held segment are driving the global market.

The micro segment is anticipated to register the fastest CAGR during the forecast period.

- Micro consoles have emerged as a developing segment in recent years, characterized by their compact size and affordability. These consoles offer an entry point into the world of 3D gaming for budget-conscious consumers, delivering impressive graphics and gameplay experiences at a fraction of the cost of traditional home consoles.

- Micro consoles also benefit from their versatility, often supporting a wide range of gaming titles and multimedia content. As a result, they appeal to a broad demographic, including casual gamers and families, contributing to the development of the global market.

- These factors are anticipated to further drive the global market during the forecast period.

By End Users:

Based on end users, the 3D gaming console market is segmented into healthcare, gaming, and mobile.

Trends in the end users:

- With the increasing popularity of online multiplayer gaming and the rise of game streaming services, the demand for high-performance gaming systems continues to grow.

- As eSports grows in popularity and professional gaming tournaments become more prevalent, the demand for commercial-grade gaming hardware rises. Commercial users typically invest in powerful gaming PCs, specialized peripherals, and high-resolution displays to ensure that players have access to top-tier technology during gaming events.

The gaming segment accounted for the largest revenue share in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- Businesses utilize augmented reality gaming as a powerful marketing tool to engage with customers, drive foot traffic to retail locations, and enhance brand awareness. These applications often involve interactive AR experiences integrated into advertising campaigns, product launches, or promotional events, offering consumers a novel and memorable way to interact with brands and products.

- AR gaming experiences for home use range from interactive storytelling and multiplayer games to fitness and exercise applications, offering a diverse array of entertainment options for users of all ages.

- VR gaming enables players to experience a sense of presence and agency within virtual environments, fostering deeper engagement and emotional connection with the gaming experience.

- For instance, in October 2022, Meta launched XTADIUM application on Meta Quest, to enhance the VR sports viewing experience for users. The application offers users a closer connection to their favourite sports by offering immersive 180-degree VR content.

- Thus, based on the above factors, these developments in the gaming segment are driving the global market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

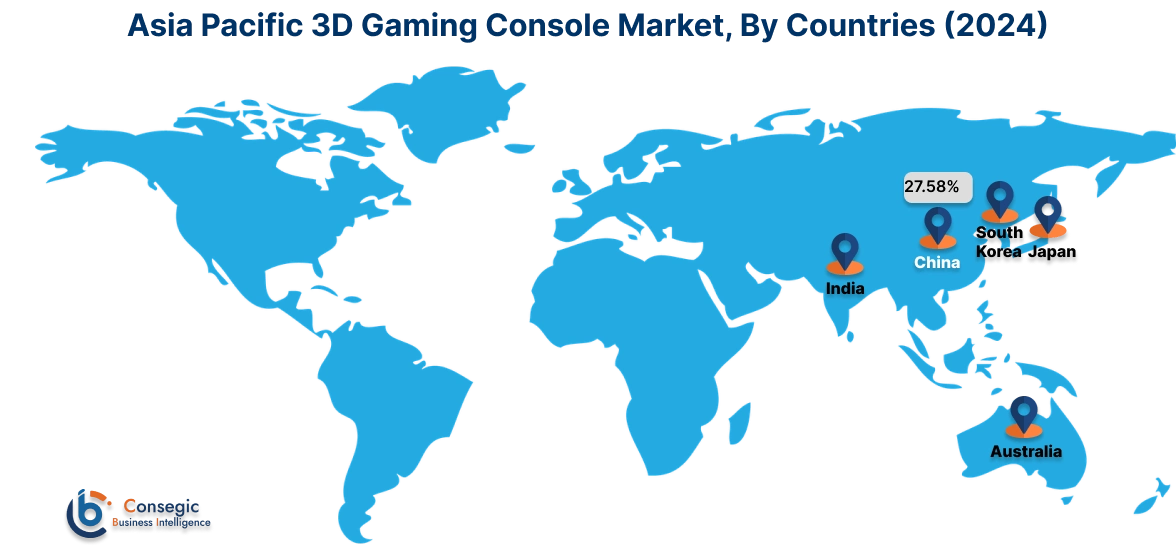

Asia Pacific 3D gaming console market expansion is estimated to reach over USD 11.32 billion by 2032 from a value of USD 3.76 billion in 2024 and is projected to grow by USD 4.24 billion in 2025. Out of this, the China market accounted for the maximum revenue split of 27.58%. The region represents a growing market for 3D gaming consoles, fueled by rapid urbanization, increasing internet penetration, and a growing middle class with a rising disposable income. Countries such as China, Japan, and South Korea are among the prominent players, with a vibrant gaming culture and adoption of the latest technological advancements. Further, the region leads in mobile gaming, driven by smartphone gaming apps and esports events that attract millions of viewers and participants. The region's diverse gaming landscape includes a mix of global brands and local manufacturers catering to regional preferences for gaming content, hardware affordability, and technological innovation. These factors would further drive the regional 3D gaming console market during the forecast period.

- For instance, in September 2022, Sony launched the Gray Camouflage Collection, which has set of accessories with the PS5 console, dual sense wireless controller, with ultra HD Blu-ray disc drive.

North America market is estimated to reach over USD 13.59 billion by 2032 from a value of USD 4.79 billion in 2024 and is projected to grow by USD 5.37 billion in 2025. In North America, the market is driven by a high penetration of smartphones and advanced gaming consoles, alongside a robust infrastructure for high-speed internet. The presence of major gaming companies and the popularity of eSports further fuel this growth. Further, the region’s technology proficient users and increasing demand for immersive gaming experiences, such as augmented reality (AR) and virtual reality (VR), are also significant contributors for driving the market. These factors would further boost the 3D gaming console in the regional market.

- For instance, in September 2024, Virtuix introduced the Omni One, a VR gaming system featuring a 360-degree treadmill that allows users to physically move within virtual environments while staying stationary in their play space. This innovation highlights the growing emphasis on physical interactivity in VR gaming.

Additionally, according to the analysis, the 3D gaming console industry in Europe is projected to witness significant development during the forecast period. Countries such as the United Kingdom, Germany, and France lead the adoption of VR gaming, fueled by a large population of gamers, innovative game developers, and rising demand for high-quality VR content. Moreover, collaborations between European gaming companies and VR startups drive innovation and development in the region's VR gaming ecosystem, further propelling the regional market Additionally, Latin America's gaming market is influenced by console gaming traditions, mobile gaming growth, and the popularity of multiplayer online games. The region has opportunities for gaming hardware manufacturers to expand their presence and cater to diverse gaming preferences. Further, countries Saudi Arabia and UAE are witnessing increasing investments in VR infrastructure and content development, driven by the growing popularity of gaming as a form of entertainment. Moreover, partnerships between international gaming companies and local distributors help accelerate the adoption of VR gaming technology in the region, paving the way for sustained market development in the upcoming years.

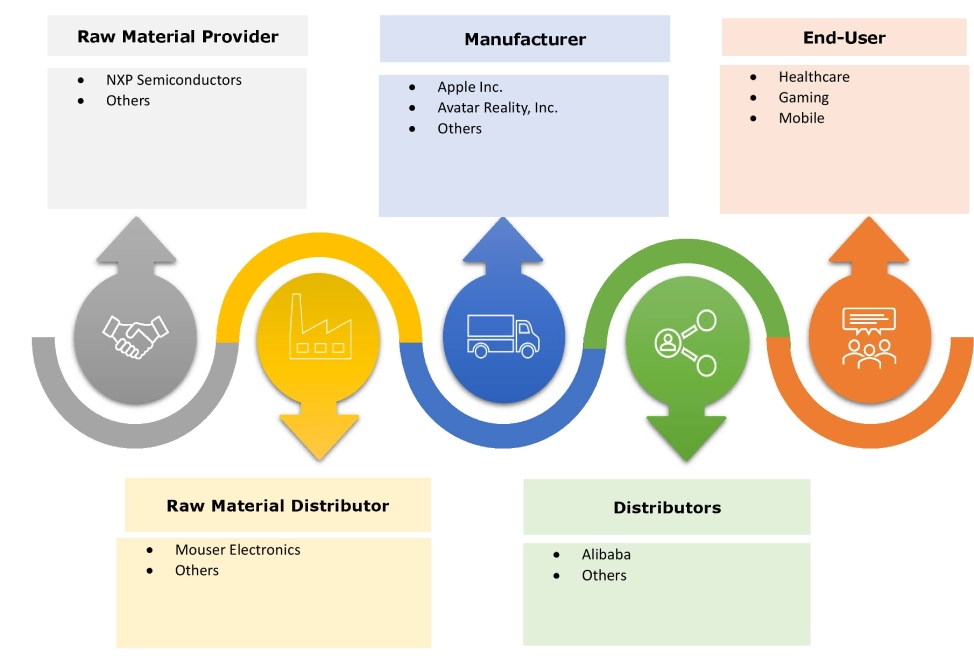

Top Key Players and Market Share Insights:

The global 3D gaming console market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the 3D gaming console industry include-

- A4TECH (Taiwan)

- Activision Publishing, Inc. (U.S.)

- Apple Inc. (U.S.)

- Avatar Reality, Inc. (U.S.)

- Electronic Arts Inc. (U.S.)

- Facebook Technologies, LLC (U.S.)

- Google (U.S.)

- Guillemot Corporation S.A. (France)

- Kava, LLC (U.S.)

- Linden Research, Inc. (U.S.)

- Logitech (Switzerland)

- Nintendo (Japan)

- NVIDIA Corporation (U.S.)

- Razer Inc. (U.S.)

- Sony Interactive Entertainment Inc. (Japan)

- Unity Technologies (U.S.)

Recent Industry Developments :

Product Launch:

- In September 2022, Zilliqa Blockchain launched Web3 games console, which features mining functions and wallet, letting gamers play while mining Zil tokens.

3D Gaming Console Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 41.04 Billion |

| CAGR (2025-2032) | 15.7% |

| By Component |

|

| By Technologies |

|

| By Platform |

|

| By Consoles |

|

| By End Users |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the 3D Gaming Console Market? +

3D Gaming Console Market Size is estimated to reach over USD 41.04 Billion by 2032 from a value of USD 14.30 Billion in 2024 and is projected to grow by USD 16.07 Billion in 2025, growing at a CAGR of 15.7% from 2025 to 2032.

Which is the fastest-growing region in the 3D Gaming Console Market? +

Asia-Pacific is the region experiencing the most rapid growth in the market.

What specific segmentation details are covered in the 3D Gaming Console report? +

The 3D gaming console report includes specific segmentation details for component, technologies, platform, consoles, end users, and region.

Who are the major players in the 3D Gaming Console Market? +

The key participants in the market are A4TECH (Taiwan), Activision Publishing, Inc. (U.S.), Apple Inc. (U.S.), Avatar Reality, Inc. (U.S.), Electronic Arts Inc. (U.S.), Facebook Technologies, LLC (U.S.), Google (U.S.), Guillemot Corporation S.A. (France), Kava, LLC (U.S.), Linden Research, Inc. (U.S.), Logitech (Switzerland), Nintendo (Japan), NVIDIA Corporation (U.S.), Razer Inc. (U.S.), Sony Interactive Entertainment Inc. (Japan), Unity Technologies (U.S.), and others.