- Summary

- Table Of Content

- Methodology

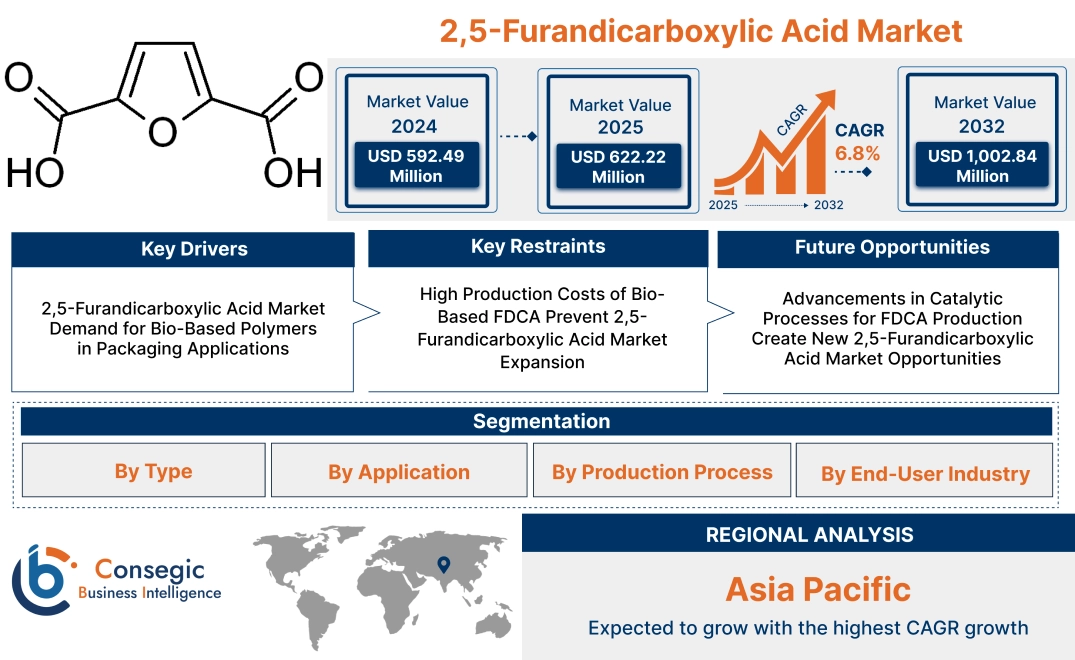

2,5-Furandicarboxylic Acid Market Size:

2,5-Furandicarboxylic Acid Market size is estimated to reach over USD 1,002.84 Million by 2032 from a value of USD 592.49 Million in 2024 and is projected to grow by USD 622.22 Million in 2025, growing at a CAGR of 6.8% from 2025 to 2032.

2,5-Furandicarboxylic Acid Market Scope & Overview:

2,5-Furandicarboxylic Acid (FDCA) is an organic compound derived from renewable resources and used in the production of bioplastics and other sustainable materials. It is a key building block for the synthesis of polyesters, providing an eco-friendly alternative to petroleum-based plastics. FDCA is typically produced through the catalytic oxidation of sugars and offers superior performance when compared to traditional petroleum-based chemicals.

The key properties of FDCA include its high thermal stability, biodegradability, and excellent compatibility with other monomers. These characteristics make it highly suitable for the production of durable, sustainable materials. The benefits of using FDCA include reduced environmental impact, lower carbon emissions, and the ability to create high-performance materials from renewable resources.

FDCA is mainly used in the production of polyethylene furanoate (PEF), a bioplastic used for packaging, textiles, and various other applications. It is also utilized in the production of resins, coatings, and other biodegradable materials. End-use industries for FDCA include packaging, automotive, textiles, and consumer goods, where sustainable, high-performance materials are a trend. The increasing shift towards sustainable practices in manufacturing is expected to expand the use of FDCA across various industries.

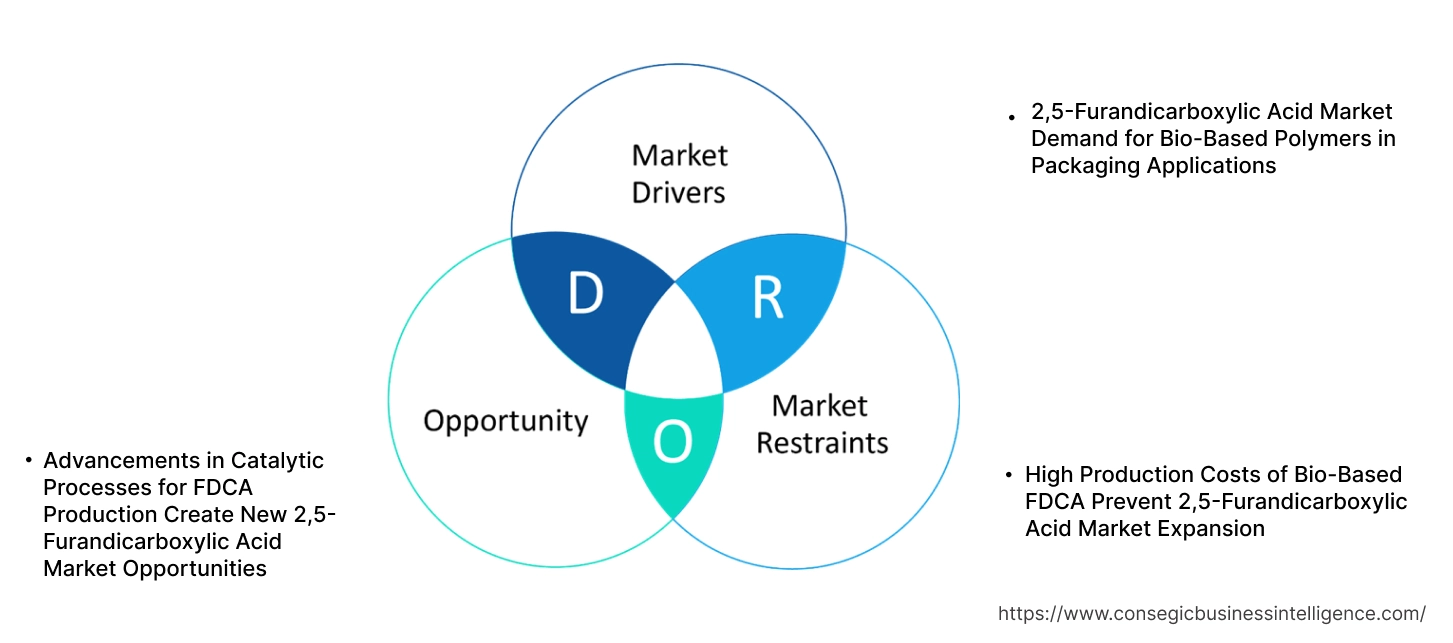

2,5-Furandicarboxylic Acid Market Dynamics - (DRO) :

Key Drivers:

2,5-Furandicarboxylic Acid Market Demand for Bio-Based Polymers in Packaging Applications

The increasing shift towards sustainable solutions in the packaging industry is driving the 2,5-furandicarboxylic acid market trend. FDCA is a key raw material for the production of polyethylene furanoate (PEF), a bio-based polymer that is emerging as an eco-friendly alternative to conventional polyethylene terephthalate (PET). PEF has superior mechanical and barrier properties compared to PET, as well as being biodegradable, making it an ideal candidate for applications in food and beverage packaging. In response to growing environmental concerns and regulatory pressure to reduce plastic waste, beverage and food manufacturers are turning to bio-based packaging solutions. For instance, several companies have already adopted PEF-based bottles for their beverages, as it helps reduce their carbon footprint while enhancing the overall sustainability of their packaging. This 2,5-furandicarboxylic acid market trend is expected to continue, further boosting the trend for FDCA as the production of PEF increases. Thus, the growing adoption of bio-based polymers, especially PEF in packaging, is a significant driver as it directly impacts the 2,5-furandicarboxylic acid market growth in packaging materials.

Key Restraints:

High Production Costs of Bio-Based FDCA Prevent 2,5-Furandicarboxylic Acid Market Expansion

One of the primary challenges hindering the widespread adoption of 2,5-furandicarboxylic acid (FDCA) is the high production costs associated with its bio-based synthesis. FDCA is typically produced through fermentation processes that require advanced technologies and renewable feedstocks, such as fructose or biomass. These feedstocks are generally more expensive than traditional petroleum-based raw materials used in producing alternatives like polyethylene terephthalate (PET). The fermentation process itself is energy-intensive and requires significant infrastructure investment, making bio-based FDCA costlier to produce. This price discrepancy between bio-based FDCA and conventional petrochemical-based materials presents a major barrier, particularly for industries that are sensitive to production costs, such as packaging. Moreover, the lack of economies of scale in bio-based FDCA production further exacerbates its cost disadvantage, as the infrastructure and technology for large-scale production are still under development. Consequently, this financial constraint is slowing the widespread adoption of FDCA-based products, especially in cost-sensitive sectors, and limiting the potential growth of the market.

Future Opportunities :

Advancements in Catalytic Processes for FDCA Production Create New 2,5-Furandicarboxylic Acid Market Opportunities

There is significant potential for reducing the production costs of 2,5-furandicarboxylic acid (FDCA) through advancements in catalytic conversion technologies. Researchers are actively working on developing more efficient catalysts that can optimize the production process, reducing energy consumption and increasing yields. Innovations in catalytic processes involve using renewable feedstocks like lignocellulosic biomass, which are more cost-effective than traditional sugar-based feedstocks. Furthermore, improvements in catalyst design could lead to higher reaction rates and greater selectivity, making the overall production process more efficient and scalable. As these catalytic technologies progress and move closer to commercialization, they hold the potential to lower production costs significantly, making bio-based FDCA a more competitive alternative to petroleum-based chemicals. The successful implementation of these advanced catalytic processes could also reduce the environmental impact of FDCA production, aligning with the growing emphasis on sustainability in the chemical industry. These technological advancements are expected to play a pivotal role in making FDCA more affordable and accessible to a wider range of industries, opening new 2,5-furandicarboxylic acid market opportunities. Thus, continued research and innovation in catalytic processes represent a major opportunity for the FDCA market to expand and become more economically viable for large-scale applications.

2,5-Furandicarboxylic Acid Market Segmental Analysis :

By Type:

Based on type, the market is segmented into bio-based and petrochemical-based 2,5-furandicarboxylic acid.

The bio-based segment accounted for the largest revenue in 2,5-Furandicarboxylic Acid Market share in 2024.

- Derived from renewable sources like carbohydrates, bio-based 2,5-furandicarboxylic acid minimizes reliance on fossil fuels.

- It is a key material for manufacturing biodegradable polymers and sustainable packaging solutions.

- This type is favored due to its lower environmental impact and compliance with global sustainability goals.

- Its applications in bio-based plastics like polyethylene furanoate (PEF) strengthen its dominance in eco-conscious industries.

- Therefore, according to 2,5-furandicarboxylic acid market analysis, the bio-based type dominates the market due to its sustainability and alignment with environmental regulations.

The petrochemical-based segment is anticipated to register the fastest CAGR during the forecast period.

- Petrochemical-based 2,5-furandicarboxylic acid utilizes petroleum derivatives for its production.

- It serves specialized industrial needs, ensuring consistent availability and reliable performance.

- Technological advances in refining and hybrid processes enhance production efficiency for this type.

- This segment appeals to markets requiring high-volume production with controlled specifications.

- Thus, according to 2,5-furandicarboxylic acid market analysis, the rapid adoption of petrochemical-based options in emerging markets supports their anticipated growth.

By Application:

Based on application, the market is segmented into polymers, plasticizers, coatings, resins, solvents, and others.

The polymers segment accounted for the largest revenue in 2,5-Furandicarboxylic Acid Market share in 2024.

- Polymers derived from 2,5-furandicarboxylic acid, like PEF, offer superior mechanical strength and barrier properties.

- PEF is increasingly used in beverage bottles and food packaging, replacing traditional plastics.

- The segment benefits from the global push for sustainable packaging solutions among major brands.

- Applications in flexible and rigid packaging formats further consolidate its market position.

- Therefore, according to market analysis, the polymers segment leads the market due to its alignment with sustainable packaging trends and superior material properties.

The coatings segment is anticipated to register the fastest CAGR during the forecast period.

- 2,5-Furandicarboxylic acid enhances the durability and corrosion resistance of coatings.

- Its eco-friendly properties make it a preferred choice for industrial and consumer applications.

- Increasing trend for high-performance coatings in automotive and construction sectors boosts this segment.

- Continuous development of bio-based formulations strengthens the adoption of coatings derived from this compound.

- Thus, according to market analysis, advancements in eco-friendly formulations drive the adoption of 2,5-furandicarboxylic acid in coatings.

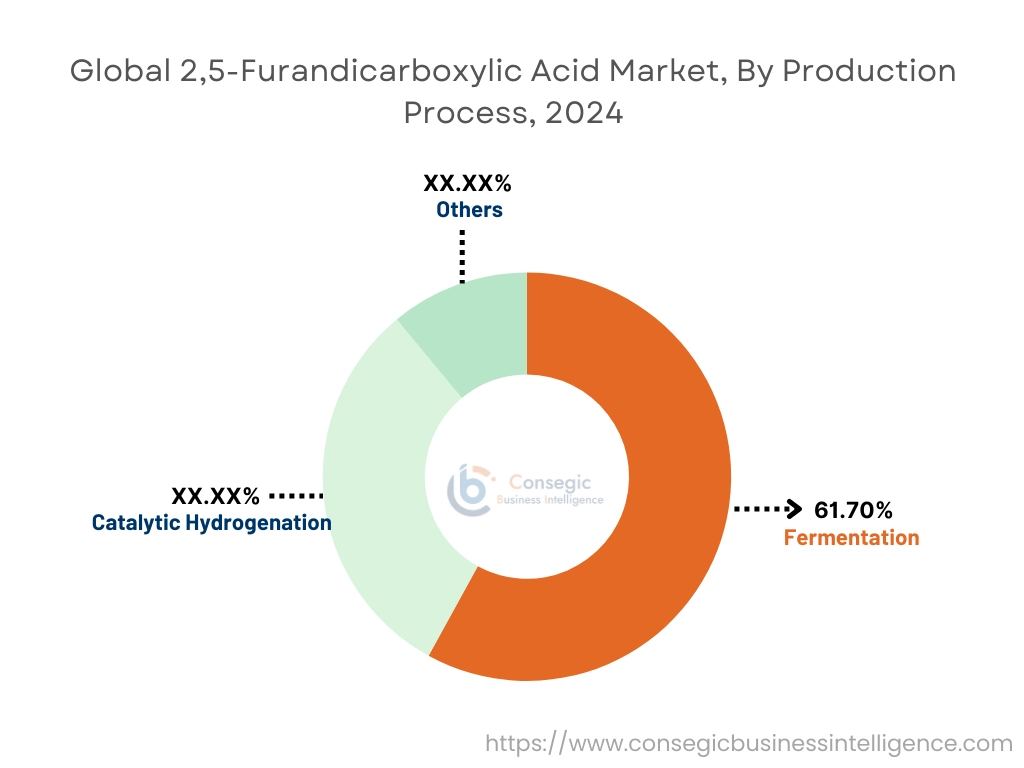

By Production Process:

Based on production process, the market is segmented into catalytic hydrogenation, fermentation, and other processes.

The fermentation process accounted for the largest revenue share by 61.70% in 2024.

- This process uses renewable feedstocks like sugars, ensuring environmental sustainability.

- High-purity production of 2,5-furandicarboxylic acid through fermentation supports diverse industrial applications.

- Its compatibility with green chemistry principles enhances its adoption across industries.

- Fermentation is cost-effective and widely used for manufacturing bio-based variants.

- Therefore, according to market analysis, fermentation leads the market due to its cost-efficiency and alignment with sustainable practices.

The catalytic hydrogenation process is anticipated to register the fastest CAGR during the forecast period.

- Catalytic hydrogenation delivers high conversion rates and efficiency in producing 2,5-furandicarboxylic acid.

- The process benefits from continuous advancements in catalyst technology, improving scalability and cost-effectiveness.

- It offers flexibility for both bio-based and petrochemical-based production methods.

- Industrial trend for hybrid production processes accelerates its adoption globally.

- Thus, according to market analysis, advancements in catalyst technologies fuel the adoption of catalytic hydrogenation.

By End-User Industry:

Based on the end-user industry, the market is segmented into packaging, automotive, electronics, construction, agriculture, and others.

The packaging segment accounted for the largest revenue share in 2024.

- Packaging uses bio-based polymers from 2,5-furandicarboxylic acid for producing biodegradable materials.

- Increasing consumer trend for eco-friendly alternatives drives its adoption in food and beverage packaging.

- Major corporations prioritize sustainability goals, enhancing the use of 2,5-furandicarboxylic acid in this segment.

- Regulatory mandates on plastic reduction encourage the use of bio-based materials in packaging.

- Therefore, according to market analysis, the packaging sector dominates due to its pivotal role in adopting biodegradable materials to address sustainability challenges.

The automotive segment is anticipated to register the fastest CAGR during the forecast period.

- Lightweight materials derived from 2,5-furandicarboxylic acid are used for improving fuel efficiency.

- Automotive interiors and exteriors benefit from the enhanced durability of bio-based polymers.

- Increased focus on reducing emissions and complying with environmental regulations drives growth.

- The growing adoption of electric vehicles further amplifies trend for sustainable materials.

- Thus, according to market analysis, increase in the 2,5-furandicarboxylic acid market demand for lightweight and eco-friendly materials has been driven by the automotive segment’s growth.

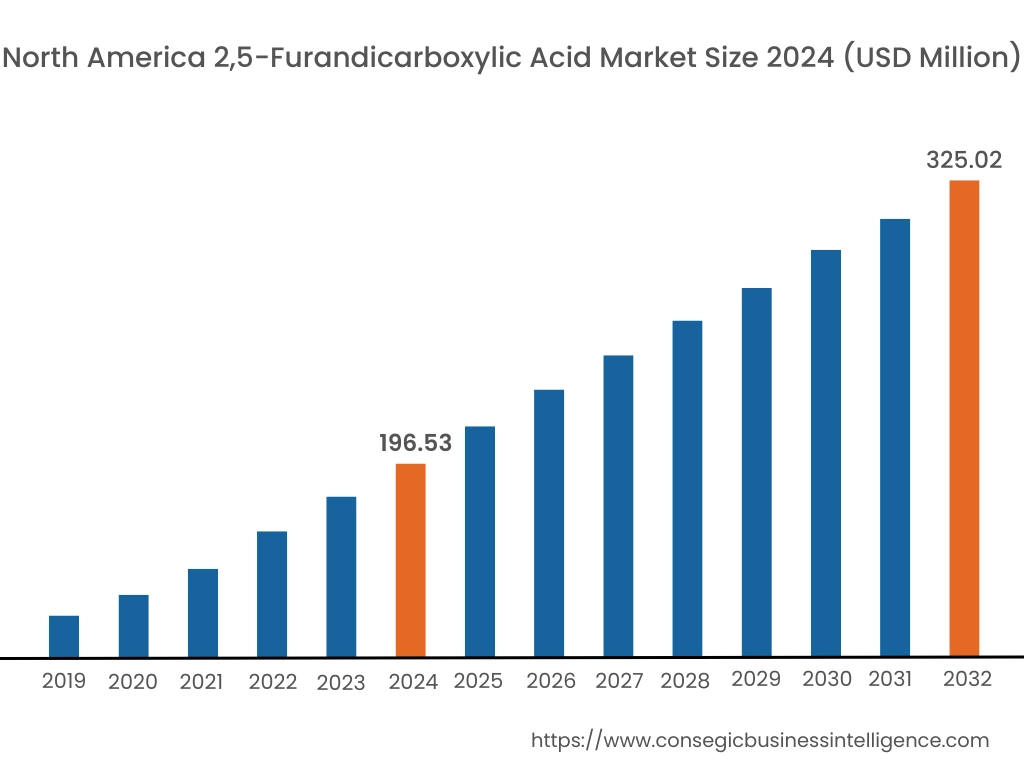

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

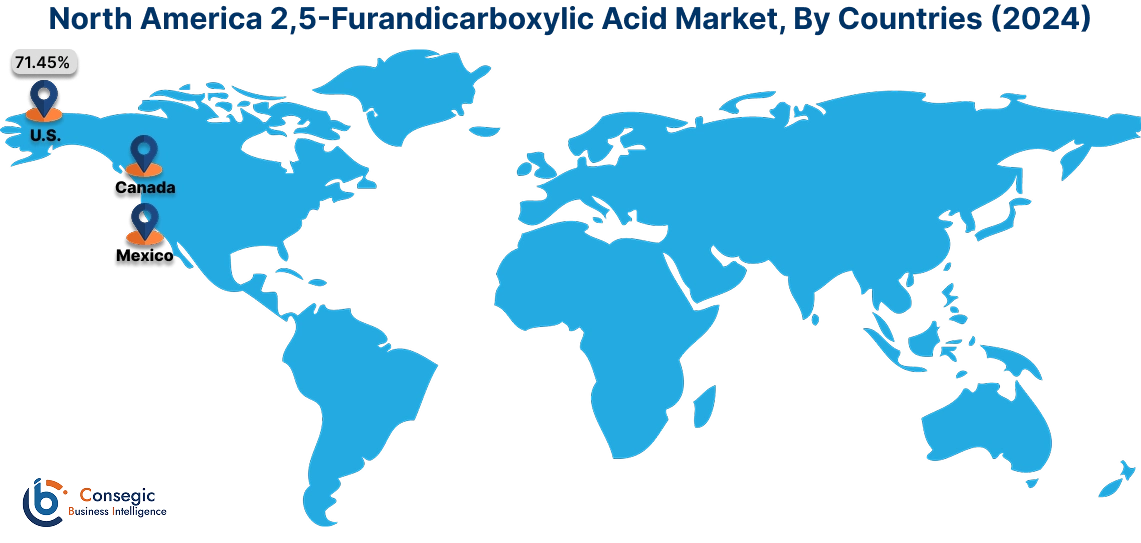

In 2024, North America was valued at USD 196.53 Million and is expected to reach USD 325.02 Million in 2032. In North America, the U.S. accounted for the highest share of 71.45% during the base year of 2024. North America plays a significant role in the 2,5-furandicarboxylic acid (FDCA) market, largely due to advancements in sustainable and bio-based chemicals. The United States and Canada are key players in the research, development, and commercialization of FDCA. The rising demand for eco-friendly packaging materials, particularly in the automotive and textile sectors, is driving market growth. The region's strong regulatory support for renewable resources and the push for reduced carbon emissions also contribute to 2,5-furandicarboxylic acid market expansion.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.8% over the forecast period. Asia-Pacific is a rapidly expanding region for the 2,5-furandicarboxylic acid market, with significant developments in China, Japan, and India. The increasing shift toward bio-based chemicals in the region’s manufacturing sectors, including textiles, plastics, and packaging, fuels market demand. The availability of cost-effective raw materials and large-scale production capacities in countries like China supports the region's dominance in the FDCA market. Additionally, governmental policies promoting sustainability and reducing reliance on petrochemical-based products encourage the adoption of FDCA in various industries.

Europe holds a strong position in the 2,5-furandicarboxylic acid market, supported by a well-established bio-based chemical industry. Countries like Germany, France, and the Netherlands focus on sustainable production methods, contributing to the market's expansion. Stringent regulations aimed at reducing environmental impact and enhancing the use of renewable resources further promote the adoption of FDCA. The region's automotive and packaging sectors are leading the demand for FDCA, driven by the push for green alternatives to traditional materials like PET.

The 2,5-furandicarboxylic acid market in the Middle East and Africa is in the early stages of development. The region has a strong petrochemical industry, but the demand for bio-based chemicals is growing slowly. Several countries are investing in sustainable technologies and shifting toward eco-friendly materials, albeit at a more gradual pace compared to other regions. Economic diversification efforts in the UAE and Saudi Arabia, along with growing interest in green initiatives, are expected to drive demand for FDCA in the coming years.

Latin America’s market for 2,5-furandicarboxylic acid is expanding, particularly in countries like Brazil and Mexico. There is an increasing focus on sustainable and renewable chemical alternatives, especially in the packaging, automotive, and textile sectors. However, challenges such as the limited availability of production facilities and high raw material costs hinder market development. Still, local initiatives aimed at boosting the bio-based chemical industry and reducing environmental impact are creating opportunities for FDCA adoption in the region.

Top Key Players & Market Share Insights:

The Global 2,5-Furandicarboxylic Acid Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global 2,5-Furandicarboxylic Acid Market. Key players in the 2,5-Furandicarboxylic Acid industry include-

- Albis Plastic GmbH (Germany)

- Avantium (Netherlands)

- Segetis, Inc. (United States)

- LCY Chemical Corp. (Taiwan)

- BASF SE (Germany)

- Genomatica, Inc. (United States)

- Corbion N.V. (Netherlands)

- Furanix Technologies (Netherlands)

- Braskem S.A. (Brazil)

- Eastman Chemical Company (United States)

2,5-Furandicarboxylic Acid Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,002.84 Million |

| CAGR (2025-2032) | 6.8% |

| By Type |

|

| By Application |

|

| By Production Process |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the 2,5-Furandicarboxylic Acid Market? +

In 2024, the 2,5-Furandicarboxylic Acid Market was USD 132.87 million.

What will be the potential market valuation for the 2,5-Furandicarboxylic Acid Market by 2032? +

In 2032, the market size of 2,5-Furandicarboxylic Acid Market is expected to reach USD 202.36 million.

What are the segments covered in the 2,5-Furandicarboxylic Acid Market report? +

The type, application, production process, and end-user industry are the segments covered in this report.

Who are the major players in the 2,5-Furandicarboxylic Acid Market? +

Albis Plastic GmbH (Germany), Avantium (Netherlands), Genomatica, Inc. (United States), Corbion N.V. (Netherlands), Furanix Technologies (Netherlands), Braskem S.A. (Brazil), Eastman Chemical Company (United States), Segetis, Inc. (United States), LCY Chemical Corp. (Taiwan), BASF SE (Germany) are the major players in the 2,5-Furandicarboxylic Acid market.